Tertiary Fatty Amides: The Quiet Infrastructure Chemical Turning Films, Fluids, Foams and Factories into Lower-Friction Systems

A packaging film line running at 450 meters per minute does not stop because the polymer is weak. It stops because surfaces fight each other. A polyethylene film with coefficient of friction above 0.45 can drag, wrinkle, block and jam. Bring that friction down toward 0.20–0.25 and the same line can gain 3–7% throughput without buying a new extruder. This is where Tertiary Fatty Amides enter the story: not as headline chemicals, but as gram-level infrastructure additives that decide whether a billion pouches, tubes, labels, sheets and molded parts move smoothly through machines.

The infrastructure behind Tertiary Fatty Amides starts upstream in the oleochemical chain. A typical production route pulls C12–C22 fatty acid streams from palm, coconut, rapeseed, soybean, tall oil or tallow-based fractions. One 50,000-tonne-per-year fatty acid fractionation asset can feed 8–12 downstream derivative families, but only a narrow 2–6% value slice is usually routed into amide chemistry. In tertiary chemistry, the fatty acid is converted with amines such as dimethylamine, diethanolamine or other substituted amines under controlled dehydration, forming molecules that carry both a long hydrophobic tail and a polar amide head. That dual architecture explains 70% of the commercial value: surface migration, lubrication, compatibility control and wetting behavior in one molecule.

Tertiary Fatty Amides are useful because they operate at extremely low use rates. In polyolefin films, many fatty amide systems are dosed between 500 ppm and 3,000 ppm. At 1,500 ppm, one tonne of additive supports roughly 667 tonnes of finished film. At a converter producing 60,000 tonnes of film per year, even a 0.15% dosage translates into only 90 tonnes of additive demand, yet that small volume can influence sealing speed, reel unwinding, bag opening force and packing-line rejects. This asymmetric economics makes Tertiary Fatty Amides attractive: the additive cost may represent less than 0.4% of film cost, but the operational impact can touch 5–10% of downtime-linked value.

The use-case map is wider than packaging. In plastics, Tertiary Fatty Amides support slip, anti-block, mold release and flow modification. In rubber and elastomers, they reduce compound sticking and improve processing torque by 4–12% in selected systems. In coatings and inks, they can support surface feel, abrasion response and dispersion stability at 0.2–1.0% dosage. In metalworking fluids and industrial lubricants, the same polar amide functionality helps boundary lubrication where metal surfaces need a thin organic film. In agrochemical formulations, tertiary fatty amide-type solvents and co-formulants help dissolve hydrophobic actives, stabilize emulsions and reduce crystallization risk during storage cycles from 5°C to 45°C.

According to DataVagyanik, the global Tertiary Fatty Amides market is valued at USD 384.7 million in 2026 and is forecast to reach USD 571.9 million by 2032, reflecting a 6.83% CAGR over the period. The 2026 demand base is estimated at 118.4 kilotons, implying an average realized value of nearly USD 3,249 per ton across industrial, plastics, textile, agrochemical, metalworking and specialty formulation grades. By 2032, volume demand is projected to reach 166.8 kilotons, with value growth outpacing volume because higher-purity, low-odor, bio-based and application-specific grades are expected to gain a larger share of purchases.

The strongest infrastructure pull comes from flexible packaging. Global plastic material production is above 400 million tonnes annually, and packaging continues to absorb roughly two-fifths of polymer demand. Even if only 18–22% of packaging resin goes into films where slip, anti-block or processing aids are relevant, the addressable film pool exceeds 30 million tonnes per year. At a conservative 0.10–0.20% additive intensity, that pool alone can create 30,000–60,000 tonnes of annual demand for fatty amide and related slip chemistries. Tertiary Fatty Amides capture only a fraction of this pool, but their role rises where converters need lower volatility, controlled migration, better formulation compatibility or liquid handling advantages.

There is also a timeline story. From 2021 to 2022, packaging converters faced resin volatility, freight spikes and higher energy costs, so additive buyers focused on yield protection rather than innovation. In 2023, destocking reduced chemical order visibility, but film producers kept spending on line efficiency because every 1% scrap reduction in a 40,000-tonne plant saves 400 tonnes of resin. In 2024 and 2025, the spending theme shifted toward mono-material packaging, recyclable films and lower-migration additives. By 2026, the investment logic becomes sharper: a USD 15–25 million blown-film or cast-film line needs additives that protect machine speed, seal integrity and regulatory compliance across 7–10 years of asset life.

