Important Milestones to Help You Secure an FHA Home Loan

Embarking on the journey to own a home can feel like a complex series of hurdles, but it is much easier when you have a clear roadmap. For many aspiring buyers in 2026, the various benefits of fha loan programs serve as the perfect starting point to bridge the gap between renting and owning. These government-backed options are specifically designed to be inclusive, ensuring that your financial past or a smaller savings account does not prevent you from securing a stable future for your family.

The process of getting your keys involves several logical phases, each bringing you closer to the finish line. By breaking the journey down into manageable segments, you can approach the market with confidence and clarity. Let's look at the specific progression from the initial research to long-term management of your new asset.

Phase One: Preparation and Initial Qualification

The first step is always about assessment. You need to understand where you stand financially before you start touring houses. Unlike more rigid traditional loans, this program looks for reasons to say yes rather than reasons to say no. Lenders will evaluate your income, your work history, and your current debt levels to determine your purchasing power.

|

Step |

Action Item |

Why It Matters |

|

1 |

Verify Credit Standing |

Scores as low as 580 allow for 3.5% down. |

|

2 |

Document Income |

Proves you can handle the monthly commitment. |

|

3 |

Review Debt-to-Income |

Ensures you aren't overextending your budget. |

|

4 |

Secure Pre-Approval |

Shows sellers you are a serious, ready buyer. |

Phase Two: Navigating the Purchase Process

Once you have a pre-approval in hand, you can begin the exciting part of the journey. When you find the right house, the focus shifts to the property itself. It is important to remember that the appraisal process for these loans is quite thorough, as it aims to protect the borrower by ensuring the home meets basic safety and habitability standards. This protects you from unforeseen structural or systemic issues shortly after moving in.

Closing the Deal Efficiently

During the final stages of the purchase, you will deal with closing costs and final inspections. A unique advantage here is that the program allows sellers or builders to contribute a significant portion of these costs. This means you can keep more of your hard-earned cash for things like moving expenses or emergency savings, rather than spending it all at the closing table.

Phase Three: Long-Term Asset Management

After you have settled into your home and started building equity, your financial strategy should continue to evolve. If you find that you need to access the value in your home for significant life goals—like major renovations or paying off high-interest student loans—you can look into an fha cash-out refinance. This milestone allows you to replace your existing mortgage with a new one, providing you with a lump sum of cash based on the equity you have accumulated. It is a powerful way to make your home work for you financially.

Adapting to Better Market Conditions

Financial landscapes change, and interest rates often dip. When this happens, you don't want to be stuck in a high-interest loan. The streamline refinance serves as a tool for homeowners to lower their monthly payments with incredible efficiency. This process is designed to be fast, often requiring no new appraisal and minimal documentation, provided you have a consistent history of on-time payments. It is the ultimate "maintenance" step for your mortgage.

Phase Four: Understanding Your Financial Foundation

As you manage your home over the years, you might find yourself explaining your choice to others. When someone asks what is an fha mortgage in plain English, you can describe it as a mortgage insured by the government. This insurance is the engine that drives the program's flexibility, giving lenders the confidence to offer lower down payments and more generous credit terms. It is the very reason why millions of people are able to move from a monthly rent check to a monthly investment in their own property.

-

Requires only 3.5% down for most credit profiles in 2026.

-

Allows for higher debt-to-income ratios than many private loans.

-

Offers fixed-rate stability for 15 or 30-year terms.

-

Provides a path for those with previous credit challenges to re-enter the market.

-

Appraisals include a safety check for the buyer's protection.

The Road to Financial Freedom

By following these steps, you are doing more than just buying a house; you are building a foundation for generational wealth. The key is to start with a clear understanding of the tools available and to use them strategically throughout your years as a homeowner. Whether it is the low entry cost at the beginning or the ability to lower your rate or access cash later on, these programs are built to support you at every turn.

