Competitive Landscape: Sheet Metal Market Share, Leaders, and Strategic Positioning

In the commodity-like world of sheet metal, market share reflects economies of scale, raw material access, and product differentiation. The Sheet Metal Market Share is fragmented globally but concentrated regionally, with a handful of large steel and aluminum producers dominating. Based on available data and industry analysis, ArcelorMittal is the global leader in steel sheet, with an estimated 8-10% global share. POSCO, Nucor Corporation, Thyssenkrupp AG, and Tata Steel are significant players. In aluminum sheet, Hindalco Industries (through its subsidiary Novelis), Alcoa Corporation, and Norsk Hydro lead. Chinese producers (Baowu, HBIS, Shagang) collectively hold a large global share, primarily in domestic and emerging markets. Understanding market share dynamics is essential for sheet metal buyers, fabricators, and investors evaluating supply chain security.

Market Overview and Introduction

The sheet metal market share landscape is shaped by several factors: vertical integration (control over iron ore, coal, or aluminum refining), production cost (access to low-cost energy, labor, and raw materials), product mix (ability to produce advanced high-strength steel, coated, or specialty sheet metal), geographic presence (proximity to major consuming markets like automotive plants), and sustainability credentials (green steel, recycled content). The market is not winner-take-all; instead, different leaders dominate different regions and product segments. ArcelorMittal leads in Europe and the Americas for automotive sheet. POSCO leads in Korea and has a strong presence in automotive steel globally. Nucor is the leader in the US for sheet metal via electric arc furnace (EAF) production. Hindalco (Novelis) leads in aluminum sheet for beverage packaging and automotive body panels.

Key Growth Drivers Influencing Share

Several drivers influence shifts in sheet metal market share. First, cost leadership: Companies with access to low-cost iron ore, coal (or scrap for EAF), and energy can underprice competitors, gaining share. Nucor’s EAF-based model is highly cost-competitive in the US. Second, product differentiation: Producers of advanced high-strength steel (AHSS) and ultra-high-strength stainless steel (JFE Steel’s March 2026 launch) gain share in premium automotive applications. Third, geographic expansion: ArcelorMittal’s acquisition of a 60% stake in a German automotive sheet-metal forming specialist (creating access to European automakers) exemplifies this. Fourth, sustainability leadership: Producers offering green steel (using hydrogen or renewable energy) are gaining share with environmentally conscious buyers. Fifth, strategic partnerships: POSCO’s partnership with Ball Corporation (March 2026) for aluminum sheet supply secures long-term demand.

Consumer Behavior and E-commerce Influence on Share

Consumer behavior influences market share indirectly through demand for sustainable and high-performance materials. Automakers seeking to improve fuel efficiency and meet emissions targets will favor sheet metal suppliers that offer lightweight AHSS and aluminum. This shifts share toward producers with advanced product portfolios. Builders seeking LEED certification favor sheet metal with high recycled content, benefiting EAF producers like Nucor. E-commerce is affecting share in the distribution segment: online platforms that aggregate supply from multiple producers can capture share from traditional distributors. Smaller, nimble producers can use e-commerce to reach customers directly, bypassing distributors and potentially gaining share from larger producers that rely on traditional sales channels. Online customer reviews and ratings of sheet metal quality and service are beginning to influence purchasing decisions for smaller buyers.

Regional Insights and Preferences in Share Distribution

Market share varies significantly by region. In Asia-Pacific, Chinese producers Baowu, HBIS, and Shagang hold the largest shares domestically, but globally, POSCO and Tata Steel are significant. In Japan, JFE Steel and Nippon Steel lead. In North America, Nucor, ArcelorMittal, and United States Steel Corporation lead for steel sheet; Alcoa and Novelis lead for aluminum sheet. The US market has seen consolidation. In Europe, ArcelorMittal is the clear leader, followed by Thyssenkrupp and Tata Steel’s European operations. In India, Tata Steel and Hindalco lead. In South America, Gerdau and Ternium have strong positions. In MEA, Emirates Steel and Hadeed lead. Overall, market share is highly regional due to transportation costs; sheet metal is heavy and bulky, making long-distance trade less economical.

Technological Innovations and Emerging Trends Affecting Share

Technology is a significant lever for shifting market share. Advanced high-strength steel (AHSS) and ultra-high-strength stainless steel are product innovations that allow producers to differentiate and gain share in high-value segments. Digitalization of production (Industry 4.0) improves yield and reduces costs, helping producers compete on price. Artificial intelligence for defect detection reduces scrap and improves quality, enhancing brand reputation. Green steel production processes (hydrogen-based direct reduction) are a major potential share shifter; first movers like SSAB and ArcelorMittal could capture share from legacy producers as carbon regulations tighten. Coating technologies (Galvalume, Galvanized, Aluminized) add value and differentiate products. Perforated sheet metal producers with advanced tooling can capture share in architectural and industrial niches.

Sustainability and Eco-friendly Practices as a Share Driver

Sustainability is becoming a significant driver of market share, particularly in Europe and for automakers with aggressive ESG targets. Green steel (produced with low CO2 emissions) commands a premium and may be preferred by automakers like BMW, Mercedes-Benz, and Volvo. Producers that can certify their products with low carbon intensity are gaining share. Recycled content is another factor; EAF producers like Nucor already have high recycled content (over 90% for some products), giving them an advantage over blast furnace producers. Sustainable sourcing certifications (ResponsibleSteel, Aluminium Stewardship Initiative) are becoming procurement requirements. Circular economy partnerships (like POSCO-Ball) lock in demand. Producers that ignore sustainability risk losing share in premium segments, particularly in Europe.

