Understanding the Financial Calculations in Contemporary Property Ownership

The landscape of wealth creation has shifted significantly in recent years, moving away from simple savings accounts toward more tangible assets. For many, the ultimate goal is to establish a portfolio that generates passive income while building equity over time. However, the bridge between a visionary idea and a signed deed is built on a foundation of rigorous data. Success in the current market requires a deep understanding of the mechanics behind rental property loans and a willingness to look at your financial life through a purely objective lens. It is no longer enough to just have a good eye for real estate; you must have a mind for the underlying economics that drive lending decisions.

When we peel back the layers of a standard mortgage application, we find a complex ecosystem of risk assessment. Financial institutions are not just looking at your ability to pay; they are looking at the stability of the entire real estate market and your place within it. This analytical approach is what separates the casual buyer from the professional investor. By dissecting the requirements and understanding the variables that influence a loan officer, you can better position yourself to secure the capital needed for your next major acquisition. The journey is as much about psychological preparation as it is about mathematical certainty.

Deconstructing the Borrower Profile

To understand how a lender thinks, you must first understand the primary tool they use to weigh your eligibility. The use of a debt service ratio calculator is the standard practice for determining how much additional pressure your monthly budget can withstand. This calculation takes every existing obligation—from student loans to car payments—and pits them against your total earnings. An analytical look at these numbers often reveals that even high earners can be rejected if their lifestyle costs are too high. Investors who succeed are those who proactively manage these ratios, keeping their personal overhead low to maximize their borrowing capacity for income-generating assets.

The Variable Nature of Modern Income

As the gig economy and entrepreneurship continue to grow, the way we define financial stability has evolved. However, traditional banking systems have been slower to adapt, making the process of providing proof of income self employed individuals need quite a strenuous task. An analytical review of a self-employed person's finances often involves looking at net profit rather than gross revenue. This is a crucial distinction, as many business owners use legal deductions to lower their tax burden, which inadvertently lowers their "on-paper" income in the eyes of a bank. Balancing tax efficiency with the need to show high earnings for a loan is a delicate dance that requires long-term planning and precise record-keeping.

The Rise of Alternative Capital Sources

For those who find the barriers of traditional banking too high, the market has responded with a variety of specialized options. Exploring the world of non traditional mortgage lenders reveals a different set of priorities. These lenders often employ an asset-based underwriting style, meaning they are more concerned with the property’s potential performance than the borrower's personal history. This shifts the analysis from the individual to the investment itself. While these sources provide much-needed liquidity, they also require the borrower to be even more diligent in their own property analysis to ensure the higher costs of these loans do not erase their profit margins.

The table below provides an analytical comparison of the different lending paths available in today's market:

|

Lending Category |

Primary Risk Focus |

Financial Flexibility |

Ideal Use Case |

|

Institutional Banks |

Personal Credit & W-2 Income |

Low (Strict Guidelines) |

Low-risk, high-credit borrowers |

|

Private Equity Firms |

Property Equity & Exit Strategy |

High (Negotiable Terms) |

Fix-and-flip or short-term holds |

|

Portfolio Lenders |

Relationship & Asset Health |

Medium (Customized) |

Expanding existing portfolios |

Data-Driven Property Selection

An analytical approach to real estate also demands a cold, hard look at the property itself. Experienced investors do not buy based on emotion or the aesthetic appeal of a home. Instead, they look at the metrics that matter to a lender. This includes a thorough investigation into the neighborhood's vacancy rates, the local employment base, and the historical appreciation of the area. A house is merely a vessel for cash flow; if the numbers do not support the debt, the house is a liability rather than an asset. By focusing on these objective truths, you align your interests with those of the lender, creating a more persuasive argument for funding.

Consider these critical analytical factors before making an offer:

-

Capitalization Rate (Cap Rate) relative to the local market average.

-

Gross Rent Multiplier to gauge how quickly the property pays for itself.

-

Cash-on-Cash Return to measure the actual yield on your invested capital.

-

Operating Expense Ratio to ensure maintenance doesn't swallow profits.

The Impact of Economic Cycles

Finally, any deep analysis must account for the broader economic climate. Interest rates, inflation, and housing supply are all external factors that can change the viability of a deal overnight. A smart investor builds stress tests into their financial models, asking what would happen if interest rates rose by 1% or if the property sat empty for three months. Preparing for these "worst-case" scenarios is not pessimistic; it is professional. It demonstrates to lenders that you have considered the risks and have a plan to mitigate them, which is the hallmark of a sophisticated borrower.

Synthesizing the Investment Strategy

Securing property finance is a multi-dimensional challenge that requires you to be part accountant, part detective, and part negotiator. By mastering the tools of the trade—from the calculators that define your debt to the diverse range of lenders that populate the market—you remove the guesswork from the process. The goal is to move beyond the surface-level excitement of buying property and into the deeper, more rewarding work of building a sustainable financial engine. With a disciplined and analytical mindset, the complexities of the mortgage world become clear, predictable, and ultimately, manageable.

