How Does India Health Insurance Benefit NRIs Living in the United Kingdom?

For Non-Resident Indians (NRIs) settled in the United Kingdom, the dual-lifestyle dynamic creates a unique set of financial and healthcare challenges that the National Health Service (NHS) cannot always address. While the UK provides a comprehensive public health safety net, the reality of maintaining deep-rooted connections in India often necessitates a parallel healthcare strategy. As medical inflation in the Indian private sector continues to outpace general inflation, often hovering around 14 percent annually, the strategic acquisition of a domestic policy is becoming a cornerstone of prudent financial planning for the diaspora.

Securing India health insurance is no longer merely an optional safety measure for those visiting home; it is a sophisticated tool for asset protection and ensuring high-velocity access to world-class medical facilities. For the UK-based NRI, the benefits extend beyond simple reimbursement, touching upon tax efficiency, care for ageing parents, and the seamless continuity of healthcare across borders.

Bridging the Gap Between the NHS and Private Care

The NHS is renowned for its clinical excellence, yet it is often characterised by significant waiting times for elective procedures and specialist consultations. For many NRIs, the ability to fly to India and receive immediate surgical intervention or specialist diagnostic care is a major advantage. However, without a local policy, the cost of top-tier private healthcare in Indian metropolitan cities can be prohibitively high when paid out-of-pocket.

By maintaining India health insurance, UK residents can bypass the queues of the UK public system for non-emergency treatments, such as elective orthopaedic surgeries, advanced ophthalmology, or comprehensive health screenings. This allows for a more flexible approach to personal health management, where one can choose the best of both worlds: the emergency and primary care of the UK and the rapid-access, high-tech elective care of India.

Financial Efficiency and the Role of NRI Accounts

One of the most compelling reasons for an NRI to hold a domestic policy involves the financial regulations surrounding cross-border payments and claims. Under the Foreign Exchange Management Act (FEMA), NRIs are encouraged to manage their Indian liabilities through NRE (Non-Resident External) or NRO (Non-Resident Ordinary) accounts.

When an NRI pays for a policy using an NRE account, they ensure that any future claim payouts are easily manageable and, in some instances, repatriable. Furthermore, many Indian insurers have tailored their digital interfaces to accept international premium payments seamlessly. This financial integration ensures that in the event of a medical emergency during a visit to India, the policyholder does not need to navigate the complexities of international wire transfers or currency fluctuations to settle hospital bills.

Tax Advantages Under Section 80D

Even for those living in the UK, the Indian tax code offers significant incentives for maintaining health cover. If an NRI has any form of taxable income in India, such as rental income from property or dividends from Indian shares, they can claim deductions under Section 80D of the Income Tax Act.

-

Self and Family: Deductions of up to ₹25,000 for premiums paid for self, spouse, and dependent children.

-

Parents: An additional deduction of up to ₹50,000 if the parents are senior citizens.

This makes the effective cost of the policy much lower while providing a robust financial shield for the family.

Comprehensive Coverage for Ageing Parents

Perhaps the most significant benefit of India health insurance for the UK diaspora is the peace of mind regarding parents left behind. Distance often compounds the anxiety of a medical crisis. A comprehensive policy ensures that parents have access to the best hospitals without the NRI child needing to be physically present to arrange finances immediately.

Modern policies offer features like 'Cashless Hospitalisation', where the insurer settles the bill directly with the hospital. This is a critical lifeline for elderly parents who may find it difficult to manage the paperwork and reimbursement process on their own. Insurers like Niva Bupa have developed extensive networks across both Tier 1 and Tier 2 cities, ensuring that high-quality care is accessible even in smaller hometowns.

Continuity of Care and the Repatriation Factor

Many NRIs in the UK eventually consider a 'return to roots' or a partial retirement back in India. Health insurance premiums are heavily dependent on the age at which the policy is first purchased. By starting a policy while still resident in the UK, an NRI can lock in lower premiums and, more importantly, complete the mandatory waiting periods for pre-existing diseases.

Navigating Waiting Periods

Most Indian policies have a waiting period of 2 to 4 years for pre-existing conditions like diabetes, hypertension, or cardiac issues. If an NRI waits until they relocate to India to buy insurance, they may find themselves uncovered for the very conditions they are most likely to develop as they age. By maintaining India health insurance during their UK years, they ensure that by the time they move back permanently, their coverage is 'fully seasoned' and provides comprehensive protection from day one.

Tailored Features for the Global Indian

The insurance landscape in India has evolved to cater specifically to the needs of the global citizen. The integration of NRI health insurance into a broader wealth management portfolio allows for a more holistic approach to risk. Modern plans are not just about hospital beds; they include a range of value-added services that are particularly useful for those living abroad.

Telemedicine and Remote Monitoring

Many top-tier Indian insurers now provide 24/7 access to tele-consultations with leading Indian doctors. For an NRI in the UK, this can be an invaluable second opinion tool. If a parent is diagnosed with a condition in India, the child can facilitate a video call with a specialist via the insurer’s app to understand the treatment plan, bridging the geographical gap through technology.

Global Cover Add-ons

Some premium Indian health products now offer 'Global Cover' as an optional rider. This means that while the primary focus of the policy is coverage within India, the policyholder can be protected for emergency treatments in other countries as well. This is particularly beneficial for NRIs who travel frequently between the UK, India, and other international destinations for business or leisure.