Challenges, Competition, and Risks to Share

Maintaining or growing market share is increasingly difficult. Overcapacity, particularly in China, leads to low prices and trade disputes; Chinese producers could export surplus sheet metal, capturing share in other markets but triggering anti-dumping duties. Raw material price volatility affects cost competitiveness; a producer with long-term contracts at favorable prices can gain share. Trade policies (tariffs, quotas) artificially protect domestic producers, limiting share shifts. Competition from alternative materials (composites, plastics) could reduce the total sheet metal pie, intensifying share battles among producers. Energy costs are a major differentiator; producers with access to low-cost renewable energy (e.g., hydro power in Canada, Scandinavia) have a structural advantage. Labor costs are another factor; Chinese and Indian producers have lower labor costs than Western counterparts.

Future Outlook and Investment Opportunities in Share

The future distribution of sheet metal market share will likely see continued consolidation, with large players acquiring smaller ones to gain scale or technology. Investment opportunities related to market share include: investing in green steel producers poised to gain share from legacy producers. Electric arc furnace (EAF) mills (vs. blast furnaces) offer lower carbon footprint and operational flexibility. Advanced coating lines that add value to commodity sheet metal. Digital distribution platforms that aggregate supply from multiple producers. Scrap processing and recycling operations that feed EAF mills. Geographically, India offers the most compelling opportunity for market share growth, with rising domestic demand and policy support for local production. Chinese producers are likely to consolidate further, with larger players gaining share from smaller, less efficient mills. US producers are protected by tariffs but face long-term transition challenges.

Conclusion

Sheet metal market share is contested by a mix of global giants (ArcelorMittal, POSCO) and regional leaders (Nucor in US, Tata in India). No single player dominates globally, but regional concentration is high. Key insights include the growing importance of product differentiation (AHSS, green steel) and sustainability as share drivers, the impact of trade policies on regional share, and the role of technological innovation in cost leadership. For manufacturers, maintaining share requires investment in advanced products, green production, and digital efficiency. For investors, opportunities lie in green steel, EAF mills, and distribution platforms.

Uncover future growth patterns with expert-driven reports:

Kitchen Ventilation Hoods Market

Категории

Больше

Kitchen Remodeling in Whittier, CA is one of the most impactful home improvement projects homeowners can invest in, but it also comes with a lot of uncertainty. Between rising material costs, different contractor pricing structures, and unexpected issues in older homes, many homeowners struggle to understand what a fair and realistic remodeling project should look like. Whittier has a mix of...

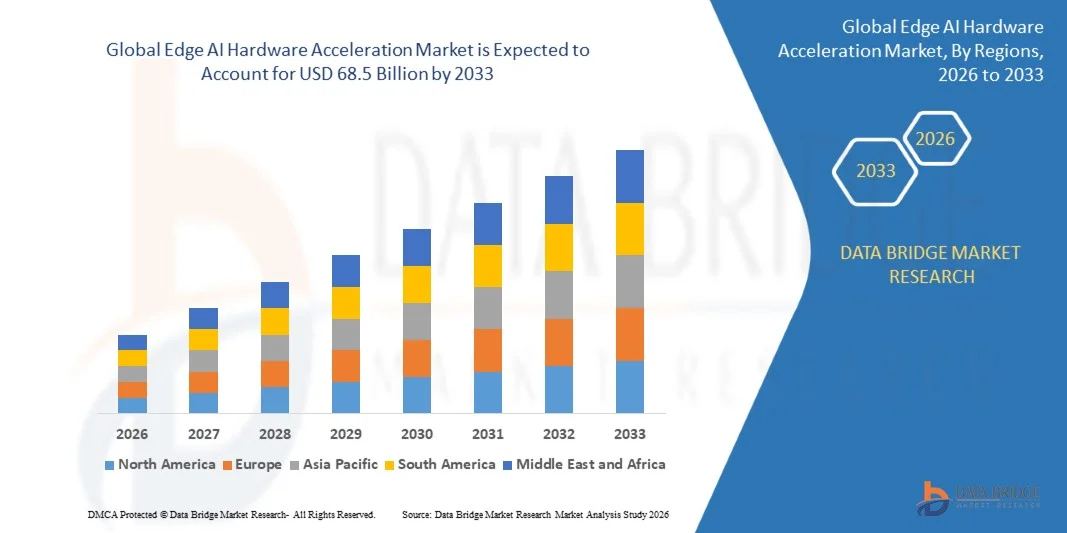

Edge AI Hardware Acceleration Market According to the latest report published by Data Bridge Market Research, the Edge AI Hardware Acceleration Market The Edge AI Hardware Acceleration Market was valued at USD 14.8 billion in 2025 and is projected to reach USD 68.5 billion by 2033, growing at a CAGR of 21.2% from 2026 to 2033. The persuasive Edge AI Hardware...

The MS Beam Price Trend remained positive during the first quarter of 2026, reflecting the strong momentum seen across India's construction, infrastructure, and industrial sectors. As one of the most widely used structural steel products, MS beams play an important role in building projects, bridges, warehouses, factories, and commercial developments. During Q1 2026, the market witnessed a...

The global Reusable Booth Systems Market is projected to grow from USD 515.0 million in 2026 to USD 875.0 million by 2036, expanding at a 5.4% CAGR over the 10-year forecast period. Growth is propelled by multi-show event strategies, rising demand for modular, cost-efficient exhibition infrastructure, and a shift toward asset reuse across recurring trade...

In today’s fast-paced digital world, the need for innovative online solutions has never been greater. Users across the globe are constantly seeking platforms that offer convenience, efficiency, and security. One such emerging platform making waves in the online ecosystem is https://zs999.io/. With its user-centric approach and advanced features, it promises to redefine the way people...