Steps to Secure Your Future Home with Form 26-1880

Taking the first leap into homeownership after your time in the service is a transformative moment that requires a clear plan of action. While the process can feel overwhelming, it is essentially a series of small, manageable milestones that lead to your new front door. Your journey officially begins the moment you decide to organize your documentation, starting with the submission of form 26-1880 to the Department of Veterans Affairs. This critical first step allows the government to verify your eligibility and issue the Certificate of Eligibility (COE) that acts as the foundation for your entire mortgage application.

Establishing Your Foundation

Once you have initiated the paperwork, you should take a moment to understand exactly what is va entitlement and how it will influence your purchasing power. This is essentially a government-backed guarantee provided to your lender, promising to cover a portion of the loan if you were to default. In practical terms, this means the bank can offer you a mortgage with no down payment because the federal government is providing the safety net that a traditional cash deposit would normally offer.

The next step in this phase is to connect with a lender who understands the nuances of military benefits. Not all banks are created equal, and finding one that specializes in these types of loans can make the transition much smoother. They will use the information from your COE to determine your "basic" and "bonus" levels of support, ensuring that you have the maximum financial backing available for the price range you are targeting.

Phase One: The Documentation Checklist

Before you dive into house hunting, ensure you have these essential items organized. Having these ready will prevent delays once you find a property you love.

|

Step Number |

Required Action |

Why It Is Critical |

|

1 |

Retrieve your DD-214 |

Proves your dates and type of discharge. |

|

2 |

Submit Form 26-1880 |

Triggers the issuance of your Certificate of Eligibility. |

|

3 |

Verify Disability Rating |

Can lead to a waiver of the VA Funding Fee. |

|

4 |

Obtain Pre-Approval |

Gives you a clear budget before you start shopping. |

Navigating the Financial Transition

With your pre-approval in hand, you can begin the exciting process of touring homes and making offers. As you enter this stage, it is important to budget for the closing cost on va loan requirements that will arise at the end of the transaction. While your down payment is zero, you will still encounter third-party fees for things like the home appraisal, title insurance, and state recording fees. Typically, these costs range between 3% and 5% of the total purchase price.

A strategic step here is to work with your real estate agent to negotiate "seller concessions." In many markets, you can ask the seller to pay all of your standard closing costs, which significantly reduces the amount of cash you need to bring to the signing table. Additionally, you may choose to pay "discount points" at this stage—a move where you pay a bit more upfront to lock in a lower interest rate for the next thirty years, saving you a fortune in the long run.

Phase Two: Budgeting and Negotiation

This table breaks down how to handle the different financial components you will face during the negotiation and closing phase.

|

Financial Item |

Standard Range |

Strategy for Veterans |

|

Appraisal Fee |

$600 – $1,200 |

VA appraisers ensure the home is safe and worth the price. |

|

Title Insurance |

$500 – $2,000 |

Protects you against legal claims to the property. |

|

VA Funding Fee |

1.25% – 3.3% |

Can be rolled into the loan or waived for disability. |

|

Origination Fee |

Capped at 1% |

Shop lenders to see who offers the lowest overhead. |

Finalizing Your Purchase

As you move toward the final signing, you might find yourself looking at homes that are higher in price than the average. Many buyers worry about a va loan max amount that might limit their options in expensive neighborhoods. In 2026, the reality is that if you have your full benefit available, the government does not set a hard ceiling on your loan amount. Your limit is now primarily determined by what your income can support and what the lender is willing to offer based on your credit profile.

The final step is the "Clear to Close" notification from your lender. This means all your financial data has been double-checked, the appraisal has come back at the right value, and your eligibility has been confirmed one last time. You will meet with a notary or a closing attorney to sign the final stack of documents, and shortly after, you will receive the keys. By following these structured steps—from that first eligibility form to the final handshake—you turn the dream of homeownership into a stable, sustainable reality for you and your family.

Every step you take is a tribute to the time you spent in uniform. This program was built to ensure that those who served have a fair shot at the American dream without the high hurdles that often stop others. Stay patient through the paperwork, be proactive with your lender, and keep your eyes on the finish line. You have earned this benefit, and now it is time to use it to build a place where you can truly feel at home.

Kategoriler

Read More

According to the latest report published by Data Bridge Market Research, the Krabbe Market CAGR Value Thorough and transparent research studies conducted by a team work of experts in their own domain accomplish this global Krabbe Market research report. The report is valuable for both customary and emerging market players in the industry and provides in-depth market...

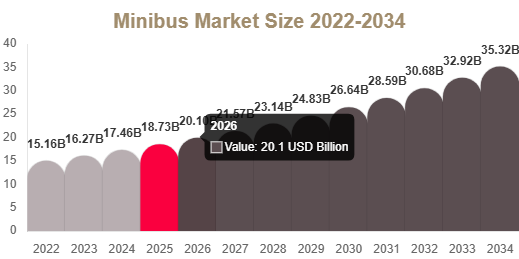

Market Overview The minibus market is expanding steadily due to increasing demand for cost-effective passenger transportation, growing tourism activities, and rising adoption of shared mobility solutions. Minibuses are widely used in urban transport, school transportation, corporate shuttle services, and tourism operations due to their flexibility and lower operational cost compared to...

"Neuraminidase Inhibitors Market Summary: According to the latest report published by Data Bridge Market Research, the Neuraminidase Inhibitors Market The global neuraminidase inhibitors market size was valued at USD 305.50 Million in 2025 and is expected to reach USD 654.86 Million by 2033, at a CAGR of 10.00% during the forecast period Today’s businesses are more inclined...

A properly functioning toilet is essential to the comfort and convenience of any home. Over time, even the best toilets can experience wear and tear from daily use. Leaky tanks, weak flushes, or running water can cause unnecessary frustration and waste. The good news is that you don’t always need to replace the entire toilet to fix these issues. With genuine Glacier Bay toilet parts, you...

The WTK Price Trend has become an important focus area for manufacturers, procurement managers, and supply chain professionals in the pulp and paper industry. Over the past few quarters, the market has experienced noticeable fluctuations driven by changes in raw material costs, logistics conditions, and evolving demand patterns. Understanding the behavior of WTK Prices helps businesses make...