Decoding Cancer at the Genetic Level: Molecular Oncology Market Set to Grow from USD 2.3 Billion in 2023 to Over US$ 7.4 Billion by 2034 at 11.0% CAGR

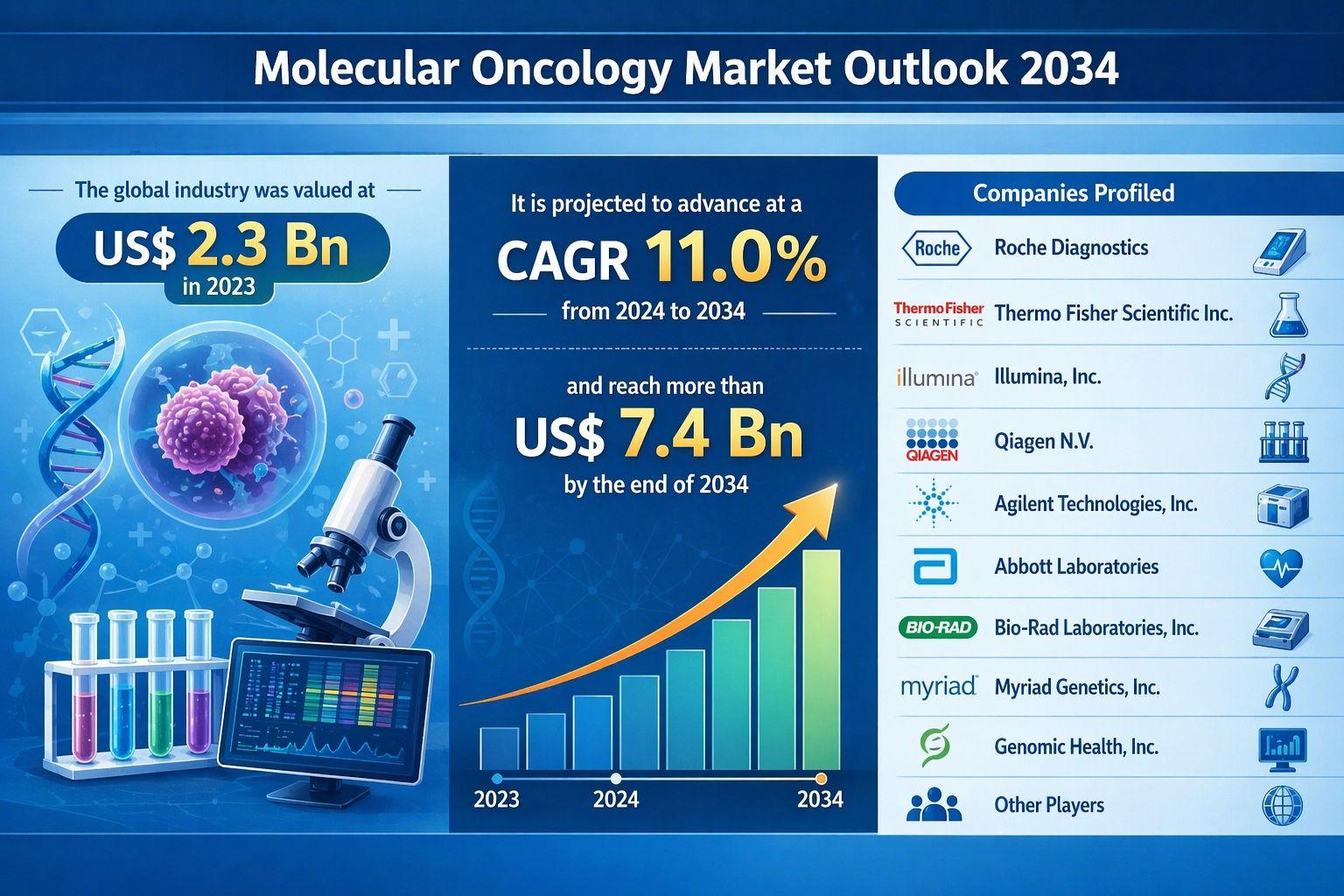

The global molecular oncology market is entering a transformative phase, driven by rapid advancements in genetic research and precision medicine. Valued at US$ 2.3 Bn in 2023, the industry is projected to expand at a robust CAGR of 11.0% between 2024 and 2034, surpassing US$ 7.4 Bn by the end of the forecast period. This strong growth trajectory reflects the increasing importance of molecular-level insights in cancer diagnosis, treatment, and monitoring.

