Polyimide for Flip Chip Packaging: The Quiet Insulation Layer Carrying AI Chips, HBM, Automotive Compute and the Next $133 Billion Fab Investment Cycle

A flip chip package looks like a tiny black square from the outside, but inside it is a dense traffic system of copper pillars, solder bumps, redistribution layers, passivation films, stress buffers and under-bump metallization. Polyimide for flip chip packaging sits in this traffic system like the roadbed beneath a high-speed rail corridor. It is not the most visible material, but without it, the package loses electrical insulation, thermal-cycle reliability and mechanical stress control.

The story begins with scale. A high-performance flip chip package can carry 10,000 to over 100,000 interconnect points, depending on die size, bump pitch and package class. Each interconnect must survive heat, current flow, board mounting pressure and repeated expansion mismatch between silicon, copper, solder and organic substrate. Polyimide for flip chip packaging earns its place because it can act as a 3–10 micron stress-buffer layer, a dielectric film, a passivation coating and, in photosensitive grades, a directly patternable layer for fine package routing.

The infrastructure behind this material is not one factory line; it is a chain of wafer coating tracks, lithography tools, curing ovens, plasma treatment, copper plating lines, inspection systems and assembly houses. One 300 mm wafer can hold several hundred to several thousand die, and every wafer-level packaging flow may require 1–3 polymer coating steps depending on RDL count and passivation design. That means Polyimide for flip chip packaging is consumed not by chip count alone, but by wafer starts, layer count, die area, bump density and yield rules.

The spending timeline explains why this material is now strategic. Global 300 mm fab equipment spending moved above the $100 billion annual zone in 2025, and SEMI projected a sharp rise for 2026 as AI chips, HBM memory and regional semiconductor localization accelerated. When front-end investment rises, advanced packaging pressure follows 12–24 months later because more high-performance wafers must be assembled into usable systems. Polyimide for flip chip packaging is therefore linked to a delayed but powerful back-end investment wave.

A simple infrastructure calculation shows the leverage. If one advanced packaging line processes 40,000 wafer starts per month, that equals 480,000 wafers per year. If 60% of those wafers use flip chip or flip-chip-derived flows, and each relevant wafer uses two polymer dielectric or passivation coats, the line generates roughly 576,000 polyimide coating events annually. At only a few milliliters of formulated material per wafer coating after dispense loss and edge-bead removal, the volume looks small; but the value is high because purity, defect control and process stability decide package yield.

Polyimide for flip chip packaging is also a geography story. Taiwan, South Korea, Japan, the United States, China and Singapore dominate the high-end assembly and packaging map. Taiwan leads in advanced logic and chiplet packaging. South Korea connects the material to HBM and memory-stack ecosystems. Japan anchors specialty polymer chemistry and photo-dielectric know-how. China is building local capacity across mature and advanced packaging. The United States is reshoring advanced packaging around AI, defense and high-performance computing. In each region, the same rule applies: a 1% yield improvement on a high-value AI package can be worth more than the annual polymer bill.

Technically, the material solves three quantified problems. First, coefficient-of-thermal-expansion mismatch: silicon sits near 2.6 ppm/°C, copper near 17 ppm/°C and organic substrates often above 15 ppm/°C. Second, cure and process survival: packaging films must withstand curing cycles commonly around 200–350°C depending on chemistry and device limit. Third, electrical isolation: dielectric layers must separate copper routing and under-bump features at micron-scale distances while preventing leakage, moisture-driven corrosion and cracking. Polyimide for flip chip packaging survives because it balances elongation, adhesion, insulation and thermal resistance better than many conventional organic coatings.

Application mapping makes the demand more visible. In smartphones, flip chip packaging is tied to application processors, RF modules, power management ICs and image processing devices. In servers, it connects CPUs, GPUs, AI accelerators and networking ASICs. In automotive electronics, it supports ADAS processors, radar chips, power control ICs and high-temperature reliability packages. In each case, Polyimide for flip chip packaging is used where the device needs dense interconnects, low defectivity and protection against package warpage.