OPD and Preventive Healthcare

In the past, Indian insurance was strictly focused on inpatient hospitalisation (treatments requiring more than 24 hours of stay). However, the shift towards preventive care has seen the introduction of Out-Patient Department (OPD) covers and annual health check-ups. For a visiting NRI, these benefits are highly practical. A trip home can be utilised to conduct comprehensive health screenings and dental or optical check-ups at a fraction of the cost of private UK clinics, all covered by their Indian policy.

The Importance of High Sum Insured

With the advancement of medical technology in India, procedures like robotic surgeries, organ transplants, and advanced oncology treatments are now standard in premium hospitals. However, these come with a premium price tag. For an NRI accustomed to the UK's standard of living, nothing less than a high sum insured policy would suffice.

Current trends suggest that for a family of four, or for elderly parents, a sum insured of at least ₹20 lakhs to ₹50 lakhs is necessary to combat medical inflation effectively. Many India health insurance now offer 'Restoration Benefits,' where the sum insured is automatically refilled if it is exhausted during a policy year. This is a vital feature for families with multiple members covered under a single floater policy.

Strategic Decision-making for the UK NRI

When choosing a policy from abroad, it is essential to look at the 'Claim Settlement Ratio' and the 'ICR' (Incurred Claim Ratio) of the provider. These metrics provide a glimpse into the reliability of the insurer when it comes to actually paying out. For the UK-based NRI, the ease of the digital interface is also a top priority. A provider that offers a robust mobile application for document uploads, policy renewals, and real-time claim tracking will significantly reduce the administrative burden of managing affairs from a distance.

In conclusion, the decision to invest in Indian health cover is an act of foresight. It protects the NRI’s Indian savings from being liquidated during a medical crisis, ensures that parents receive dignified and immediate care, and provides a seamless transition for those planning a future return to the subcontinent. By understanding the nuances of these policies, NRIs in the UK can effectively fortify their family’s health and financial future against the uncertainties of a globalised world.

Nach Verein filtern

Read More

The Asia Pacific High Intensity Focused Ultrasound (HIFU) market is growing rapidly, driven by increasing demand for non-invasive cancer treatments, rising prevalence of prostate and uterine tumors, growing medical tourism, and technological advancements in focused ultrasound systems. According to Business Market Insights, the market was valued at USD 290.2 million in...

Industrial projects often face major challenges when operating in remote or environmentally sensitive areas. In places like Fox Creek, where forestry, oil and gas, and construction industries play an important role in the local economy, reliable ground support systems are critical for maintaining safe and efficient operations. Access mats have become one of the most practical solutions for...

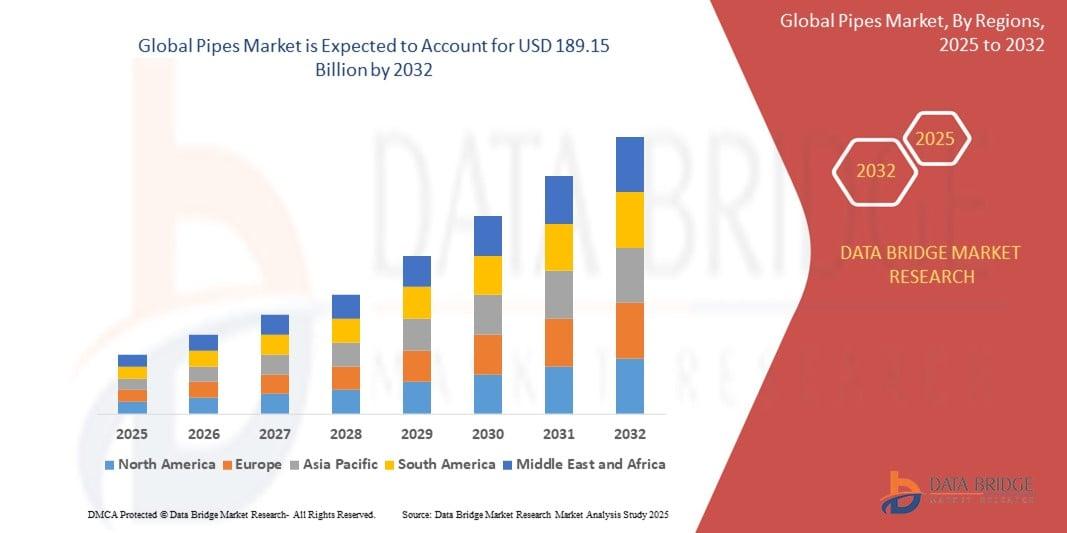

According to the latest report published by Data Bridge Market Research, the Pipes Market The global pipes market size was valued at USD 125.13 billion in 2024 and is expected to reach USD 189.15 billion by 2032, at a CAGR of 5.3% during the forecast period This growth is primarily driven by infrastructure modernization, urbanization, and the expansion...

Polaris Market Research has published a brand-new report titled Trail Mix Market Size, Share, Trends, & Industry Analysis Report By Product (Nuts & Seed, Dried Fruit, Granola & Cereal Bar, and Others), By Type, By Distribution Channel, and By Region – Market Forecast, 2025–2034 that includes extensive information and analysis of the industry dynamics. The...

According to the latest report published by Data Bridge Market Research, the Point-of-Care Molecular Imaging Devices Market CAGR Value The global point-of-care molecular imaging devices market size was valued at USD 1.04 billion in 2025 and is expected to reach USD 4.56 billion by 2033, at a CAGR of 20.30% during the forecast period...