Key Insights into the COE for VA Loan Requirements that Every Veteran Should Know

The journey toward homeownership for veterans and active-duty service members often begins with a specific piece of paperwork that serves as the foundation for the entire mortgage process. Securing a coe for va loan eligibility is the primary requirement that confirms to a private lender that you have met the minimum service requirements set by the Department of Veterans Affairs. This document is not merely a formality; it is a verification of your dedicated service and the key that unlocks a suite of financial advantages designed specifically for the military community. By obtaining this certificate, you provide the necessary evidence that the government is willing to guarantee a portion of your mortgage, which in turn allows lenders to offer more favorable terms, including the absence of a traditional down payment requirement.

The educational value of this program lies in how it bridges the gap between service and civilian stability. When you transition from the military or move between duty stations, having a guaranteed path to a primary residence is a significant stress reliever. However, the system is governed by specific rules and terminology that can seem like a foreign language to those who aren't familiar with the nuances of federal housing policy. Learning how these components work together ensures that you can maximize the benefits you have earned through your time in uniform. From understanding how eligibility is calculated to knowing how much of your benefit remains after a previous purchase, education is the best tool for any veteran house hunter in the current real estate market.

The Mechanics of Federal Guaranty

One of the most important concepts to master is how the government actually supports your loan. The Department of Veterans Affairs does not hand out the cash directly; instead, it provides a promise to your bank. If you were to ever fall behind on payments to the point of foreclosure, the government would pay the lender a specific portion of the loss. This safety net is what makes the zero-down payment option possible. For many veterans, this benefit is not limited to a single use. If you have already used your benefit and still own that home, you may be eligible to use va second tier entitlement for your next purchase. This additional layer of coverage is what allows service members to keep a current residence as a rental property while buying a new home at their next location.

To calculate how much of this secondary benefit you have available, you generally look at the current housing limits and subtract the amount of entitlement you have already used on your existing property. In 2026, these limits have been adjusted to reflect the rising costs of housing nationwide. By understanding that your entitlement is divided into two tiers, you can see that the program is designed to grow with you as your real estate needs change over time. It is a sophisticated financial structure that provides more flexibility than almost any other mortgage product available today, provided you have a clear understanding of your remaining balance and how it applies to your new purchase price.

Understanding Borrowing Thresholds

A common point of confusion in the veteran community involves the total amount one can borrow. It is a widespread myth that there is a strict, national va loan maximum that applies to every single borrower regardless of their situation. In reality, for those who have their full entitlement available—meaning they have never used a VA loan before or have fully restored their benefit—the government does not place a cap on the loan amount for which they will provide a guaranty. This means if you can qualify based on your income and credit score, you could technically borrow a very large sum with no money down. This policy ensures that veterans are not priced out of high-cost markets where home values far exceed the national average.

However, if you are using your entitlement for a second time while still holding another loan, or if you have had a past foreclosure, some limits do come back into play. In these scenarios, the lender uses the conforming loan limits set by the Federal Housing Finance Agency to determine your zero-down buying power. In most parts of the country for 2026, the baseline limit for a single-family home has increased significantly. Knowing these figures is essential because they dictate whether you will need to bring any cash to the closing table to cover the portion of the loan that the VA won't guarantee. Education on these limits prevents surprises when you are deep in the negotiation phase of a home purchase.

Navigating the Financials of Closing

While the elimination of a down payment is a massive advantage, it does not mean there are zero costs involved in the transaction. Every home buyer should be prepared to handle the closing cost for va loans to ensure a successful transition into their new property. These costs represent the various fees required to finalize the legal and financial aspects of the deal. They typically include the appraisal fee, title search fees, credit report charges, and local recording fees. One unique cost associated with this program is the VA Funding Fee, which is a percentage of the loan amount paid to the government to help the program stay self-sustaining. This fee varies based on your service status and whether you are a first-time or repeat user of the benefit.

Fortunately, the program offers several ways to mitigate these expenses. For starters, veterans with a service-connected disability rating of 10% or more are usually exempt from the funding fee entirely. Additionally, the VA allows for seller concessions up to 4% of the total purchase price. This means you can negotiate with the person selling the home to have them cover many of your out-of-pocket expenses. In a balanced or buyer-friendly market, it is quite common for a veteran to walk away from a closing with very little of their own money spent. Understanding how these pieces fit together—from the initial certificate to the final settlement statement—allows you to plan your finances with precision and confidence.