DataVagyanik estimates the global Polyimide for flip chip packaging market at USD 487.6 million in 2026, with demand forecast to reach USD 742.8 million by 2031, representing a 2026–2031 CAGR of 8.8%. This sizing includes photosensitive and non-photosensitive polyimide materials used as stress-buffer, passivation, dielectric and RDL-support layers in flip chip, flip chip BGA, wafer-level and flip-chip-derived advanced packages. The 2026 value is anchored to advanced packaging wafer volumes, 300 mm capacity additions, AI/HBM package growth, and material intensity per package layer rather than broad semiconductor material assumptions.

The use-case story is easiest to see in an AI accelerator. A single high-end accelerator package may integrate a logic die, multiple HBM stacks, silicon interposer or organic substrate routing, copper pillars, micro-bumps and high-density redistribution. The package may sell for hundreds or thousands of dollars, but one failure at the polymer-metal interface can scrap the entire unit. Polyimide for flip chip packaging becomes a low-volume, high-consequence material: its cost share may sit below 1% of package value, but its failure impact can reach 100% of the package.

In manufacturing, the adoption decision is not emotional; it is statistical. A packaging house compares defect density, crack resistance, via opening accuracy, copper adhesion, cure temperature, film shrinkage and compatibility with developers or strippers. If a polyimide system reduces voiding, delamination or leakage by even 500 parts per million on a million-unit build, it protects 500 packages. In consumer ICs this may be a cost issue; in AI, automotive and aerospace-grade chips, it becomes a qualification and reliability issue. That is why Polyimide for flip chip packaging is qualified slowly but retained for long production cycles.

The material also sits at the center of the photosensitive-versus-non-photosensitive choice. Photosensitive polyimide reduces process steps because the film can be patterned directly through lithography, removing separate photoresist coating and stripping steps in some flows. Non-photosensitive polyimide remains relevant where stress-buffer performance, adhesion and film uniformity matter more than direct patterning. For high-volume packaging, removing even one process step across 500,000 wafers per year can save thousands of tool hours and reduce defect opportunities. Polyimide for flip chip packaging therefore competes not just on material price, but on total process economics.

The supplier ecosystem is concentrated but not static. HD MicroSystems, DuPont-linked material platforms, Qnity electronics materials, Toray, Asahi Kasei, Fujifilm, Sumitomo Chemical and other Japanese and global specialty chemical players form the core chemistry base around polyimide, PBO, dielectric coatings and package polymers. OSATs and foundry-owned packaging lines then convert those chemistries into qualified process recipes. Polyimide for flip chip packaging is rarely bought like a commodity resin; it is co-qualified with coating thickness, bake profile, lithography conditions, copper plating chemistry and reliability testing.

By infrastructure theme, one kilogram of advanced electronic-grade polyimide formulation is not comparable to one kilogram of industrial polymer. The semiconductor version requires ionic purity, filtration discipline, lot traceability, low-metal contamination and stable viscosity. A material batch may pass through particle filtration below sub-micron levels, metal ion checks, shelf-life control and cleanroom-compatible packaging. Polyimide for flip chip packaging therefore carries value from invisible controls: fewer particles, fewer mobile ions, better coating uniformity and tighter lot-to-lot behavior.

The next demand layer comes from bump pitch compression. Traditional flip chip bump pitches have moved from coarse ranges above 150 microns toward finer pitches in advanced packages, while chiplet and 2.5D architectures push interconnect density even further. As pitch shrinks, the polymer window narrows. Via openings must be cleaner, sidewalls must be stable, copper interfaces must hold, and stress must be distributed across thinner structures. Polyimide for flip chip packaging becomes more critical as the package shifts from “connection platform” to “system architecture.”

The theme is clear: the future of computing is not only about smaller transistors. It is about more chips talking to each other inside one package, across shorter distances, with less power loss and higher bandwidth. Every AI server rack, every HBM stack, every advanced GPU and every automotive compute module increases pressure on the packaging layer. Polyimide for flip chip packaging is one of the quiet materials absorbing that pressure, one micron-thick film at a time.