Molecular oncology represents a paradigm shift in cancer care, moving away from generalized treatment approaches toward targeted, patient-specific therapies. By analyzing genetic mutations and molecular pathways, healthcare providers can tailor treatment plans that significantly improve clinical outcomes.

Analysts’ Viewpoint

Sustained investment in cancer research continues to play a pivotal role in advancing molecular oncology. Funding from governments, private organizations, and pharmaceutical companies is accelerating the development of cutting-edge technologies such as next-generation sequencing (NGS), single-cell analysis, and CRISPR/Cas9 gene editing.

These innovations are enabling researchers to decode cancer at an unprecedented level of detail. Collaborative efforts between scientists, clinicians, and industry players are bridging the gap between laboratory discoveries and clinical applications. As a result, novel biomarkers are being identified for early detection, prognosis, and disease monitoring, ultimately improving survival rates and quality of life for patients.

Market Introduction

Molecular oncology focuses on understanding cancer through genetic and molecular profiling. Clinical laboratories are increasingly adopting molecular diagnostics to guide targeted therapy decisions across a wide range of cancers, including lung, breast, colorectal, ovarian, prostate, melanoma, lymphoma, and multiple myeloma.

Researchers utilize a combination of genomics, computational biology, tumor imaging, and both in vitro and in vivo models to analyze cancer behavior. These techniques help identify genes responsible for tumor growth and progression, which can then be targeted through innovative therapies or diagnostic tools.

The integration of these technologies enables validation of new candidate genes and supports the development of personalized treatment strategies, making molecular oncology a cornerstone of modern oncology.

Key Market Drivers

Precision Cancer Care

One of the most significant drivers of the molecular oncology market is the growing emphasis on precision cancer care. Advances in genetic profiling have transformed how oncologists assess risk and determine treatment pathways. By identifying specific mutations within cancer cells, clinicians can select therapies that are more effective and less toxic.

As personalized medicine continues to gain traction, demand for advanced diagnostic tools is rising rapidly. Molecular oncology provides the insights needed to differentiate between cancer subtypes and optimize treatment decisions, reducing reliance on trial-and-error approaches.

Facilitated Process Scale-up and Versatility in Research

Technological advancements are enhancing the scalability and versatility of molecular oncology research. Instruments such as flow cytometers, PCR systems, and NGS platforms are essential for genetic analysis and biomarker identification.

NGS technology, in particular, has revolutionized the field by enabling rapid sequencing of entire genomes or targeted regions. This provides comprehensive insights into tumor genetics, supporting more accurate diagnoses and treatment planning.

Additionally, innovations such as mass spectrometry and digital PCR are further driving market growth by improving sensitivity, accuracy, and throughput in molecular analysis.

Surge in Incidence of Lung Cancer

The rising global burden of lung cancer is another major factor propelling market expansion. Lung cancer remains one of the most prevalent and deadly cancers worldwide, creating a significant demand for advanced diagnostic and therapeutic solutions.

Despite declining smoking rates and improvements in early detection, lung cancer continues to pose a serious public health challenge. Risk factors such as occupational exposure and pre-existing lung conditions further contribute to disease prevalence.

The high incidence of lung cancer necessitates the adoption of molecular oncology technologies to enable early detection, identify actionable mutations, and guide targeted therapies, thereby improving patient outcomes.

Dominance of PCR Technology

Polymerase Chain Reaction (PCR) technology holds the largest share in the molecular oncology market. Techniques such as reverse transcription PCR (RT-PCR) and digital PCR offer several advantages over traditional diagnostic methods.

PCR minimizes subjective interpretation, reducing both intra- and interobserver variability. Unlike conventional techniques that require highly experienced pathologists, PCR results are straightforward and easy to interpret, making the technology accessible even in resource-limited settings.

Moreover, PCR methods can be automated and standardized across laboratories, enabling large-scale testing and molecular subtyping of patients. The ability to deliver reliable, accurate, and rapid results has solidified PCR’s position as a preferred diagnostic tool in oncology.

Role of Diagnostic Laboratories

Diagnostic laboratories are a critical end-user segment in the molecular oncology market. These facilities play a central role in delivering accurate and timely test results that guide treatment decisions and monitor therapeutic effectiveness.

As cancer care becomes increasingly precise, the need for high-quality diagnostic services continues to grow. Laboratories equipped with advanced molecular testing capabilities are essential for identifying genetic mutations and ensuring optimal treatment strategies.

Their contribution to early detection and personalized care underscores their importance in the broader oncology ecosystem.

Regional Outlook

North America dominates the global molecular oncology market, supported by advanced healthcare infrastructure, strong research capabilities, and high healthcare expenditure. The region benefits from widespread adoption of cutting-edge technologies and a favorable regulatory environment.

