Vision Care and Eyewear Coverage: What Health Insurance Includes for UK NRIs

Strategic cross-border financial planning requires Non-Resident Indians (NRIs) residing in the United Kingdom to closely evaluate the operational boundary lines of their domestic policies. While a significant portion of expatriate wealth management focuses on protecting against catastrophic medical events, managing high-frequency, outpatient clinical needs is equally critical to preventing minor financial leaks. Among these routine medical requirements, ophthalmology and corrective optics represent a specialized sector where coverage rules differ widely between the UK and India. For an expat balancing the state-funded provisions of the National Health Service (NHS) with private options back home, understanding the specific scope of vision care eyewear insurance coverage parameters is essential to establishing a seamless, dual-geographic health shield.

Many global professionals mistakenly assume that standard comprehensive plans automatically absorb all routine optical expenses. In reality, ophthalmic risk management follows strict underwriting definitions that dictate when a claim is covered and when it is excluded.

The Core Bifurcation: Therapeutic vs Cosmetic Ophthalmology

The fundamental principle governing optical claims in the Indian domestic market is the distinction between therapeutic medical interventions and cosmetic or preventative correction. Understanding this distinction allows policyholders to predict their out-of-pocket expenses accurately.

Covered Therapeutic Interventions

Indian health policies prioritize conditions that are classified as medically necessary to preserve basic vision or reverse progressive ocular disease. Advanced surgical procedures are fully covered under standard inpatient or daycare definitions, subject to localized sub-limits. These covered interventions include:

-

Cataract Extractions: The surgical removal and replacement of a clouded lens, which is routinely managed under a fixed monetary sub-limit per eye.

-

Glaucoma Managements: Surgical or advanced laser interventions designed to lower intraocular pressure and protect the optic nerve.

-

Retinal Detachment Repairs: Emergency cryopexy or vitrectomy procedures required to treat structural trauma to the retina.

-

Ocular Trauma Treatments: Immediate clinical interventions resulting from sudden external injuries or accidents.

Excluded Refractive Treatments

Conversely, procedures or items used purely to correct refractive errors, such as myopia, hyperopia, or astigmatism, are traditionally excluded from baseline hospitalisation contracts. Unless explicitly stated in a premium global rider, insurance plans do not cover routine eye examinations, contact lens prescriptions, or standard spectacle frames. This separation highlights why checking your specific vision care eyewear insurance coverage parameters before scheduling routine clinical visits is so important.

The Evolution of Refractive Error Coverage and LASIK Guidelines

As advanced laser technology has transformed ophthalmic care, the strict exclusion of refractive error treatments has evolved. The Insurance Regulatory and Development Authority of India (IRDAI) modernised claims guidelines by establishing clear, objective clinical thresholds for laser corrective surgeries.

Under current regulatory definitions, advanced refractive treatments like LASIK, PRK, or SMILE are no longer dismissed as purely cosmetic, provided the patient’s refractive error meets specific severity metrics. Most modern policies will consider a laser correction claim valid if the refractive error is documented at 7.5 dioptres or higher.

When a policyholder meets this clinical threshold, the procedure is recognized as a corrective treatment for a severe functional disability rather than an aesthetic enhancement. For a UK NRI utilizing an integrated nri health insurance contract, meeting this metric allows them to access premier corporate eye care chains across India, where advanced laser procedures are performed at a fraction of the cost of private treatment in London or Manchester.

Outpatient Department (OPD) Riders and Eyewear Allowances

For expatriates who want complete coverage for everyday eye care, including routine check-ups and prescription glasses, relying solely on standard hospitalisation terms is insufficient. Securing this level of protection requires adding a dedicated Outpatient Department (OPD) or wellness rider to the core policy framework.

Ophthalmic Policy Architecture

-

Core Inpatient Coverage (Standard)

-

Cataract Daycare Surgeries

-

Emergency Retinal Repairs

-

High-Dioptre LASIK (Refractive Error > 7.5)

Optional OPD & Wellness Riders (Premium Add-ons)

-

Annual Ophthalmologist Consultations

-

Prescription Eyewear & Corrective Lenses

-

Diagnostic Glaucoma Screenings

These optional riders expand the policy's utility by providing a specific annual allowance for everyday eye care. This allowance can be used to offset the cost of comprehensive eye examinations, diagnostic screenings, and prescription lenses or frames at empanelled optical networks. For families who wear prescription glasses, adding an OPD rider ensures that their routine optical care is covered, providing consistent financial support throughout the policy year.

Key Considerations for United Kingdom NRIs

Expatriates living in the United Kingdom navigate a unique healthcare system that directly influences how they design and use their health portfolios back home.

|

Expat Operational Reality |

Impact on Optical Planning |

Strategic Recommendation |

|

Long NHS Waiting Lists |

Non-emergency ophthalmic consultations or elective cataract procedures under the NHS can face extended administrative delays. |

Maintain a robust domestic policy in India to access immediate, high-quality private surgical care during personal visits. |

|

High Private UK Optical Costs |

Private ophthalmology visits and high-end prescription eyewear in the UK are expensive out-of-pocket costs. |

Schedule routine advanced eye screenings and diagnostic evaluations in India to leverage cost-effective private care. |

|

Cross-Border Exchange Rates |

Paying for a premium policy tier in Indian Rupees offers a distinct financial advantage when funded from a Pound Sterling source. |

Invest early in an advanced portfolio that waives sub-limits on daycare surgeries to maximize long-term protection. |

For an expat managing family health from abroad, choosing a tailored nri health insurance policy that offers clear terms on optical care is essential. It ensures that if a senior dependent parent in India requires immediate cataract surgery, or if you choose to undergo advanced laser correction during a visit, the financial process remains transparent, predictable, and fully supported by the insurer.