How Polyimide for Flip Chip Packaging Turns Wafer-Level Complexity Into Reliable Electronic Infrastructure

The investment map around advanced packaging is becoming as important as the fab map itself. A new front-end fab may cost USD 10–20 billion, but the chips produced inside it cannot enter AI servers, smartphones, vehicles or telecom equipment without back-end infrastructure. Substrate plants, bumping lines, RDL lines, molding lines, thermal cycling labs and reliability chambers are now part of the same semiconductor sovereignty equation. Polyimide for flip chip packaging benefits directly from this shift because it is consumed exactly where wafer output becomes a packaged system.

In a typical flip chip packaging flow, the polyimide layer appears after wafer passivation and before final bump or redistribution structures. The wafer is cleaned, coated, soft-baked, exposed or patterned depending on material type, cured and then integrated with metal routing or bumping. Each step carries a yield number. If coating uniformity is off by even 5–10%, via definition, bump coplanarity or adhesion may suffer. Polyimide for flip chip packaging is therefore part of the process-control stack, not just the material stack.

The economics are sharper in fan-out and wafer-level packaging. A wafer-level package can eliminate some substrate dependency, reduce package height and improve electrical performance, but it increases sensitivity to polymer behavior. Warpage during cure, reconstitution and redistribution can create alignment errors measured in microns. If a 300 mm reconstituted wafer carries 500 large packages and 2% are lost to polymer-linked defects, 10 packages are gone before final test. In high-value devices, that loss can exceed the material cost by 50–200 times.

This is why OSATs and foundries do not switch these materials casually. A new polyimide grade may require 6–18 months of qualification across adhesion, thermal cycling, humidity bias, dielectric breakdown, copper compatibility, solder reflow and board-level reliability. Automotive-grade devices can push qualification even harder because components may face 1,000–2,000 temperature cycles and long operating lives. Polyimide for flip chip packaging must prove that it can survive both the factory and the field.

The automotive use case is a useful stress test. A vehicle that once used 500–800 semiconductor devices can now use 1,500–3,000 devices in EV and ADAS-heavy platforms. Not all are flip chip, but the share of high-compute and power-management packages is rising. Radar processors, domain controllers, battery management ICs and infotainment SoCs need compact, reliable packaging. Polyimide for flip chip packaging supports this migration by enabling dense I/O, better stress relief and improved package durability under heat, vibration and humidity.

The AI server use case is even more material-intensive. A single AI server may host 4–8 accelerator modules, high-speed networking chips, CPUs, power controllers and memory interfaces. The most advanced accelerators rely on flip chip, 2.5D packaging, HBM integration and high-density substrates. Compared with a conventional server board from five years ago, the package-level interconnect burden is several times higher. Polyimide for flip chip packaging rides this rise because every advanced package needs more dielectric protection, redistribution support and interfacial reliability.

In smartphones, the story is about space. A premium smartphone board may contain more than 1,000 electronic components in a few tens of square centimeters. Application processors, RF front-end modules, power management chips, image processors and memory packages compete for area and thickness. Flip chip packaging helps reduce footprint and improve signal performance. Polyimide for flip chip packaging makes this miniaturization practical by protecting fine features while allowing thinner, denser package structures.

From a use-case mapping perspective, demand can be split into four high-growth lanes. First, AI and HPC packages account for the fastest value growth because die sizes are larger and package complexity is higher. Second, HBM and memory-interface packaging adds demand through fine interconnect and thermal-cycle reliability. Third, automotive compute creates long-life reliability demand. Fourth, mobile and consumer electronics create high-volume demand where yield economics dominate. Polyimide for flip chip packaging sits across all four lanes, but value per wafer is highest in AI, HPC and advanced memory.

Material intensity varies by package architecture. A simple flip chip BGA may require one main stress-buffer or passivation layer. A more advanced wafer-level or redistribution-heavy package can require two or more polymer dielectric layers. A chiplet-based package can multiply the polymer requirement because routing density and interface count rise. If the average number of polyimide-related coating layers rises from 1.2 to 1.6 across a qualified packaging portfolio, material demand increases by 33% even if wafer volume is unchanged.

