Decoding the Industrial Defense: The Operational Technology Security Market Share Dynamics

The global Operational Technology Security Market Share is a highly specialized and rapidly consolidating competitive landscape. Unlike the broader IT cybersecurity market, which is fragmented into dozens of sub-segments, the core OT security market for network visibility and threat detection is dominated by a handful of pure-play vendors who were early pioneers in this space. Market share is being won by those companies that can demonstrate the deepest understanding of proprietary industrial protocols, provide the most comprehensive asset discovery, and offer the most accurate and context-aware threat detection with the fewest false positives. The competitive dynamic is also being shaped by a wave of acquisitions, as large IT security and industrial automation giants are buying up these specialized OT security startups to quickly enter the market and offer a more integrated solution to their existing customer base.

A dominant portion of the market share is held by a group of specialized, pure-play OT security vendors. Companies like Dragos, Claroty, and Nozomi Networks are widely recognized as the leaders in the space. These companies were founded specifically to address the unique challenges of securing industrial control systems. Their market share is built on the strength of their technology, particularly their deep expertise in decoding a vast array of proprietary industrial protocols and their ability to provide rich, context-aware insights into OT network behavior. They have established a strong first-mover advantage and have secured contracts with many of the world's largest industrial and critical infrastructure organizations. Their focus and deep domain knowledge give them a powerful competitive advantage over more generalist security vendors who may not understand the unique nuances and safety-critical nature of OT environments.

Another significant and growing share of the market is being captured by the major IT security platform vendors who are extending their offerings into the OT space. Companies like Fortinet, Palo Alto Networks, and Cisco have all made major pushes into OT security. Their strategy is often twofold. First, they have developed ruggedized versions of their firewalls specifically for industrial environments, allowing for secure network segmentation between IT and OT. Second, they are increasingly acquiring or partnering with the specialized OT visibility vendors to integrate OT threat detection capabilities into their broader security platforms (e.g., their XDR or SIEM solutions). Their key advantage is their massive existing customer base and their ability to offer a single, consolidated security platform that can provide visibility across both the IT and OT environments. For many organizations, the prospect of a single vendor solution is highly attractive, making these IT giants formidable competitors.

The traditional industrial automation vendors, such as Siemens, Schneider Electric, Honeywell, and Rockwell Automation, are also key players and hold a unique position in the market. They have an unparalleled understanding of the industrial processes and the control systems they manufacture. Their market share strategy is to build security directly into their own products and to offer a suite of security services and solutions designed to protect their own ecosystem of devices. They often partner with the specialized OT security software vendors to provide a complete solution to their customers. Their key advantage is their trusted relationship with the plant managers and control engineers who operate their equipment. While they may not have the deep cybersecurity expertise of a pure-play vendor, their intimate knowledge of the underlying industrial systems gives them immense credibility and a strong channel to market, making them a crucial part of the competitive landscape.

Explore More Like This in Our Regional Reports:

Kategoriler

Read More

" According to the latest report published by Data Bridge Market Research, the Hazelnut Meal Market The global hazelnut meal market size was valued at USD 730.76 million in 2024 and is expected to reach USD 1182.42 million by 2032, at a CAGR of 6.20% during the forecast period. Hazelnut Meal Market report is a great option to achieve current as well as upcoming technical...

Let's cut through the hype, shall we, and speak plainly. You, as a business owner, are not obsessed with your website. Please, hear me out, before you decide to go all in on the DIY website building approach. I'm not knocking amateurs out of existence here, but the cheapest and easiest solutions such as Wix or Squarespace tend to show at a glance what their capabilities are. Your customers will...

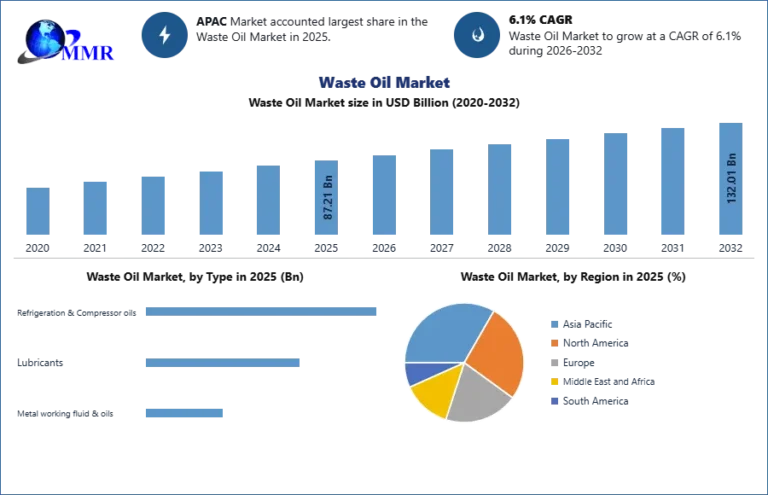

Market OverviewThe global Waste Oil Market is experiencing steady expansion, driven by increasing adoption of advanced recycling technologies and strong regulatory support for sustainable waste management. The market is expected to grow at a notable CAGR during the forecast period, supported by rising environmental awareness and the need for efficient disposal and reuse of used oils.Waste oil...

Atunci când alegi finisajele pentru locuință, una dintre cele mai importante decizii este alegerea tipului de gresie. Mulți clienți care vizitează showroom-urile CeraMall se întreabă ce înseamnă gresie rectificata și care sunt diferențele reale dintre aceasta și gresia nerectificată. Deși la prima vedere pot părea similare, există câteva aspecte importante care...

Modern weight-loss problems are no longer caused only by eating too much. They are strongly connected to dehydration, toxin buildup, slow metabolism, poor digestion, and inflammation. Many people diet, exercise, and still struggle with stubborn fat, bloating, and low energy. This is where AquaFit changes the game. AquaFit is a natural hydration-based weight-management formula designed...