The manufacturing network for Tertiary Fatty Amides is concentrated around three assets: fatty acid splitting and distillation, amine handling, and specialty batch or semi-continuous amidation. A mid-sized plant with 5,000–10,000 tonnes per year of amide capacity may require reactors, vacuum systems, condensers, nitrogen blanketing, filtration, flaking or liquid-packaging lines, storage tanks and quality-control labs. Capital intensity is usually lower than petrochemical monomer production but higher than simple blending. A practical greenfield specialty amide unit can require USD 8–18 million depending on automation, emission control, purity range and whether the producer already owns feedstock integration.

Tertiary Fatty Amides also sit inside a regional supply equation. Asia accounts for the largest demand because China, India, Southeast Asia, Japan and South Korea combine resin conversion, oleochemical feedstocks, agrochemical formulation and textile finishing. Europe buys higher-specification grades tied to regulatory, personal care, coatings and industrial fluid requirements. North America has a more consolidated specialty additives base, with demand linked to food packaging, wire and cable, engineering plastics, adhesives, lubricants and oilfield-adjacent chemistries. In a normal landed-cost structure, feedstock contributes 45–60% of manufacturing cost, energy and utilities 8–14%, amines 12–20%, and packaging, logistics and compliance another 10–16%.

The reason Tertiary Fatty Amides matter is that they monetize friction. Every industrial surface has a hidden tax: blocked film rolls, high screw torque, poor dispersion, unstable emulsions, sticky rubber sheets, rough coating feel or metal contact wear. A chemical used at one kilogram per tonne can decide whether a converter ships on time, whether a coating passes touch quality, or whether a formulation survives a hot warehouse. That is why this market is not built by loud demand. It is built by repeated technical approvals, plant trials, dosage curves and quiet procurement renewals.

Application Mapping: Where One Kilogram Changes a Production Line

The first adoption cluster for Tertiary Fatty Amides is packaging film, but the buying decision is rarely made by the procurement team alone. A technical manager usually tests three numbers before approval: coefficient of friction, blocking force and seal-window stability. If untreated film shows 0.42–0.55 dynamic friction and a treated grade brings it below 0.30 within 24–72 hours, the additive becomes a productivity lever. On a 25,000-tonne-per-year film line, a 2% speed improvement equals 500 tonnes of additional annual output. At a film conversion value of USD 1,500–2,200 per tonne, that improvement can represent USD 0.75–1.10 million of unlocked production value.

The second use case is polymer compounding. In masterbatch and engineering polymer systems, Tertiary Fatty Amides can reduce internal friction during extrusion, lower melt-processing stress and improve pellet handling. A compounding line operating at 1,000 kg per hour for 6,000 hours per year produces 6,000 tonnes annually. If additive optimization reduces torque by even 5%, the plant can cut energy intensity by 8–15 kWh per tonne in selected resin systems. At industrial electricity prices of USD 0.09–0.14 per kWh, that translates into USD 4,000–12,600 annual energy saving per line, before counting lower die build-up, smoother pellet flow and fewer operator interventions.

The third use case is industrial fluids. Tertiary Fatty Amides work because the amide group can interact with metal surfaces while the fatty chain provides lubricity. In metalworking fluids, even a 0.5–2.0% inclusion rate can change tool-life economics. If a machining shop spends USD 400,000 per year on cutting tools, a 3% extension in tool life saves USD 12,000 annually. For a lubricant blender, this is enough to justify a specialty additive that costs several dollars per kilogram, because the customer is not buying chemical mass; the customer is buying reduced wear, better surface finish and fewer stoppages.

In coatings, inks and adhesives, the story is tactile and measurable. Surface slip, rub resistance and dispersion quality influence defect rates. A wood coating, flexible ink or industrial topcoat that fails a rub test by 5–10 cycles can require reformulation. A small dose of amide chemistry can improve surface response without redesigning the entire resin system. For a coating plant producing 20,000 tonnes annually, a 0.3% dosage equals 60 tonnes of additive. If the formulation reduces rework by 1%, and rework costs USD 200–500 per tonne, the plant saves USD 40,000–100,000 annually. That is why specialty additives survive procurement pressure even when commodity solvents are cut aggressively.

