Helpful Insights for Successfully Completing the 203k Rehab Loan Process

Taking on a home renovation project is an exciting milestone, but it often requires a specialized financial approach to keep things running smoothly. One effective strategy for buyers looking at fixer-uppers is the 203k rehab loan, which allows you to roll the costs of improvements directly into your primary mortgage. This eliminates the need for high-interest credit cards or draining your personal savings to fix a leaky roof or an outdated electrical system. By planning ahead and understanding the nuances of this program, you can maximize your budget and ensure your renovation adds the most possible value to your property from day one.

Strategic Planning for Your Renovation

Success with a renovation mortgage starts long before the first hammer hits a nail. You need to assemble a team that understands the specific requirements of government-backed construction lending. This includes finding a lender who specializes in these products and a contractor who is comfortable with the paperwork and inspection schedules. Unlike a standard cash project, the funds are held in an escrow account and released as work is completed, so your contractor must be financially stable enough to start the work before the first draw is released.

Here is a quick reference for the two different paths you might take:

|

Project Detail |

The Limited Path |

The Standard Path |

|

Maximum Budget |

$35,000 in total costs |

No limit up to regional caps |

|

Structural Work |

Not permitted |

Full structural allowed |

|

Oversight Needs |

Self-managed or contractor |

HUD Consultant required |

|

Occupancy |

Must be livable during work |

Up to 6 months of payments can be financed |

Maximizing Your Buying Power

When you are out hunting for the perfect diamond in the rough, it is vital to keep an eye on the ceiling of what you can borrow. These figures known as fha limits are determined by the median house price in your specific county and are updated every year to keep pace with the real estate market. If you are shopping in an expensive coastal city, you will have a much higher ceiling than if you are looking in a rural township. Knowing these numbers prevents you from falling in love with a property that, after adding renovation costs, exceeds the maximum amount the government is willing to insure.

To help you stay on track during your search, consider these pro tips for property selection:

-

Always check the local county ceiling before making an offer on a distressed home.

-

Look for homes with "good bones" where cosmetic updates will yield the highest return on investment.

-

Ensure the total of the purchase price plus the renovation bid includes a 10-20% contingency reserve for unexpected issues.

-

Verify that the home is a one-to-four unit residential property, as commercial spaces do not qualify.

Preparing for the Inspection Phase

Before the loan is finalized, the property must undergo a rigorous evaluation. The fha appraisal requirements are significantly more detailed than a standard home inspection. The appraiser is looking for specific safety and health hazards that must be addressed in your renovation plan. If the house has peeling paint (in homes built before 1978), a broken furnace, or missing handrails, these items must be included in the contractor's bid. The goal is to ensure that once the renovation is complete, the home is safe, sound, and secure for its occupants.

The appraiser will perform two valuations: the "as-is" value and the "after-improved" value. This second number is crucial because it determines how much equity you are essentially creating through your hard work. By choosing projects that improve the "marketability" of the home—like adding a second bathroom or updating a cramped kitchen—you are more likely to see a favorable appraisal that supports your total loan amount.

Long-Term Financial Management

After the renovations are finished and you have successfully moved into your upgraded home, your financial strategy should shift toward long-term maintenance and equity growth. Eventually, market conditions might change, leading many to ask, can you refinance a fha loan to get a lower interest rate or remove the mortgage insurance? This is a common move for homeowners who have seen their property value skyrocket after a successful rehab. Transitioning into a conventional loan once you have 20% equity is a great way to lower your monthly overhead.

Keep these milestones in mind for your post-renovation journey:

-

Track your home’s value as local comparable sales increase in your neighborhood.

-

Maintain all receipts and permits from your 203k project to show future buyers or appraisers.

-

Consider a Streamline Refinance if rates drop but you aren't ready to move to a conventional loan.

-

Wait at least six months from your closing date before applying for a new mortgage.

Final Considerations for Success

A renovation loan is a marathon, not a sprint. It requires patience, meticulous documentation, and a clear vision of the end goal. By using these tips to manage your contractors, understand your borrowing limits, and prepare for the appraisal, you turn a potentially stressful process into a rewarding investment. The reward is a home tailored specifically to your needs, built on a solid financial foundation that provides security for years to come.