Success in this arena is a matter of preparation and persistence. When you treat your real estate journey as a data-driven business, doors begin to open. Whether you are working with established banks or seeking out new partnerships, your ability to present a clear, mathematically sound case will always be your greatest asset. Keep your records sharp, your debts low, and your analysis deep, and you will find that the path to a thriving real estate portfolio is well within your grasp.

Categories

Read More

Modern lifestyles can place significant pressure on men’s physical and mental well-being. Long working hours, stress, poor sleep, unhealthy eating habits, and reduced physical activity can all affect daily energy, stamina, confidence, and overall performance. Many men begin looking for natural solutions that may help restore vitality, improve endurance, and support healthy...

Many users are unaware that Netflix's content varies significantly across different countries, often discovering this only when traveling abroad and facing limited viewing options. This regional restriction means that the selection available in one location may be drastically different from another, leaving some viewers unable to access their favorite shows. Fortunately, there are methods to...

If you have a diamond and want to borrow money or sell it, its price can change a lot. A Diamond Pawn Shop gives you money based on how valuable your diamond is in the market. When diamond prices go up in the world, you get more money. When prices go down, you get less money. This guide explains in very simple words how diamond prices change and why timing matters when you go to...

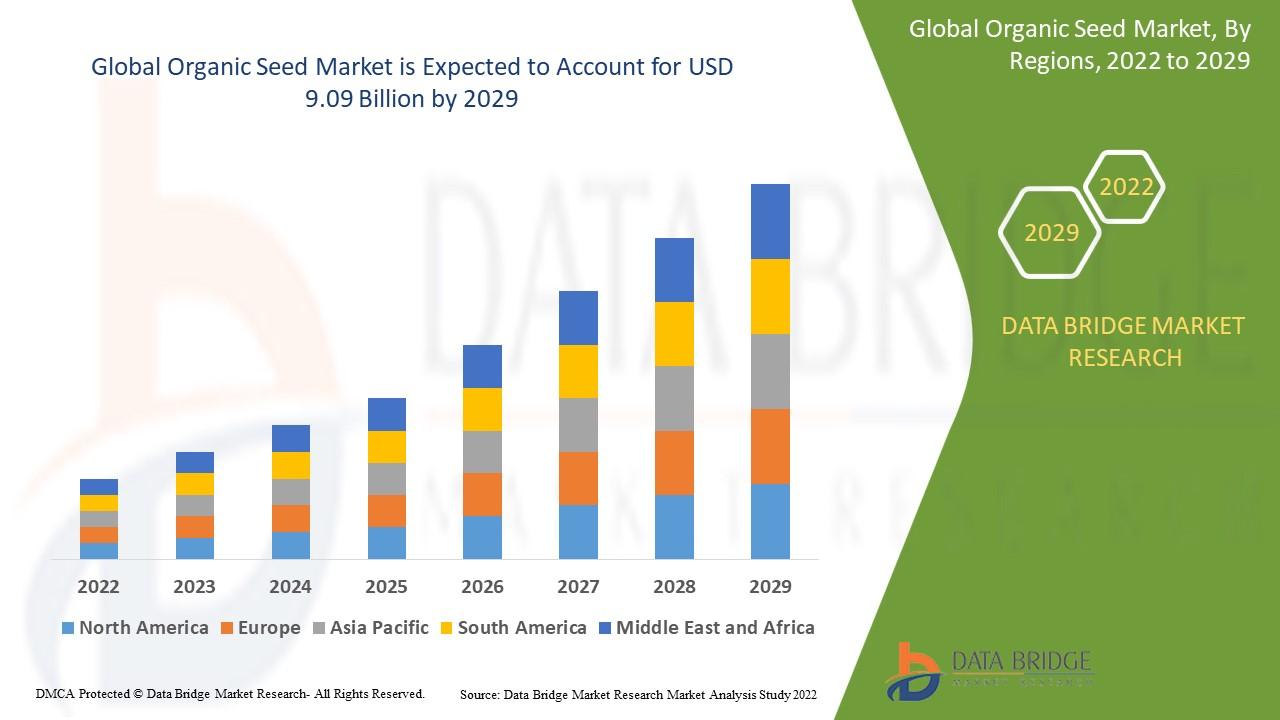

The organic seed market is experiencing robust expansion as consumers increasingly prioritize sustainable, chemical-free agriculture. Data Bridge Market Research analyses that the organic seed market was valued at USD 4.09 billion in 2021 and is expected to reach the value of USD 9.09 billion by 2029, at a CAGR of 10.50% during the forecast period. Organic seeds are produced without...

A violent incident unfolded at a Gamestop in Colma, California, resulting in a man sustaining multiple stab wounds and requiring hospitalization. The altercation took place early in the morning around 9:20 am on July 5 on Junipero Serra Boulevard. When police arrived, they found the injured individual with severe injuries, prompting immediate medical attention. According to authorities, the...