Examining The Global Competitive Landscape And Trends Within Ultra-Low-Power Microcontroller Market Share

The competitive distribution of market share in the global ultra-low-power microcontroller sector reflects the diverse product requirements and application-specific optimization priorities that characterize different IoT and embedded market segments. A thorough examination of the Ultra-Low-Power Microcontroller Market share reveals that while established microcontroller vendors including STMicroelectronics, Texas Instruments, and Renesas maintain significant aggregate market share through their broad product portfolios and extensive customer relationships, specialized ultra-low-power focused vendors including Nordic Semiconductor and Silicon Labs have captured disproportionate share in wireless IoT applications where their product focus on optimized wireless power consumption and comprehensive wireless protocol support creates decisive competitive advantages for connected device designers.

Geographically, market share reflects the distribution of IoT device manufacturing activity and the different priority weightings placed on energy efficiency across major markets. Asia-Pacific, and particularly China, represents the largest manufacturing volume market for ultra-low-power microcontrollers as the concentration of consumer electronics, wearables, and IoT device manufacturing in Chinese factories drives extraordinary component volumes. North America represents the highest-value market where medical device, industrial IoT, and precision agricultural applications command premium product pricing that rewards the most sophisticated ultra-low-power capabilities. Europe shows strong demand driven by smart metering, building automation, and industrial sensor applications where the combination of wireless connectivity and multi-year battery requirements perfectly matches ultra-low-power microcontroller capabilities.

The influence of wireless connectivity standard dynamics on competitive market share is particularly significant in the IoT segment, where the choice of wireless connectivity protocol—Bluetooth Low Energy, Zigbee, Thread, Z-Wave, LoRaWAN, or proprietary Sub-GHz—often determines which microcontroller vendors can serve specific application requirements. The fragmentation of IoT wireless standards has created specialized competitive advantages for vendors that have deeply optimized their microcontrollers for specific protocol stacks, as the combination of radio hardware integration and optimized protocol software stack represents barriers that generalist vendors cannot easily overcome. Nordic Semiconductor's dominance in Bluetooth Low Energy applications reflects this dynamic, where their product focus has created accumulated optimization advantages across both hardware and software that competitors have struggled to match.

Finally, the future of ultra-low-power microcontroller market share will be significantly influenced by the competitive dynamics around TinyML and edge AI capabilities as machine learning inference becomes a standard requirement for differentiated IoT products. Silicon vendors that develop the most energy-efficient neural network acceleration capabilities within ultra-low-power power budgets—enabling meaningful AI inference from coin cell batteries or harvested energy—will capture growing share of the high-value connected device market where AI capabilities enable the differentiated product experiences that command premium pricing and strong customer preference.

Top Report:

Accounting Professional Service Market

Categories

Read More

As per Market Research Future analysis, the Autonomous Farm Equipment Market Size was estimated at 33.2 USD Billion in 2024. The Autonomous Farm Equipment industry is projected to grow from 40.28 USD Billion in 2025 to 278.74 USD Billion by 2035, exhibiting a compound annual growth rate (CAGR) of 21.34% during the forecast period 2025 - 2035. The increasing adoption of precision agriculture...

Are you looking to take into your home a strict and loving dog? Knowing about the Pitbull Dog Price in India is essential before you start looking for the breed. Pitbulls are well known for being loyal, intelligent, protective dogs; however, they also require responsible breeding, Puppy Needs Training. ZoodleApp makes it easy to find trusted pet sitters, dog walkers, and world-class care all...

