LED Materials Market Growth Accelerates with Expanding General Lighting Applications

Market Overview

The LED materials market is expected to grow at an excellent CAGR of 10.5% in the long run to reach US$ 25.28 billion by 2028.

Industry stakeholders closely monitor LED materials market size analysis to evaluate investment priorities and expansion strategies. Rising demand for energy-saving lighting systems, coupled with increasing infrastructure development, is strengthening material consumption. Advancements in semiconductor manufacturing processes and cost-effective wafer production are helping companies improve operational efficiency while addressing evolving customer requirements across diverse applications.

The increasing adoption of energy-efficient lighting technologies and the growing replacement of conventional lighting systems are contributing to the expansion of the market. LED materials play a critical role in the production of advanced lighting and display solutions across multiple industries.

What is LED Materials?

LEDs (Light-Emitting Diodes) are semiconductor devices that emit light when an electric current passes through them. Unlike traditional bulbs, LEDs do not use filaments or gas-filled tubes. They are manufactured using semiconductor materials such as gallium arsenide, gallium nitride, and other compound semiconductors.

LED materials are primarily categorized into substrate, wafer, epitaxy, and phosphor materials. These materials are extensively used in applications such as general lighting, automotive lighting, and backlighting. LEDs offer several advantages including improved energy efficiency, longer lifespan, durability, and resistance to shock and vibration.

Market Growth Drivers

Several factors are driving the growth of the LED materials market:

- Bans on the usage of incandescent bulbs in multiple countries, accelerating the shift toward LED lighting.

- Increasing adoption of advanced technologies in cameras, high-definition televisions, camcorders, and related electronic devices.

- Rising utilization of LEDs in general lighting and automotive lighting applications.

- Growing demand for energy-efficient lighting solutions across residential and commercial sectors.

- Expansion of semiconductor-based technologies and infrastructure development.

The market is also benefiting from the ongoing transition toward modern lighting and display technologies.

Key Challenges

One of the primary challenges affecting the LED materials market is the lack of awareness among consumers regarding the advantages of LED technology.

Additionally, the market experienced disruptions during the COVID-19 pandemic due to supply chain interruptions and reduced demand from residential and commercial building sectors. However, the market recovered as manufacturing operations and supply chains resumed after the pandemic.

Get the free sample of the report:

https://www.stratviewresearch.com/Request-Sample/led-materials-market#form

Market Segmentation

By Material Type

The LED materials market is segmented into:

- Substrate

- Wafer

- Epitaxy

- Phosphor

- Others

Wafer is expected to remain the dominant material type during the forecast period due to its extensive use in microelectronic devices, cost-effectiveness of 6-inch and 8-inch wafer materials, and superior yield performance.

By Application Type

The market is segmented into:

- General Lighting

- Automotive Lighting

- Backlighting

- Others

General Lighting is projected to be the largest and fastest-growing application segment. Demand is driven by the widespread adoption of LEDs in streetlights, downlights, track lights, and other residential and commercial lighting applications.

Regional Analysis

The LED materials market is analyzed across:

- North America

- Europe

- Asia-Pacific

- The Rest of the World

Asia-Pacific is expected to remain both the dominant and fastest-growing regional market. The region accounts for more than 35% of the market share during the forecast period.

Growth is supported by:

- Increasing use of LEDs in general illumination.

- Rising demand for semiconductor devices.

- Expanding transportation sector.

- Rapid infrastructure development.

- Strong manufacturing base for LEDs and related applications.

Key Companies

The following companies are identified as key players in the LED materials market:

- Addison Engineering, Incorporated

- Akzo Nobel N.V.

- ams-OSRAM International GmbH

- Coherent Corporation

- Dowa Electronics Materials Co., Ltd.

- Epistar Corporation

- Intematix Corporation

- Macom

- MTI Corporation

- Nichia Corporation

- UBE Corporation

- Wolfspeed, Incorporated

FAQ

What is the projected growth rate of the LED materials market?

The LED materials market is expected to grow at a CAGR of 10.5% during the forecast period.

What will be the size of the LED materials market by 2028?

The market is expected to reach US$ 25.28 billion by 2028.

Which material type is expected to dominate the market?

The wafer segment is expected to remain the dominant material type during the forecast period.

Which region is expected to lead the LED materials market?

Asia-Pacific is expected to remain the largest and fastest-growing market, accounting for more than 35% of the market share.