That layer-count effect is one reason market growth can outpace semiconductor unit growth. The number of packaged chips may grow in single digits, but advanced package material intensity can grow faster because more devices move from wire bond to flip chip, from flip chip to fan-out, and from standard BGA to 2.5D or chiplet structures. Polyimide for flip chip packaging is exposed to this intensity curve rather than only to chip shipment volume.

The infrastructure spending behind the trend is measurable. Advanced packaging facilities require lithography steppers or aligners, spin coaters, spray coaters, curing ovens, plasma tools, electroplating equipment, metrology systems and reliability-test chambers. A single advanced packaging expansion can involve hundreds of tools and tens of thousands of square meters of cleanroom and controlled manufacturing space. Polyimide consumption begins only after this infrastructure is installed, qualified and loaded with wafers, which creates a lag between capital spending announcements and material revenue.

There is also a hidden logistics layer. Semiconductor polyimide formulations are shipped under controlled conditions, stored with shelf-life limits and handled through clean dispensing systems. Packaging houses track lot numbers because a deviation in one chemical batch can affect thousands of wafers. If one lot supports 5,000–10,000 wafers in a high-volume line, traceability must connect raw material certificate, coating result, wafer ID and reliability outcome. Polyimide for flip chip packaging is therefore tied to quality infrastructure as much as production infrastructure.

The technical selection criteria are also quantified. Low moisture uptake matters because absorbed moisture can expand during reflow and create delamination risk. High elongation helps absorb stress between rigid silicon and softer organic substrate. Dielectric strength protects against leakage between copper features. Thermal stability protects the film during curing, solder reflow and package operation. Adhesion to copper, silicon nitride, silicon oxide and redistribution metals determines whether the package survives cycling. Polyimide for flip chip packaging wins when these properties remain stable together, not separately.

The competitive alternatives are real. PBO, benzocyclobutene-based dielectrics, epoxy-based passivation materials and other photosensitive dielectric systems are used in parts of advanced packaging. However, polyimide remains deeply embedded because of its long reliability record, process familiarity and broad supplier base. In high-volume semiconductor manufacturing, the incumbent material has an advantage when it has already passed qualification across billions of shipped devices. Polyimide for flip chip packaging continues to hold share because process risk often matters more than headline material innovation.

The adoption curve is also linked to substrate constraints. During periods of ABF substrate shortage, packaging companies looked harder at wafer-level redistribution, fan-out and alternative package architectures. These approaches do not remove polymer demand; they often increase reliance on high-performance dielectric coatings. When routing shifts closer to the wafer or reconstituted panel, polymer films become part of the package’s electrical and mechanical architecture. Polyimide for flip chip packaging gains relevance when the industry tries to reduce bottlenecks in conventional substrate-heavy flows.

Panel-level packaging could create another step change. Moving from 300 mm wafers to larger rectangular panels can increase processed area per cycle, but it also magnifies coating uniformity, warpage and defect-control challenges. A 600 mm class panel can carry multiple times the usable area of a 300 mm wafer, but the polymer process window must remain consistent across the entire surface. If panel-level packaging scales, Polyimide for flip chip packaging will need stronger performance in planarization, coating control and cure-stress management.

Regional localization adds another theme. The United States, Europe, India, Japan, South Korea, Taiwan and China are all pushing semiconductor self-reliance, but advanced packaging localization is harder than announcing a fab. It needs material suppliers, trained process engineers, clean chemical logistics, equipment maintenance, reliability labs and customer qualification. A country can assemble simple packages relatively quickly, but high-density flip chip packaging needs years of ecosystem development. Polyimide for flip chip packaging becomes a marker of whether the local supply chain is moving from basic assembly to advanced semiconductor manufacturing.

India is a good example of future potential. The country already has electronics assembly demand, design talent and rising semiconductor policy support, but advanced packaging depth is still developing. As outsourced assembly, test and packaging investments enter the country, the first wave will likely focus on mature and mid-complexity packages. Over time, flip chip, wafer-level and advanced substrate-linked capabilities can expand. Polyimide for flip chip packaging will not be the first material localized at large scale, but it will become important once India targets higher-value package qualification.

