How a 401(k) Hardship Withdrawal Can Help During Financial Hardship

Unexpected financial emergencies can place significant pressure on your savings and long-term financial plans. For some individuals, a 401(k) hardship withdrawal may seem like the quickest solution when facing urgent expenses. While these withdrawals provide access to retirement funds during difficult times, they can also have lasting effects on retirement savings and tax obligations.

Understanding how a 401(k) hardship withdrawal works, its tax consequences, and its impact on future retirement goals is essential before making a decision.

What Is a 401(k) Hardship Withdrawal?

A 401(k) hardship withdrawal allows participants to withdraw money from their retirement account to cover an immediate and heavy financial need. Unlike a 401(k) loan, hardship withdrawals are not repaid to the retirement plan.

The IRS permits hardship withdrawals for specific qualifying expenses, including:

- Certain medical expenses

- Costs related to purchasing a primary residence

- Tuition and educational fees

- Payments necessary to prevent eviction or foreclosure

- Funeral expenses

- Certain home repair costs resulting from disasters

Employers may have additional requirements, and not every 401(k) plan offers hardship withdrawal options. Participants should review their plan documents before submitting a request.

How Hardship Withdrawals Reduce Retirement Savings

One of the biggest drawbacks of a hardship withdrawal is the immediate reduction in retirement assets.

When money is withdrawn from a 401(k), those funds no longer benefit from potential market growth, compound interest, or employer-sponsored retirement investment opportunities.

For example, if a participant withdraws $15,000 at age 35, that amount could have potentially grown significantly by retirement age. Assuming an average annual return of 7%, that $15,000 could have grown to more than $80,000 over 25 years.

This illustrates how even a relatively small withdrawal can create a substantial gap in retirement savings over time.

Loss of Compound Growth

Compound growth is one of the most powerful advantages of retirement investing. Every dollar removed from a retirement account loses the opportunity to generate future earnings.

As a result, hardship withdrawals can:

- Reduce long-term retirement wealth

- Delay retirement goals

- Increase reliance on Social Security or other income sources

- Require larger future contributions to make up for lost savings

The younger the participant, the greater the potential long-term impact because there is more time for investments to grow.

Tax Implications of a 401(k) Hardship Withdrawal

A hardship withdrawal may solve an immediate financial problem, but it often creates a tax liability.

Traditional 401(k) contributions are generally made using pre-tax dollars. Therefore, money withdrawn from the account is usually treated as taxable income during the year of withdrawal.

Federal Income Taxes

The withdrawn amount is added to the participant's taxable income.

For example:

- Annual salary: $70,000

- Hardship withdrawal: $20,000

- Taxable income increases to approximately $90,000

This increase may push the taxpayer into a higher tax bracket or result in a larger tax bill when filing a federal income tax return.

State Income Taxes

Depending on where the taxpayer lives, state income taxes may also apply.

Some states fully tax retirement distributions, while others provide exemptions or reduced taxation. Understanding local tax rules is important before requesting a withdrawal.

Mandatory Tax Withholding

Many retirement plan administrators withhold a portion of hardship withdrawals for federal taxes.

However, withholding may not fully cover the actual tax liability. Participants could still owe additional taxes when filing their annual return.

Early Withdrawal Penalties

Historically, individuals younger than age 59½ often faced a 10% early withdrawal penalty on hardship distributions.

While recent retirement plan changes have expanded hardship withdrawal flexibility, penalty rules may still apply depending on the specific circumstances and withdrawal type.

For example, a participant taking a $10,000 withdrawal could potentially face:

- Federal income taxes

- State income taxes

- Additional penalties if applicable

This means the actual amount received may be considerably less than the amount withdrawn from the account.

Because retirement plan rules continue to evolve, participants should review current IRS guidance and consult a qualified tax professional before proceeding.

Impact on Future Retirement Contributions

Another often-overlooked consequence of hardship withdrawals is the effect on future retirement planning.

Many individuals who withdraw retirement funds during a financial crisis struggle to replenish those savings later. Increased living expenses, debt obligations, or other financial pressures may make it difficult to increase future contributions.

As a result, participants may experience:

- Lower retirement account balances

- Reduced investment growth

- Greater retirement funding gaps

- Increased financial stress later in life

To recover from a hardship withdrawal, individuals may need to:

- Increase salary deferrals

- Maximize employer matching contributions

- Utilize catch-up contributions when eligible

- Create a long-term savings recovery plan

Situations Where a Hardship Withdrawal May Make Sense

Despite the drawbacks, hardship withdrawals can provide necessary financial relief in certain situations.

Examples include:

Significant Medical Expenses

Unexpected healthcare costs can quickly become overwhelming. Accessing retirement funds may help cover critical treatments or emergency procedures.

Preventing Foreclosure or Eviction

Protecting a primary residence may justify the use of retirement savings when other options are unavailable.

Disaster Recovery

Natural disasters, severe property damage, or emergency repairs may create immediate financial needs that exceed available cash reserves.

Educational Emergencies

Certain tuition and educational expenses may qualify under plan rules and provide short-term financial assistance.

Even in these situations, individuals should carefully evaluate alternatives before withdrawing retirement funds.

