How to Coordinate Health Insurance Claims When Both Spouses Have Separate Policies

Health insurance plays a crucial role in safeguarding families against rising medical expenses. In many households today, both spouses are employed and covered under separate health insurance policies provided either by their employers or purchased individually. While having multiple policies can enhance financial protection, it can also create confusion when it comes to filing claims.

Questions such as which policy should be used first, whether claims can be made under both policies and how reimbursement works often arise during hospitalisation. Understanding the process of coordinating claims between multiple policies can help families maximise their insurance benefits while ensuring a smoother claims experience.

For individuals evaluating comprehensive health plans for family, understanding how multiple health insurance policies work together is essential for effective healthcare and financial planning.

This article explains how policyholders can coordinate health insurance claims when both spouses have separate health insurance policies.

Why Do Couples Have Separate Health Insurance Policies?

There are several reasons why spouses may hold separate health insurance policies.

These include:

-

Employer-provided group health insurance for each spouse.

-

Individually purchased health insurance policies.

-

Existing family floater policies purchased before marriage.

-

Additional top-up or super top-up policies.

-

Separate policies maintained for enhanced financial security.

Having multiple policies can offer several advantages, including increased overall coverage and broader healthcare access.

Is It Possible to Claim Under Two Health Insurance Policies?

Yes. If both spouses have separate health insurance policies, it is generally possible to claim under more than one policy, subject to policy terms and conditions.

However, policyholders cannot receive reimbursement exceeding the actual medical expenses incurred.

The purpose of multiple policies is to share the financial burden rather than generate financial gain.

Understanding this principle is important while managing claims under health plans for family.

Understanding Contribution and Claim Sharing

Historically, insurers often followed the principle of contribution, under which multiple insurers shared claim expenses proportionately.

However, current regulations provide greater flexibility to policyholders.

Policyholders may generally choose the insurer with whom they wish to file the claim first. If the entire claim amount is not settled due to policy limits or other admissible restrictions, the remaining eligible amount may subsequently be claimed from the second insurer.

This flexibility can simplify claim management for families with multiple policies.

Which Policy Should Be Used First?

There is no universally applicable rule. However, policyholders often consider the following factors:

Employer Group Policy First

Many individuals prefer to utilise employer-provided insurance before using personal policies because:

-

Group policies may not offer lifelong renewability.

-

Coverage may cease upon resignation or retirement.

-

Group policies often have lower waiting periods.

Using employer coverage first can preserve benefits available under personal insurance plans.

Personal Policy First

Some policyholders may prefer using their individual policy first, especially if:

-

The policy offers higher coverage.

-

Cashless treatment is available.

-

The insurer provides faster claim settlement.

The choice ultimately depends on individual circumstances and policy features.

Individuals comparing health plans for family should understand how multiple policies can complement each other.

Scenario 1: Cashless Claim Under One Policy and Reimbursement Under Another

A common approach involves:

-

Availing cashless treatment through one insurer.

-

Obtaining settlement for eligible expenses under that policy.

-

Claiming the unpaid balance from the second insurer through reimbursement.

For example:

-

Total hospital bill: ₹6 lakh

-

First insurer pays: ₹4 lakh

-

Remaining payable amount: ₹2 lakh

The policyholder may submit a reimbursement claim for the remaining admissible expenses under the second policy.

Proper documentation is essential in such cases.

Scenario 2: Reimbursement Claim Under Both Policies

If cashless treatment is unavailable, policyholders may pay the hospital bill directly and subsequently seek reimbursement.

The general process involves:

Step 1: Submit Claim to the First Insurer

The policyholder submits:

-

Original hospital bills

-

Discharge summary

-

Diagnostic reports

-

Prescriptions

-

Claim form

The insurer processes the claim and settles the admissible amount.