The final commercial logic is simple: packaging is no longer the back office of semiconductors. It is now a performance engine. AI chips need bandwidth. Vehicles need reliability. Smartphones need miniaturization. Data centers need thermal and electrical efficiency. Every one of those needs pushes more value into the package. Polyimide for flip chip packaging is not a headline material like silicon or copper, but it is one of the enabling layers that lets modern chips survive dense interconnect, high heat, fine pitch and long operating life.

The next five years will not be defined by whether polyimide is known. It is already known. The real shift will be in how much more demanding the package becomes. Larger die, finer pitch, more redistribution, higher current density, chiplet architectures and regional advanced packaging investments will keep raising the performance floor. In that environment, Polyimide for flip chip packaging becomes less of a consumable and more of a qualified infrastructure material, quietly deciding whether the most expensive chips in the world can be manufactured at scale.

Κατηγορίες

Διαβάζω περισσότερα

Nearby Car Assistance Service: Reliable Help When Your Car Breaks Down Car trouble can strike without warning—during your commute, on a road trip, or while running errands. When that happens, finding a nearby car assistance service becomes your top priority. Quick access to professional help can keep you safe, reduce stress, and get you back on the road faster. This article explains what...

The creative team behind this project boasts an impressive roster of award-winning talent. George C. Wolfe, celebrated for his stage and screen direction, will helm the feature. Ruben Santiago-Hudson is tasked with adapting August Wilson’s powerful play for the screen. An exceptional cast has been assembled, led by Viola Davis as the formidable Ma Rainey. She is joined by Chadwick...

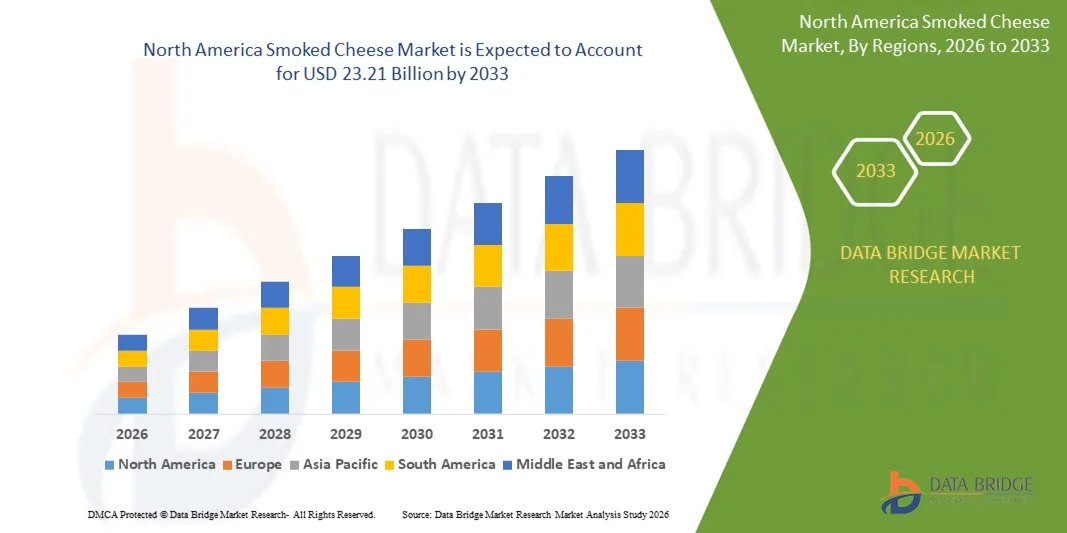

"Global Executive Summary North America Smoked Cheese Market: Size, Share, and Forecast The North America smoked cheese market size was valued at USD 15.00 billion in 2025 and is expected to reach USD 23.21 billion by 2033, at a CAGR of 5.00% during the forecast period The global North America Smoked Cheese Market analysis report gives a careful overview of...

China Voltage Control Relay plays an important role in industrial automation projects where stable electrical monitoring and coordinated control contribute to efficient equipment operation. Industrial users in manufacturing, infrastructure, renewable energy, machinery production, commercial buildings, and power distribution often evaluate product quality together with engineering support and...