Alternatives to a Hardship Withdrawal

Before tapping retirement savings, consider other options that may have less impact on long-term financial security.

Possible alternatives include:

- Emergency savings accounts

- Personal loans

- Home equity financing

- Payment plans with medical providers

- Temporary expense reductions

- Assistance programs

- 401(k) loans, if permitted by the employer's plan

A 401(k) loan may be preferable in some cases because the borrowed amount can typically be repaid to the retirement account, reducing long-term damage to retirement savings.

However, every option carries risks and should be evaluated carefully.

Tips for Minimizing Financial Damage

If a hardship withdrawal is unavoidable, consider strategies to reduce its impact:

- Withdraw only the amount necessary to meet the immediate need.

- Understand all tax consequences before requesting funds.

- Continue contributing to retirement accounts whenever possible.

- Increase contributions after the financial emergency passes.

- Maintain a dedicated emergency fund for future unexpected expenses.

- Seek advice from a financial advisor or tax professional.

Taking proactive steps can help rebuild retirement savings and reduce long-term financial setbacks.

Conclusion

A 401(k) hardship withdrawal can provide much-needed financial support during emergencies, but it comes with important trade-offs. Withdrawn funds lose the opportunity for future growth, potentially reducing retirement income and delaying long-term financial goals. In addition, hardship withdrawals may trigger federal and state income taxes and, in some cases, additional penalties.

Before accessing retirement savings, individuals should carefully assess all available alternatives and fully understand the financial consequences. While hardship withdrawals can offer short-term relief, preserving retirement assets whenever possible remains one of the best strategies for long-term financial security.

Categorieën

Read More

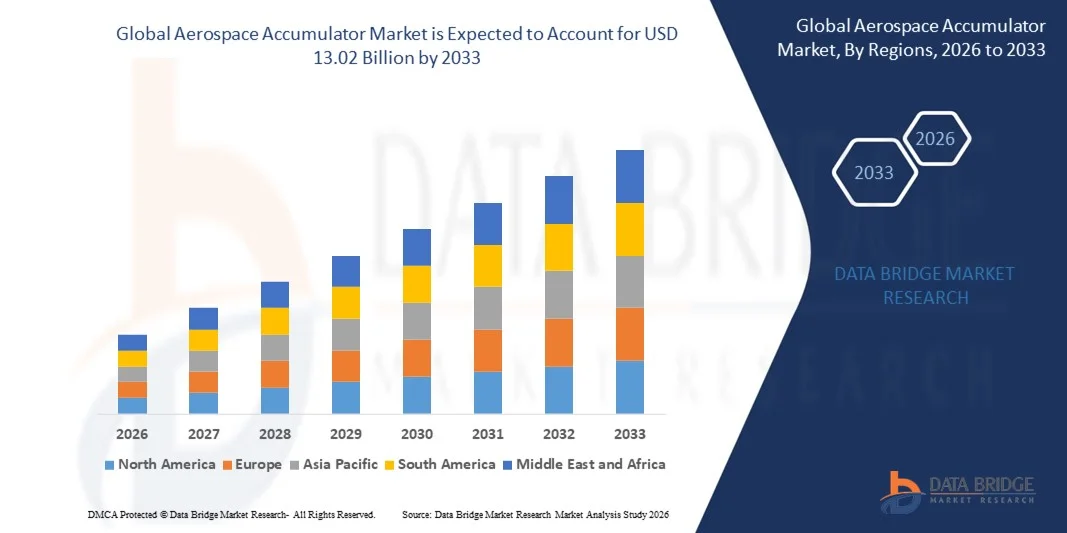

According to the latest report published by Data Bridge Market Research, the Aerospace Accumulator Market The global aerospace accumulator market size was valued at USD 9.89 billion in 2025 and is expected to reach USD 13.02 billion by 2033, at a CAGR of 3.50% during the forecast period. The wide ranging Aerospace Accumulator Market report provides...

Lakme Academy Powered by Aptech, Lal Koti is among the most trusted institutions in Jaipur for beauty education, providing professional and career-centric courses. If your aim is to make your career in the beauty and fashion sector, our Makeup Course in Jaipur will help you gain experience in makeup through professional techniques, products, and processes. If you aspire to be a professional...

How Digital Permit-to-Work Systems Strengthen Control Over High-Risk Activities Authorizing hazardous work should never be viewed as a routine step or reduced to a simple act of signing a form. Every permit represents a conscious decision that determines whether a task will proceed safely or introduce avoidable risk to people, equipment, and ongoing operations. The Permit-to-Work (PTW)...

According to the latest report published by Data Bridge Market Research, the Carbon Footprint Management Market CAGR Value DBMR team uses simple language and easy to understand statistical images to provide thorough information and in-depth data on the Carbon Footprint Management Market industry and Carbon Footprint Management Market. The company profiles of all the key...

Online gambling programs have become significantly common, and Domino8 is one of many titles frequently looked by consumers enthusiastic about on the web card and domino games. If you are new and desire to know how the subscription method works, this guide can help you understand everything about Daftar Domino8 in an easy and distinct way. What is Domino8? Daftar Domino8 is an on the web...