Deconstructing the Competitive Landscape and Virtual CPE Market Share

The Titans: Incumbent Network Equipment Providers

The battle for Virtual Cpe Market Share is fiercely contested, with traditional network equipment providers (NEPs) playing a dominant role. Giants like Cisco, Juniper Networks, Nokia, and Ericsson have leveraged their long-standing relationships with global communication service providers (CSPs) and large enterprises to establish a significant foothold in the vCPE space. These incumbents have adopted a hybrid strategy. On one hand, they have virtualized their own proven and trusted networking software (such as Cisco's IOS-XE or Juniper's Junos) to create a portfolio of Virtual Network Functions (VNFs). This allows their existing customer base to transition to a virtualized environment while retaining the familiarity and feature-richness of the operating systems they already know. On the other hand, they have invested heavily in developing or acquiring sophisticated orchestration platforms (like Cisco's NSO or Nokia's CloudBand) to provide end-to-end management of the NFV stack. Their market share is underpinned by their global sales channels, extensive support networks, and their ability to offer comprehensive, pre-integrated solutions that reduce the deployment risk for large, complex organizations. They offer a "one-stop-shop" approach that is highly appealing to customers seeking to minimize integration headaches.

The Challengers: Pure-Play Software and NFV Specialists

Challenging the dominance of the incumbents is a dynamic group of pure-play software vendors and NFV specialists who have built their businesses from the ground up on the principles of virtualization. Companies like Ciena (through its Blue Planet division), ADVA Optical Networking, and others have focused intensely on creating open, flexible, and highly automated vCPE solutions. Their key competitive differentiator is often their commitment to multi-vendor environments and open-source principles. Unlike some incumbents who may favor their own VNFs, these specialists build their orchestration platforms to be truly vendor-agnostic, allowing customers to mix and match the best-of-breed VNFs from any developer. This "disaggregated" model appeals to sophisticated buyers, particularly large service providers, who are keen to avoid a new form of software-based vendor lock-in. These companies often lead in areas like cloud-native architecture, utilizing containers and microservices to deliver more agile and efficient solutions. They capture market share by positioning themselves as more innovative, more flexible, and more aligned with the true spirit of NFV than the traditional hardware-centric giants. Their success has forced the entire industry to move towards more open and interoperable systems.

The Role of Open-Source and White Box Vendors

A crucial, disruptive force in the vCPE market share discussion is the growing influence of open-source projects and white box hardware vendors. Open-source platforms like ONAP (Open Network Automation Platform), OpenStack, and Kubernetes have become de facto standards in the NFV world, providing foundational components that many commercial vCPE solutions are built upon. The availability of this powerful, free-to-use software lowers the barrier to entry and enables a new ecosystem of innovation. Complementing this is the rise of white box vendors who manufacture generic, commercial off-the-shelf (COTS) servers and switches. This commoditizes the hardware layer, severing the link between network software and proprietary hardware. This trend allows service providers and even large enterprises to build their own vCPE solutions by integrating open-source software with low-cost white box hardware. While this "do-it-yourself" approach requires significant in-house expertise, it offers the ultimate level of control and cost savings. This disaggregated model puts immense pressure on the integrated solutions from traditional vendors and is a key factor in driving down prices and promoting openness across the entire market, even if it doesn't always show up directly in vendor market share reports.

Strategic Partnerships and Ecosystem Plays

In the complex vCPE landscape, no single company can do it all. As a result, strategic partnerships and ecosystem building have become critical strategies for gaining and maintaining market share. Leading vendors are building out vast ecosystems of certified partners. A vCPE platform vendor, for example, will create a marketplace of third-party VNFs that have been pre-tested and validated to run on their platform. This provides customers with choice and confidence, making the platform more attractive. We see deep collaborations between hardware manufacturers (like Dell and HP Enterprise), VNF developers, orchestration specialists, and public cloud providers (like AWS, Azure, and Google Cloud). For example, a service provider might offer a managed SD-WAN service based on a VNF from one vendor, running on an orchestration platform from another, deployed on a white box server from a third, with connectivity to workloads hosted in a public cloud. The vendors who are most successful at building and nurturing these rich, multi-vendor ecosystems are the ones best positioned to capture a larger slice of the market. The competitive battle is increasingly not just about product features, but about the strength and breadth of a vendor's partner ecosystem.