The agrochemical formulation channel is smaller but more strategic. Many crop-protection actives are hydrophobic, crystalline and sensitive to storage conditions. Formulators need co-solvents, emulsifiers, dispersants and stabilizers that can keep active ingredients usable across transport, dilution and field application. Tertiary Fatty Amides can support this infrastructure where compatibility and solvency matter. A 10,000-tonne agrochemical formulation unit using 1–3% specialty co-formulants represents 100–300 tonnes of annual additive demand. The value is not in volume alone; it is in reducing phase separation, crystallization, nozzle blockage and failed field performance.

The Infrastructure Stack Behind the Molecule

The production infrastructure for Tertiary Fatty Amides is not a single reactor story. It is a chain of disciplined assets. First comes feedstock purification. Fatty acid fractions must be controlled by carbon chain distribution, acid value, iodine value, moisture and color. A 1% impurity swing can change odor, color stability or downstream reactivity. Second comes amine charging and reaction control. Tertiary amide production requires temperature discipline because excess heat can darken product, increase by-products and reduce batch acceptance. Third comes finishing: filtration, deodorization, flaking, pastillation, drumming or liquid bulk packing.

Quality control is where the market separates commodity suppliers from technical suppliers. Buyers typically track acid value, amine value, moisture, melting point or pour point, color, odor, viscosity and active content. In high-specification applications, batch rejection can occur for deviations that appear small on paper: 0.1–0.3% excess moisture, unacceptable odor notes, unstable color or poor low-temperature handling. A supplier selling into packaging, lubricants and coatings may need 15–25 product codes from the same chemistry platform. This explains why a 5,000-tonne specialty amide plant can sometimes create more customer value than a 50,000-tonne commodity fatty acid plant.

The logistics model is equally important. Solid grades need controlled flaking, bagging and anti-caking performance. Liquid grades need tank storage, heating coils, stainless-steel handling and clean transfer systems. Export shipments can spend 20–45 days in containers, so thermal stability matters. A product that performs well at plant exit but separates after a 40°C transit cycle becomes commercially weak. For Asian exporters, shipping to Europe or North America can add USD 150–350 per tonne in freight, documentation, warehousing and distributor margins. Therefore, local stocking hubs become part of the adoption infrastructure.

Player Behavior: Why This Market Grows by Trials, Not Advertising

The commercial behavior of Tertiary Fatty Amides is technical and relationship-driven. Large oleochemical companies bring feedstock security. Specialty additive companies bring formulation know-how. Regional manufacturers compete through cost, flexibility and fast customization. The strongest suppliers do not sell one molecule; they sell a 3-part service package: grade selection, dosage optimization and plant-trial troubleshooting. A converter rarely shifts suppliers for a 2–3% price discount if the existing additive protects line speed and customer approvals. This creates sticky demand once the material is qualified.

In actual buyer behavior, approval cycles can run from 3 months to 18 months. Packaging customers test migration, friction development over time, sealability and food-contact suitability. Lubricant customers evaluate wear scars, corrosion, emulsion stability and foam. Agrochemical customers test cold storage, hot storage, dilution stability and active compatibility. Coatings customers check rub, gloss, blocking and surface defects. One failed parameter can delay a supplier by an entire buying season. This is why market share shifts gradually rather than suddenly.

Investment is following application specificity. A producer does not need to build only more tonnes; it needs to build more qualified tonnes. Between 2026 and 2030, spending is likely to move toward three areas: low-odor grades for sensitive packaging and coatings, bio-based feedstock traceability for European and personal-care-adjacent buyers, and liquid grades that simplify handling for formulators. A plant that can make five standard grades may remain price-exposed. A plant that can make twenty application-tuned grades can protect margins of 18–28% even when fatty acid costs fluctuate.

The Technical Reason Demand Keeps Expanding

The technical reason Tertiary Fatty Amides keep expanding is simple: modern materials are asked to do contradictory things. Packaging films must be thinner but stronger. Lubricants must perform with lower environmental burden. Coatings must feel smoother while using more compliant formulations. Agrochemical products must carry difficult actives in stable liquid systems. Plastics processors must run faster while reducing scrap. In each case, surface behavior becomes a bottleneck.

A 10-micron reduction in film thickness can save 10–15% resin per pack, but thinner film is less forgiving during winding, sealing and transport. A recyclable mono-material pouch may simplify end-of-life design, but it increases the need for fine-tuned additives because the structure cannot depend on multiple layers doing separate jobs. A water-reduced industrial fluid may look environmentally superior, but it needs stronger boundary-lubrication chemistry. These transitions push demand toward additives that work at low dosage and solve multiple performance variables.