Property Standards and Long-Term Value

The educational journey also involves understanding the Minimum Property Requirements (MPRs) set by the VA. These are not meant to be hurdles but are safeguards for you, the veteran. The government wants to ensure that the home you buy is safe, structurally sound, and sanitary. This means an appraiser will look for issues like peeling lead-based paint, faulty wiring, or a roof that is near the end of its life. While this might occasionally disqualify a "fixer-upper" from being purchased with a standard VA loan, it ensures that your new home won't become a financial burden due to immediate, massive repairs.

If repairs are needed, they must generally be completed before the loan can close. This often prompts sellers to fix issues they might otherwise have ignored. By learning about these standards, you can better select properties that are likely to pass inspection, making the process much smoother for everyone involved. It is an educational step that protects your investment from day one. When you combine this with the low interest rates and flexible credit requirements, the value proposition of the VA program becomes clear. It is a comprehensive system designed to set you up for long-term stability rather than just a one-time transaction.

Strategic Financial Planning

Finally, it is worth noting that your housing benefit is a tool for building wealth. Because you aren't tying up all your liquid cash in a down payment, you have the opportunity to invest that money elsewhere, whether in an emergency fund, a retirement account, or home improvements that increase equity. The program also offers the Interest Rate Reduction Refinance Loan (IRRRL) for when market conditions change. This "streamline" refinance allows you to lower your monthly payment with minimal documentation if rates drop in the future. It is a feature that keeps on giving long after the initial move-in date.

Education is the key to unlocking these doors. By taking the time to understand the nuances of the certificate of eligibility, the layers of entitlement, and the reality of the closing process, you position yourself as a savvy consumer in a competitive market. The 2026 real estate landscape requires this level of preparation. Armed with the right information and a supportive team of professionals who understand military life, you can navigate the path to homeownership with the same discipline and success that defined your time in the service. Your home is more than just a roof; it is a reward for your sacrifice, and understanding the mechanics of that reward is the first step to securing your future.

Categories

Read More

Metaverse Gaming Trends: Shaping the Future of Immersive Digital Entertainment Metaverse gaming is rapidly emerging as one of the most transformative trends in the global gaming industry, combining immersive technologies such as virtual reality (VR), augmented reality (AR), blockchain, and artificial intelligence (AI). These innovations are redefining how players interact, socialize, and...

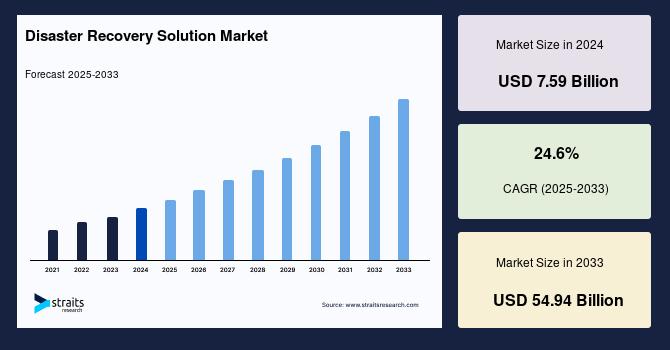

Disaster Recovery Solution Industry Insights: Straits Research recently introduced the latest update on the Disaster Recovery Solution Market that provides an extensive outlook of the market, analyzing key growth opportunities, challenges, risk factors, and emerging trends across diverse geographic regions. The report offers a definitive and meticulous analysis of the Disaster...

Video-Based People Counters: Transforming Footfall Intelligence with Smart Surveillance Video-based people counters are rapidly becoming a cornerstone of modern analytics systems used in retail, transportation hubs, smart buildings, and public infrastructure. By leveraging computer vision and artificial intelligence (AI), these systems convert standard video feeds into actionable data on...

Executive Summary Hydroxypropyl Methylcellulose (HPMC) Market: Growth Trends and Share Breakdown Hydroxypropyl methylcellulose (HPMC) market size is expected to grow at a compound annual growth rate of 3.38% for the forecast period of 2021 to 2028 and is likely to reach USD 5.92 billion by 2028. This global Hydroxypropyl Methylcellulose (HPMC) Market research report conducts a...

A busca por plataformas confiáveis, rápidas e envolventes no universo das apostas online cresce a cada dia. Com tantas opções disponíveis, encontrar um ambiente que combine segurança, facilidade de uso e entretenimento de qualidade faz toda a diferença. É exatamente isso que a 74BET oferece: uma solução moderna,...