Conclusion

The LED materials market is positioned for strong long-term expansion, supported by growing adoption of energy-efficient lighting technologies, increasing demand across electronics and automotive applications, and the global transition away from conventional lighting systems. With a projected market value of US$ 25.28 billion by 2028 and a CAGR of 10.5%, the industry offers substantial opportunities for manufacturers, suppliers, and investors. The dominance of wafer materials, the rapid growth of general lighting applications, and the leadership of the Asia-Pacific region will continue to shape the future of the market.

Categorieën

Read More

The Smart Manufacturing Market is rapidly transforming the global industrial landscape by integrating advanced digital technologies such as Artificial Intelligence (AI), Industrial Internet of Things (IIoT), robotics, cloud computing, and real-time analytics into manufacturing operations. As industries focus on improving efficiency, reducing operational costs, and enabling...

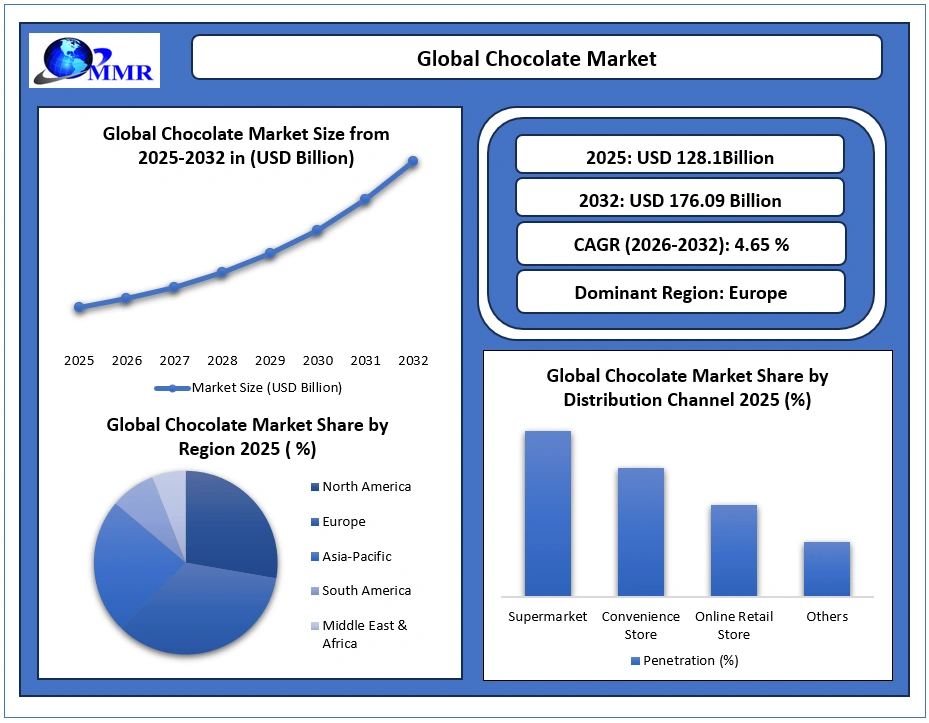

Global Chocolate Market Expands Rapidly with Premium Product Demand and Innovation in Sustainable Cocoa Sourcing The global chocolate market is witnessing substantial growth driven by increasing consumer demand for premium confectionery products, rising disposable incomes, and expanding product innovation across developed and emerging economies. Growing preference for dark chocolate,...

https://www.facebook.com/UsbestyPortableAC/ https://www.facebook.com/StopWattGermany/ https://www.facebook.com/StopWattGermany.Get/ https://www.facebook.com/BurnTide.Official/ https://www.facebook.com/BurnTide.Get/ https://www.facebook.com/groups/stopwattgermany/ https://www.facebook.com/groups/stopwattde/ https://www.facebook.com/CoreGLP.FR/ https://www.facebook.com/ErexivaGermany/...

"Executive Summary Apple Cider Vinegar Market Size and Share Forecast The global apple cider vinegar market was valued at USD 1.16 billion in 2024 and is expected to reach USD 2.24 billion by 2032. During the forecast period of 2025 to 2032 the market is likely to grow at a CAGR of 8.60%, primarily driven by the rising health consciousness amongst consumer This Apple Cider...

The 2025 BMW M4 Competition has made its way into GTA 5, and it's already turning heads across the modding community. It feels right at home in GTA 5's street racing chaos, whether you're pushing it hard through Vinewood Hills or blasting down the freeway with sirens in the distance. The fact that it's already pulled in thousands of downloads says a lot about how much players were waiting for a...