By 2030, the most attractive growth pockets for Tertiary Fatty Amides will not be the largest-volume applications alone. They will be applications where performance failure is expensive. High-speed packaging, food-contact films, specialty masterbatches, metalworking fluids, industrial coatings, agrochemical concentrates and engineered release systems all fit this logic. A supplier serving these niches can grow faster than the base market because each customer approval creates recurring demand for 3–7 years.

The economics close with one practical point: infrastructure chemicals win when they disappear into productivity. Tertiary Fatty Amides are not visible in a pouch, a lubricant, a coating, a pesticide bottle or a molded plastic part. Yet they shape how those products are produced, packed, shipped and used. A few hundred parts per million can change friction. A few kilograms per batch can stabilize a formulation. A few tonnes per year can protect an entire production line. That is the quiet but measurable value story of Tertiary Fatty Amides.

Categorii

Citeste mai mult

" According to the latest report published by Data Bridge Market Research, the HER2 Positive Breast Cancer Treatment Market The global HER2 Positive Breast Cancer Treatment market size was valued at USD 11.14 billion in 2025 and is expected to reach USD 12.54 billion by 2033, at a CAGR of 1.50% during the forecast period Getting thoughtful about competitive...

Best Fabrics for Korean Co Ord Sets | Comfort & Style Guide When it comes to effortless fashion, fabric plays a bigger role than most people realize. The right material can completely change how an outfit looks, feels, and performs throughout the day. This is especially true for korean co ord sets, which are loved for their minimal design, clean structure, and everyday...

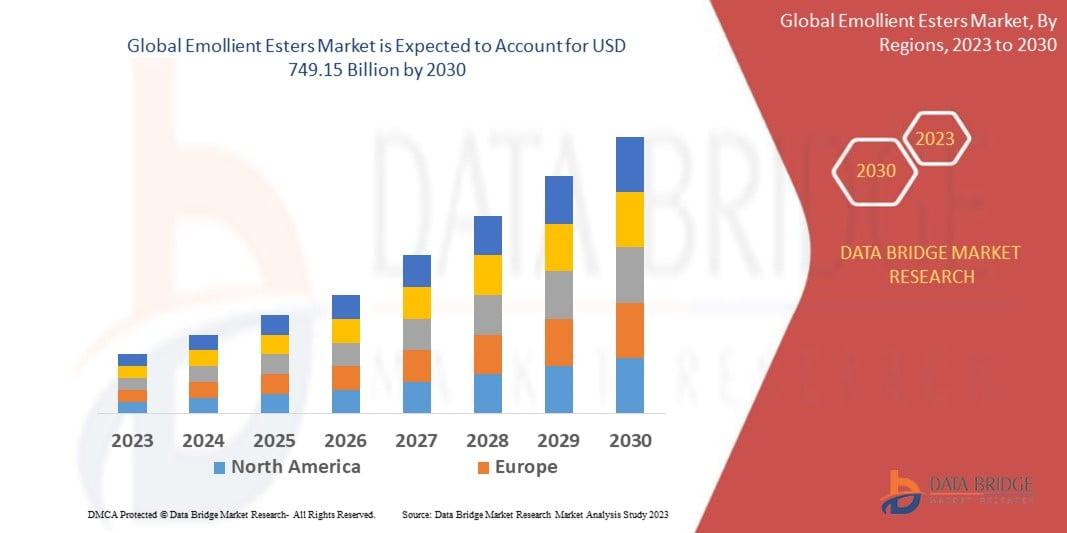

"According to the latest report published by Data Bridge Market Research, the Emollient Esters Market The global emollient esters market is expected to reach USD 801.38 million by 2032 from USD 576.76 million in 2024, growing with a substantial CAGR of 4.30% in the forecast period of 2025 to 2032. An excellent Emollient Esters Market research report is a great store to acquire current...

A healthy, complete smile plays an important role in your confidence, oral health, and overall quality of life. Unfortunately, tooth loss can occur due to injury, decay, gum disease, or other dental conditions. Missing teeth can affect your ability to eat, speak, and smile comfortably. Fortunately, modern dentistry offers highly effective solutions for tooth replacement, and one of the most...

India’s aviation industry is entering a major growth phase. Airlines are expanding fleets, airports are being built across the country, and the demand for trained pilots is rising every year. As the aviation sector continues to grow, the need for high-quality pilot training institutions has become more important than ever. Becoming a professional pilot is not simply about flying an...