Homeownership is a marathon, not a sprint. By utilizing a financing path that prioritizes accessibility and long-term flexibility, you are giving yourself a massive advantage. You don't need to be a financial expert to succeed; you just need to follow the milestones and work with professionals who can guide you through the specifics of each phase. Your future self will thank you for making the move today.

Categories

Read More

Detailed Analysis of Executive Summary Sheet Metal Market Size and Share The global sheet metal market size was valued at USD 339.78 billion in 2024 and is projected to reach USD 490.65 billion by 2032, with a CAGR of 4.70% during the forecast period of 2025 to 2032. In the universal Sheet Metal Market research report, global, local and regional level is considered to know the...

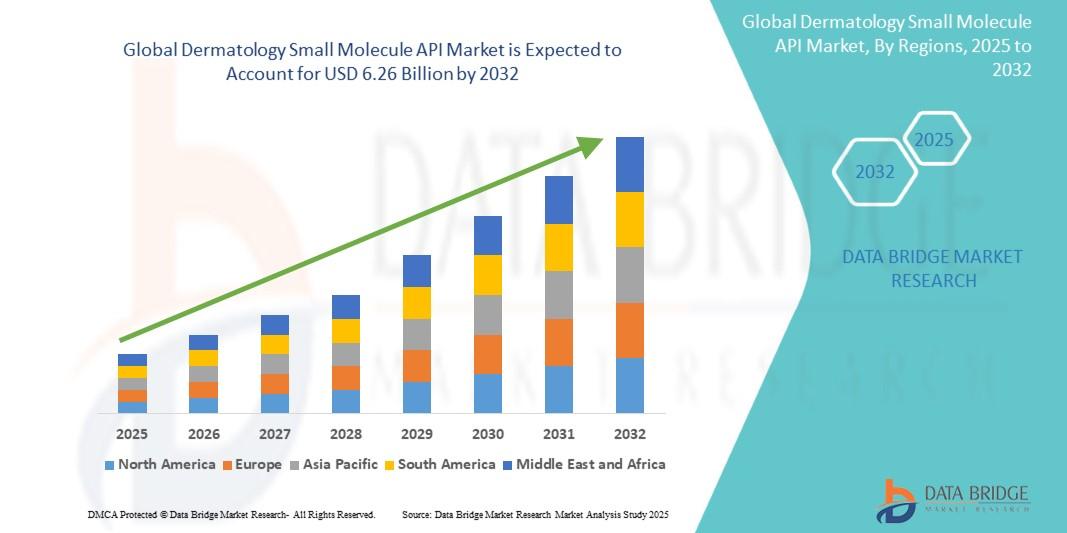

Dermatology small molecule active pharmaceutical ingredients (APIs) are low molecular weight compounds designed to target specific biological pathways for treating skin conditions. The global dermatology small molecule API market size was valued at USD 3.64 billion in 2024 and is projected to reach USD 6.26 billion by 2032, with a CAGR of 7.00% during the forecast period of 2025 to...

Live match betting has become one of the most exciting parts of modern sports betting. Unlike traditional betting, where users place their bets before a match starts, live betting allows players to place wagers while the match is in progress. This dynamic form of betting has attracted millions of sports fans who enjoy predicting outcomes based on real-time match situations. To participate in...

As per Market Research Future analysis, the Darts Market Size was estimated at 6.162 USD Billion in 2024. The Darts industry is projected to grow from 6.423 USD Billion in 2025 to 9.732 USD Billion by 2035, exhibiting a compound annual growth rate (CAGR) of 4.24% during the forecast period 2025 - 2035 The darts market is witnessing growth driven by increasing interest in competitive...

Saudi Arabia stands tall in the Middle East. Its economy once leaned heavy on oil. Now, it turns to fresh ideas. Innovation labs lead this charge. They spark new ways to handle money. Think fintech apps that pay bills in seconds. Or AI tools that spot smart investments. These labs test bold ideas safely. They help build a future where finance grows fast and fair. Vision 2030 drives it all. This...