Explore More Like This in Our Reports:

Categorias

Leia Mais

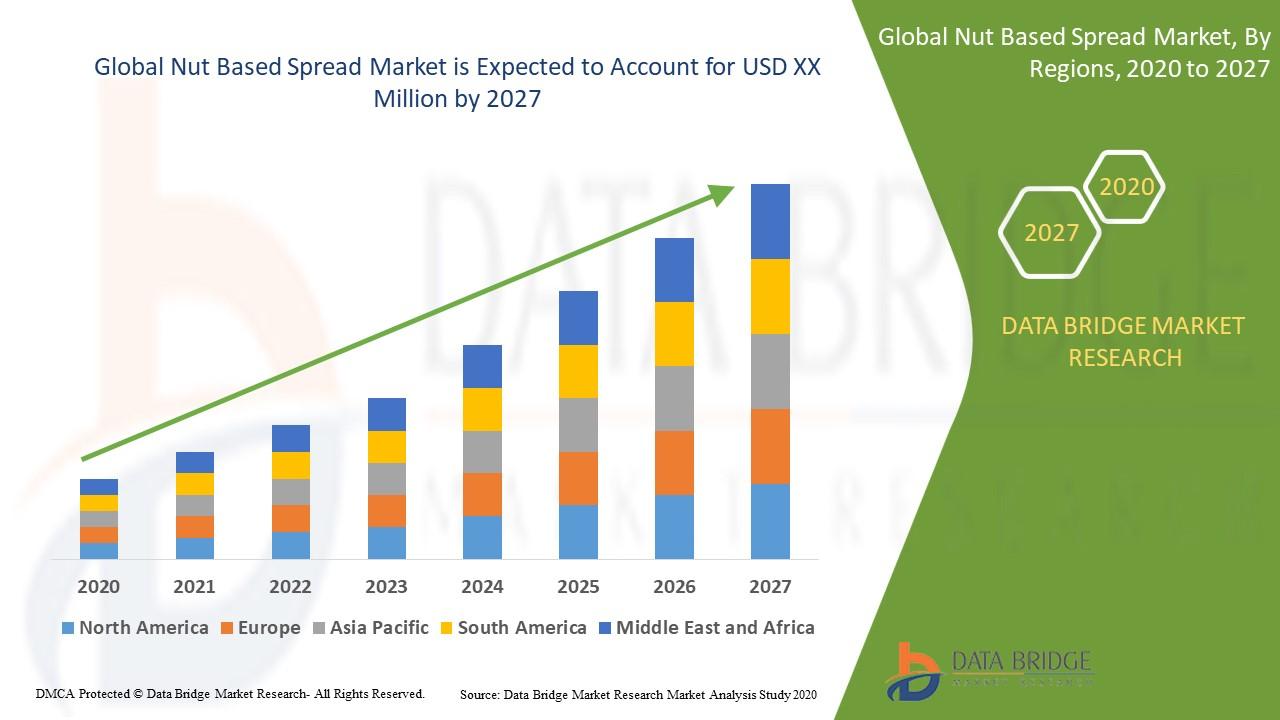

"Executive Summary Nut Based Spread Market Market Size and Share Analysis Report The global nut based spread market size was valued at USD 3.50 billion in 2024 and is projected to reach USD 5.17 billion by 2032, with a CAGR of 5.00 % during the forecast period of 2025 to 2032. This Nut Based Spread Market Market research report guides the management of a firm in planning. For...

In today’s competitive digital market, having a strong online presence is no longer optional. Customers search online before making purchasing decisions, and businesses that appear on the first page of Google gain the most attention. This is why hiring a professional SEO company in Pune has become essential for businesses looking to grow online. A trusted SEO company in...

Get updated and reliable N16302GC10 Dumps from HelloDumps. Prepare effectively with expert-verified study materials designed to help you pass your Oracle N16302GC10 certification exam on the first attempt. N16302GC10 Exam Dumps to Achieve Outstanding Results on Your First Attempt HelloDumps offers highly effective Oracle N16302GC10 exam dumps that perfectly support your preparation...

Looking for a watch that perfectly blends style, functionality, and affordability? Joeme Online Watches Store is your go-to destination for the latest trends in timepieces, and their collection featuring Knax watches is redefining what it means to wear a statement accessory. Whether you are dressing up for a formal occasion or adding a stylish touch to your casual look, Knax watches at Joeme...

Streetwear culture has seen explosive growth over the past decade, becoming a dominant force in fashion worldwide. Among the myriad brands that have risen to prominence, the Essentials Hoodie stands out as a flagship product for one of the most beloved streetwear brands in the market today. Known for its minimalist design, exceptional comfort, and broad appeal, Essentials...