Categorieën

Read More

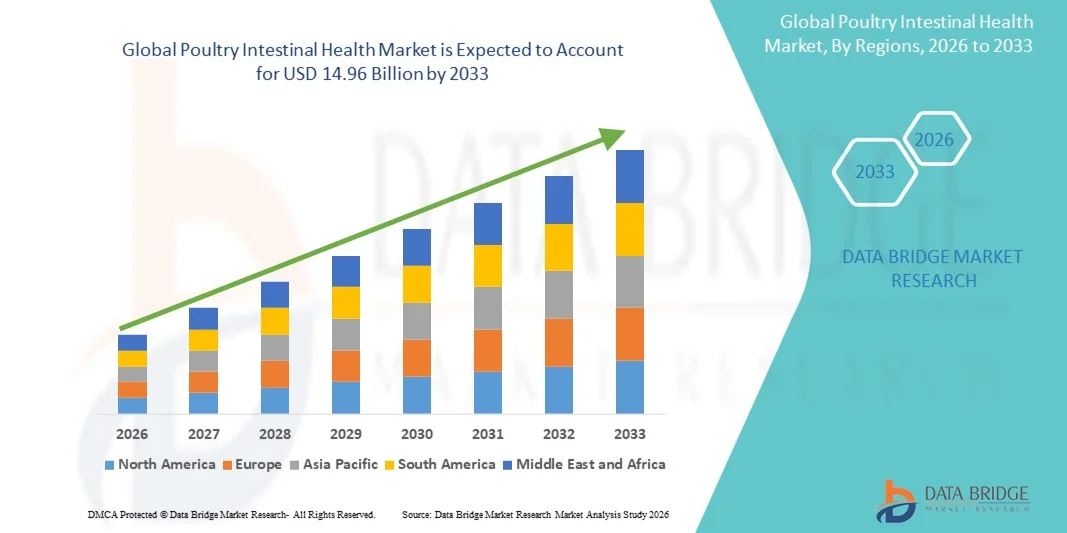

According to the latest report published by Data Bridge Market Research, the Poultry Intestinal Health Market The global poultry intestinal health market size was valued at USD 8.32 billion in 2025 and is expected to reach USD 14.96 billion by 2033, at a CAGR of 7.60% during the forecast period The market growth is largely fueled by the increasing...

In today’s fast-paced digital gaming environment, reliable customer support is essential for players to enjoy a seamless gaming experience. Sevengame, a leading online gaming platform, understands this need and offers a comprehensive range of customer support and help options to ensure that players can resolve their issues quickly and efficiently. Whether it is account-related queries,...

카지노 리워드 프로그램의 개념과 역할 온라인 카지노 시장이 지속적으로 성장하면서 다양한 리워드 프로그램이 이용자들의 관심을 받고 있다. 카지노 리워드 프로그램은 회원들의 활동에 따라 포인트와 보너스, 특별 혜택을 제공하는 고객 보상 시스템으로, 이용자의 만족도를 높이고 장기적인 관계를 형성하기 위한 중요한 서비스이다. 단순히 신규 가입 혜택을 제공하는 수준을 넘어 지속적인 플레이에 대한 보상을 제공한다는 점에서 많은 플랫폼이 적극적으로 운영하고 있다. 리워드 프로그램은 카지노 운영사와 이용자 모두에게 긍정적인 효과를 제공한다. 운영사는 충성도 높은 회원을 확보할 수 있으며, 이용자는 게임을 즐기는 과정에서 다양한 추가 혜택을 받을 수 있다. 이러한 구조는 온라인 카지노 산업에서 가장 널리...

Buying a used car in Dubai can feel exciting, stressful, and overwhelming all at once. The market is huge, the options are endless, and the prices vary from great bargains to suspicious deals. Whether you're a new resident, a long-time expat, or simply upgrading your ride, one thing is true: Dubai is one of the best places in the world to buy a used car. But it’s also a market where you...

Hiring the right staff is one of the biggest challenges in the restaurant industry. From busy kitchens to front-of-house service, every role needs skilled and dependable people. This is why many businesses now rely on the best restaurant hiring platforms to streamline recruitment and reduce time spent on finding qualified candidates. Why Restaurants Need Specialized Hiring Platforms Restaurants...