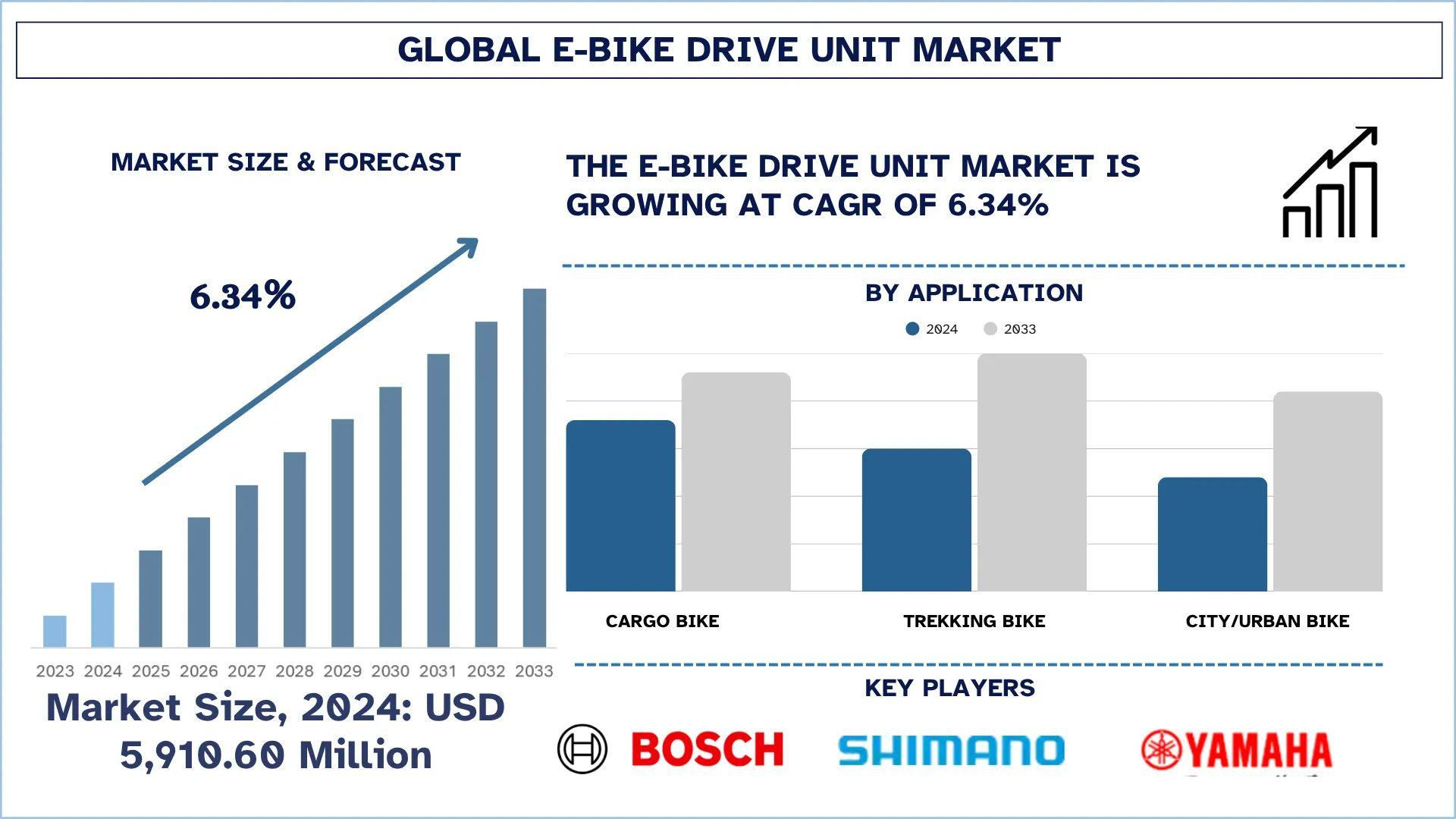

According to UnivDatos analysis, the rising demand for efficient, eco-friendly transportation and continuous technological advancements are the major factors driving the growth of the E-Bike Drive Unit market. As per their “E-Bike Drive Unit Market” report, the global market was valued at USD 5,910.60 million in 2024, growing at a CAGR of about 6.34% during the forecast period from...

Market Overview Endoscope cleaning timers play a crucial role in ensuring that medical devices used in gastrointestinal, respiratory, and urological procedures are properly reprocessed before reuse. These devices help healthcare professionals maintain accurate timing for pre-cleaning, manual cleaning, enzymatic soaking, high-level disinfection, rinsing, and drying stages. The U.S. Endoscope...

When homeowners think about insulating their houses, they usually focus on attics or walls. However, one of the most overlooked areas is the crawl space. Crawl space insulation plays a critical role in maintaining indoor comfort, protecting your home from moisture damage, and improving energy efficiency. For homeowners in Kent, WA, proper crawl space insulation is especially important because...