Step 2: Obtain Claim Settlement Documents

After settlement, the first insurer usually provides:

-

Claim settlement summary

-

Attested copies of bills and records

-

Claim payment advice

Step 3: Submit Remaining Claim to the Second Insurer

The policyholder may then submit:

-

Attested copies of medical documents

-

Settlement summary from the first insurer

-

Claim form for the second insurer

The second insurer evaluates the balance amount for reimbursement.

Documents Required for Multiple Insurance Claims

When coordinating claims between two policies, policyholders generally require:

-

Original hospital bills

-

Hospital discharge summary

-

Doctor's prescriptions

-

Diagnostic reports

-

Claim forms

-

Pharmacy bills

-

Identity proof

-

First insurer's settlement letter

-

Attested copies of documents

Maintaining organised records can significantly simplify claim processing.

Importance of Informing Both Insurers

Transparency is essential when filing claims under multiple policies.

Policyholders should disclose:

-

Details of all existing health insurance policies.

-

The insurer through which the primary claim is being made.

-

Amount already settled by another insurer.

Non-disclosure may lead to delays or complications during claim assessment.

Comprehensive health plans for family function more effectively when policyholders maintain clear communication with insurers.

Can Both Spouses Cover Each Other Under Their Policies?

Yes, in many cases spouses may be covered under:

-

Their own employer group policy.

-

Their spouse's family floater policy.

-

Separate individual policies.

Such overlapping coverage can provide additional financial security.

However, policyholders should review policy documents carefully to understand:

-

Eligibility criteria.

-

Coverage limits.

-

Waiting periods.

-

Exclusions.

Benefits of Having Multiple Health Insurance Policies

Maintaining separate policies can offer several advantages.

Enhanced Coverage

Combined coverage may help meet rising healthcare costs.

Reduced Out-of-Pocket Expenses

Higher overall coverage can minimise personal expenditure during major medical events.

Access to Larger Hospital Networks

Different insurers may have different empanelled hospitals, improving healthcare accessibility.

Better Financial Flexibility

Multiple policies provide flexibility in structuring claims.

These advantages make comprehensive health plans for family particularly valuable for growing households.

Common Challenges in Coordinating Multiple Claims

Despite the advantages, certain challenges may arise.

Documentation Complexity

Managing paperwork for multiple insurers can be time-consuming.

Delays in Claim Processing

Claims involving more than one insurer may require additional verification.

Understanding Policy Terms

Different policies may have varying:

-

Waiting periods

-

Exclusions

-

Coverage limits

-

Claim procedures

Policyholders should familiarise themselves with policy provisions beforehand.

Tips for Smooth Claim Coordination

To ensure hassle-free claim settlement:

Maintain Updated Policy Records

Keep copies of all health insurance documents readily accessible.

Understand Coverage Details

Review:

-

Sum insured

-

Sub-limits

-

Exclusions

-

Network hospitals

Notify Insurers Promptly

Inform insurers immediately upon hospitalisation.

Preserve Medical Documents Carefully

Retain:

-

Bills

-

Prescriptions

-

Investigation reports

-

Discharge summaries

Seek Clarification When Needed

Contact insurer customer support if any aspect of the claim process is unclear.

Factors to Consider While Purchasing Family Health Insurance

When evaluating health plans for family, families should consider:

-

Adequate sum insured.

-

Extensive hospital network.

-

Cashless treatment facilities.

-

Maternity and newborn benefits.

-

Restoration benefits.

-

Waiting periods.

-

Claim settlement support.

-

Lifetime renewability.

A comprehensive approach ensures long-term healthcare protection.

Conclusion

When both spouses have separate health insurance policies, coordinating claims effectively can help maximise available coverage and reduce out-of-pocket expenses. Understanding how cashless and reimbursement claims work, maintaining proper documentation and communicating transparently with insurers are essential for a seamless claim experience.

Comprehensive health plans for family become even more valuable when policyholders understand how to utilise multiple policies strategically. Proper planning can ensure better financial preparedness and uninterrupted access to quality healthcare.