Selecting an Institutionally Aligned Portfolio

When evaluating different options in the domestic Indian market, look closely at the underlying policy wordings to confirm how they treat daycare ophthalmic procedures. Premium plans designed for global clients often feature shorter waiting periods for cataract surgeries and offer higher sub-limits on advanced intraocular lens implants.

Leading providers have adapted their product lines to meet the expectations of international clients by introducing comprehensive wellness benefits. For example, premium health portfolios like those structured by Niva Bupa offer elite variants that combine high-value inpatient limits with optimized outpatient benefits, allowing policyholders to manage both emergency eye surgeries and routine diagnostic consultations with ease.

Before finalizing any corporate [Health Insurance] program, verify that the contract explicitly details the waiting periods for optical ailments and outlines the pre-authorization path for daycare procedures. Managing these vision care eyewear insurance coverage details proactively protects your family's financial interests, ensuring complete peace of mind and access to world-class clinical eye care whenever you return home.

Categorías

Read More

"Antivertigo Agents Market Summary: According to the latest report published by Data Bridge Market Research, the Antivertigo Agents Market The global antivertigo agents market size was valued at USD 3.00 billion in 2025 and is expected to reach USD 4.10 billion by 2033, at a CAGR of 4.01% during the forecast period DBMR team uses simple language and easy...

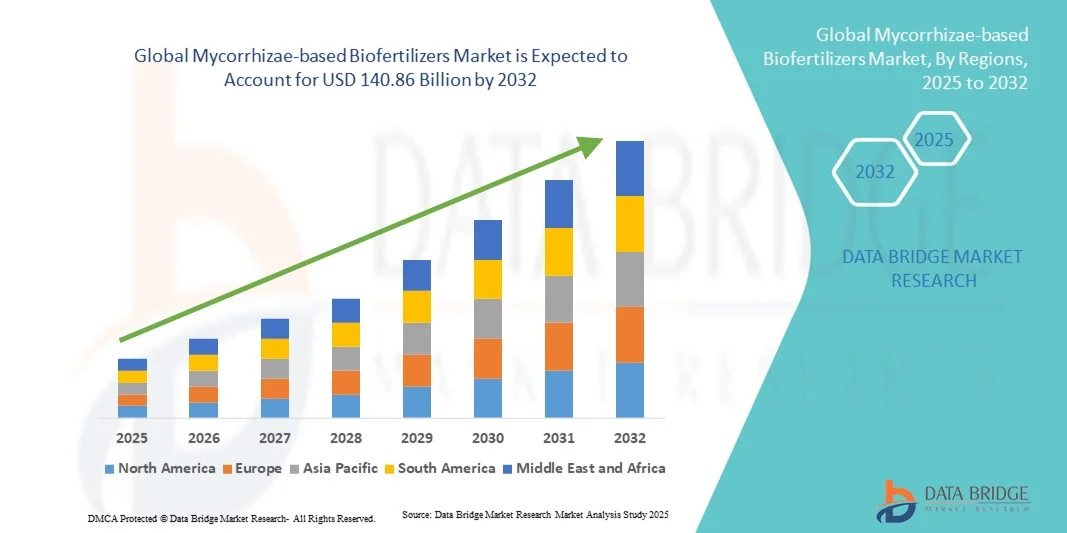

Mycorrhizae Based Biofertilizers According to the latest report published by Data Bridge Market Research, the Mycorrhizae-based Biofertilizers Market The global mycorrhizae-based biofertilizers market size was valued at USD 871.09 million in 2024 and is expected to reach USD 140.86 billion by 2032, at a CAGR of 6.40% during the forecast period The...

Sky Exchange 247: Everything You Need to Know Before Creating an Account The online betting and gaming industry has grown rapidly over the past few years, giving users access to a wide variety of sports betting, live casino games, and interactive gaming experiences from the comfort of their homes. Among the platforms gaining attention in this space is Sky Exchange 247, a platform known for...

Hard water is one of the most common household cleaning challenges in the United States. Millions of homes experience mineral buildup caused by calcium and lime deposits found in water supplies. Over time, these minerals accumulate inside appliances, pipes, faucets, showerheads, and other household surfaces, making cleaning more difficult and reducing appliance performance. As homeowners search...

In today’s fast-moving property market, making the right real estate decision is not always straightforward. Prices fluctuate, demand shifts quickly, and off-market opportunities are often hidden from public listings. This is where real estate consultants play a crucial role. Whether you are buying your first home, investing in rental property, or expanding your portfolio, a...