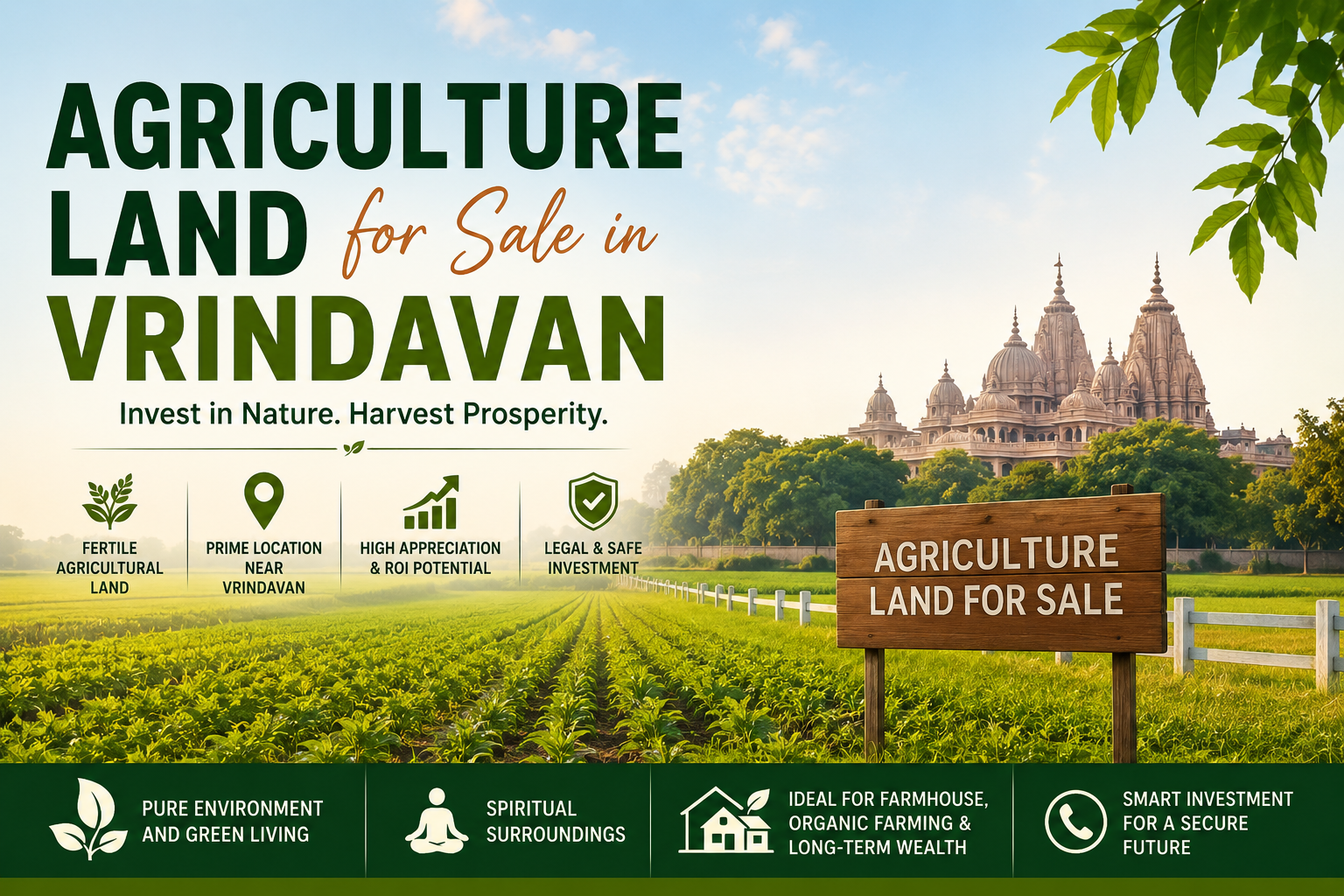

Vrindavan is one of those rare places in India where spirituality, heritage, and natural abundance converge. Situated along the sacred Yamuna River in the Mathura district of Uttar Pradesh, it has long been revered as a pilgrimage destination. But a quieter story is unfolding alongside its temples and ghats — one of rising land value, improving infrastructure, and growing investor...