Niva Bupa offers comprehensive health insurance solutions designed to meet the evolving healthcare needs of modern families. With extensive coverage options, broad hospital networks, customer-centric services and efficient claims support, Niva Bupa helps families navigate medical expenses with greater confidence and peace of mind.

Catégories

Lire la suite

Memories of MU Ignition's beta phase still linger, but launch day now feels like a distant echo. Just two weeks post-release, the game unveils its inaugural content expansion. The level ceiling has been lifted to 400, a substantial leap—whether from 300 or another figure, it marks a significant climb for adventurers. Fresh zones await exploration, while Blade Knights, Soul Masters, and...

In today’s competitive market, a strong brand presence at trade shows and exhibitions is essential for businesses to stand out. An effective exhibition design can attract attention, engage visitors, and leave a lasting impression. Innovation Dynamics, a leading Exhibition Design Company in Dubai, specializes in transforming creative concepts into high-impact exhibition experiences. This...

The popularity of Online Slot Game Malaysia continues to rise as more players look for exciting, easy and rewarding gaming experiences. Online slot games have become one of the top choices because they are simple to play, offer great bonus features and provide opportunities for big jackpots. In Malaysia, players can now enjoy slot gaming anytime through trusted online platforms. With modern...

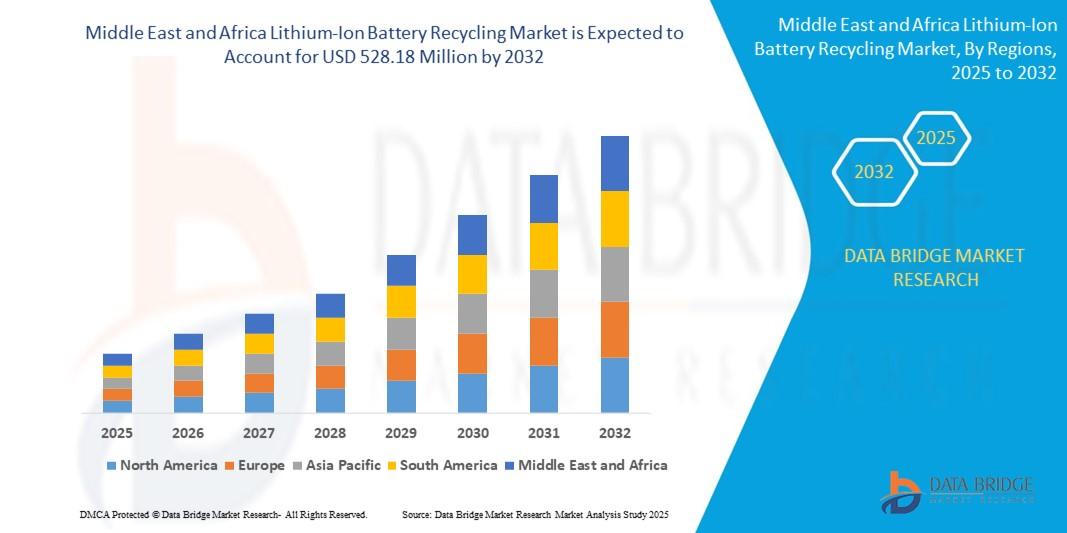

The Middle East and Africa Lithium-Ion Battery Recycling Market is positioned for robust growth, driven primarily by the escalating adoption of Electric Vehicles (EVs) and significant investments in renewable energy storage solutions across the region, particularly in the Gulf Cooperation Council (GCC) countries and South Africa. Governments are increasingly implementing stringent...

SUNWIN is an emerging online entertainment platform that has gained attention among gaming enthusiasts for its wide range of digital gaming options and user-friendly experience. Designed to provide seamless access to entertainment anytime and anywhere, SUNWIN continues to attract players who enjoy online casino-style games and interactive betting experiences. One of the key highlights...