The United States, in particular, leads the market due to the presence of major pharmaceutical and biotechnology companies, as well as extensive research initiatives. Organizations such as the American Cancer Society provide valuable data and insights that support informed decision-making and resource allocation.

Additionally, the region’s large patient population and ongoing investment in oncology research create significant growth opportunities for market players.

Competitive Landscape and Key Players

The molecular oncology market is highly competitive, with several leading companies focusing on innovation and strategic collaborations. Key players include Roche Diagnostics, Thermo Fisher Scientific Inc., Illumina, Inc., Qiagen N.V., Agilent Technologies, Inc., Abbott Laboratories, Bio-Rad Laboratories, Inc., Myriad Genetics, Inc., and Genomic Health, Inc..

These companies are investing heavily in research and development to introduce innovative products and expand their market presence. Their strategies include product launches, partnerships, and geographic expansion.

Key Developments

Recent developments highlight the dynamic nature of the molecular oncology market. In November 2023, Roche Diagnostics launched the LightCycler PRO System, enhancing its PCR testing portfolio and providing advanced solutions for cancer and infectious disease testing.

In the same month, Zydus Lifesciences partnered with Guardant Health to introduce the Guardant360 suite of biopsy tests in India and Nepal. These tests aim to enable genomic profiling and support targeted treatment decisions for advanced cancers.

Market Segmentation Overview

The molecular oncology market is segmented based on product, cancer type, technology, end-user, and region.

- By Product: Instruments, reagents, and others

- By Cancer Type: Lung, breast, colorectal, ovarian, pancreatic, and others

- By Technology: PCR, NGS, microarray, FISH, and others

- By End-user: Hospitals and clinics, diagnostic laboratories, cancer centers, and public health agencies

- By Region: North America, Europe, Asia Pacific, Latin America, and Middle East & Africa

This comprehensive segmentation reflects the diverse applications and growing adoption of molecular oncology across healthcare systems worldwide.

Investment Landscape and Future Opportunities

The investment landscape in molecular oncology is highly promising, with increasing funding directed toward research, technology development, and infrastructure. Venture capital firms, government agencies, and private investors are recognizing the potential of molecular diagnostics and targeted therapies.

Opportunities lie in expanding access to advanced diagnostics in emerging markets, developing cost-effective testing solutions, and integrating artificial intelligence with molecular data analysis. These innovations are expected to enhance diagnostic accuracy and streamline clinical workflows.

Conclusion

The molecular oncology market is poised for significant growth over the next decade, driven by advancements in precision medicine, rising cancer incidence, and continuous technological innovation. With a projected market value exceeding US$ 7.4 Bn by 2034, the industry is set to play a crucial role in transforming cancer care.

As research continues to uncover the molecular mechanisms of cancer, and as collaborations between stakeholders intensify, molecular oncology will remain at the forefront of medical innovation—offering hope for more effective treatments, earlier detection, and improved patient outcomes worldwide.

Categorías

Read More

North America is emerging as a critical hub for advanced semiconductor manufacturing as governments and private organizations continue to invest heavily in domestic chip production capabilities. The region's focus on strengthening supply chains, reducing dependence on overseas semiconductor sources, and supporting next-generation technologies has accelerated demand for advanced wafer...

Medical Grade Commercial Cleaning: The Most Trusted Solution for Your Facility Cleanliness today is no longer just a "nice to have" — it has become an absolute necessity, especially for spaces where health and hygiene directly affect people's safety. Hospitals, clinics, labs, dental offices, and corporate healthcare facilities cannot rely on ordinary cleaning methods. This is exactly why...

Have you ever felt physically fine but mentally drained? You sit down to work, but your mind feels foggy. You try to focus, but distractions pull you away. This is often a sign of low mental energy. Mental stamina is just as important as physical strength. It helps you think clearly, solve problems, make decisions, and stay productive. Without it, even simple tasks can feel...

According to the latest report published by Data Bridge Market Research, the Water Purifiers Market CAGR Value The global water purifiers market size was valued at USD 35.01 billion in 2024 and is projected to reach USD 65.28 billion by 2032, with a CAGR of 8.10% during the forecast period of 2025 to 2032. An influential Water Purifiers Market report analyses...

Dubai is famous for luxury attractions, tall buildings, and modern lifestyle, but the desert side of Dubai offers a completely different experience. One of the most popular desert destinations is Al Badayer Desert. Known for its giant red dunes and exciting activities, this place attracts adventure lovers from around the world. An al badayer desert safari is perfect for travelers who want...