The Ultimate Breakdown: Conventional Mortgage Benefits and Limits

The journey toward homeownership is often paved with questions about the best way to leverage your capital. In a real estate market that continues to evolve, a conventional loan remains the gold standard for many buyers. Unlike government-backed options, these loans are governed by private lenders and must adhere to specific "conforming" limits set by the Federal Housing Finance Agency. Choosing this path often signals to sellers that you are a well-qualified buyer, which can be a significant advantage in competitive bidding wars. However, navigating the intersection of loan ceilings and your personal savings requires a clear understanding of the rules that apply to today’s properties.

For 2026, the baseline limit for a single-family home has seen a notable increase, reflecting the steady rise in national property values. In most counties, the maximum amount you can borrow while still falling under the standard conforming guidelines is now $832,750. This expansion provides more breathing room for buyers in mid-priced markets who want to avoid the stricter requirements of jumbo financing. By understanding these boundaries, you can better align your search with a mortgage product that offers the most flexibility for your long-term financial health.

Understanding Modern Conforming Boundaries

When you exceed the baseline limits set for your specific area, you move into the territory of non-conforming or "jumbo" loans. These typically come with higher interest rates and more stringent credit score demands. Knowing where these lines are drawn helps you avoid unexpected hurdles during the underwriting process. In high-cost regions, such as parts of California or the Northeast, the limits are significantly higher to accommodate the local market realities.

2026 Conforming Loan Limits by Property Type

The table below outlines the maximum borrowable amounts for properties in standard-cost areas versus designated high-cost regions for the current year.

|

Number of Units |

Standard Baseline Limit |

High-Cost Area Ceiling |

|

Single-Family Home |

$832,750 |

$1,249,125 |

|

Duplex (2 Units) |

$1,066,250 |

$1,599,375 |

|

Triplex (3 Units) |

$1,288,800 |

$1,933,200 |

|

Fourplex (4 Units) |

$1,601,750 |

$2,402,625 |

Strategies for Low-Capital Entry

A common hurdle for many first-time buyers is the belief that a massive upfront payment is the only way to secure a private mortgage. You might be wondering, can you buy a house with no money down through these traditional channels? While 100 percent financing is typically reserved for specialized government programs like the VA or USDA, there are specific private products that come very close. For instance, some lenders offer 3 percent down programs specifically for first-time buyers or those within certain income brackets.

If you find that you are just short of the cash needed for a deposit, you can explore no down-payment home loans that utilize secondary financing. This "piggyback" structure involves taking out a primary mortgage for 80 percent of the value and a second loan to cover the remaining portion. This can sometimes allow a buyer to enter the market with very little out-of-pocket cash while still benefiting from the structure of a private mortgage. It is a strategic way to bypass the need for a massive savings account if your income is strong enough to support the double payment.

Determining Your Upfront Investment

When calculating your budget, the most pressing question is often: how much of a down payment do i need for a house to get the best possible terms? While 3 percent is the floor for many, putting down 20 percent remains the milestone for avoiding private mortgage insurance (PMI). This insurance is a monthly fee that protects the lender, but it adds no value to your equity. By contributing more upfront, you not only eliminate this fee but also generally secure a lower interest rate, which can save you thousands over the life of the loan.

However, putting 20 percent down isn't always the smartest move if it leaves you with zero cash in your emergency fund. Modern financial wisdom often suggests a balanced approach:

· 3% to 5% Down: Ideal for first-time buyers who want to keep cash liquid for repairs and furniture.

· 10% Down: A middle ground that often results in lower insurance premiums and better rate tiers.

· 20% Down: The gold standard for the lowest monthly payment and immediate equity.

The Benefits of Private Financing

Beyond the numbers, private mortgages offer several qualitative benefits. Because they are not government-insured, they often have less "red tape" regarding the condition of the home. This makes them a favorite for buyers looking at homes that might need a little cosmetic work, which can sometimes disqualify an FHA or USDA loan. Furthermore, once you reach 20 percent equity—either through paying down the balance or through home value appreciation—you can request to have your mortgage insurance removed. This "automatic raise" is one of the most attractive features of the conventional path.

Final Checklist for Conforming Loan Success

· Verify the specific loan limit for your county, as high-cost areas vary significantly.

· Check your credit score; a 620 is the typical minimum, but 740+ gets you the best rates.

· Obtain a pre-approval letter to show sellers you have the backing of a private lender.

· Review your Debt-to-Income (DTI) ratio, aiming to keep it below 43 percent for the easiest approval.

· Compare Loan Estimates from at least three lenders to ensure you are getting the lowest fees.

By understanding the limits and the leverage available to you, you can move forward with a plan that protects your savings while securing your future. Whether you choose to go in with a small deposit or a large one, the private mortgage path offers a clear and reliable roadmap to the front door of your new home.

Categorias

Leia mais

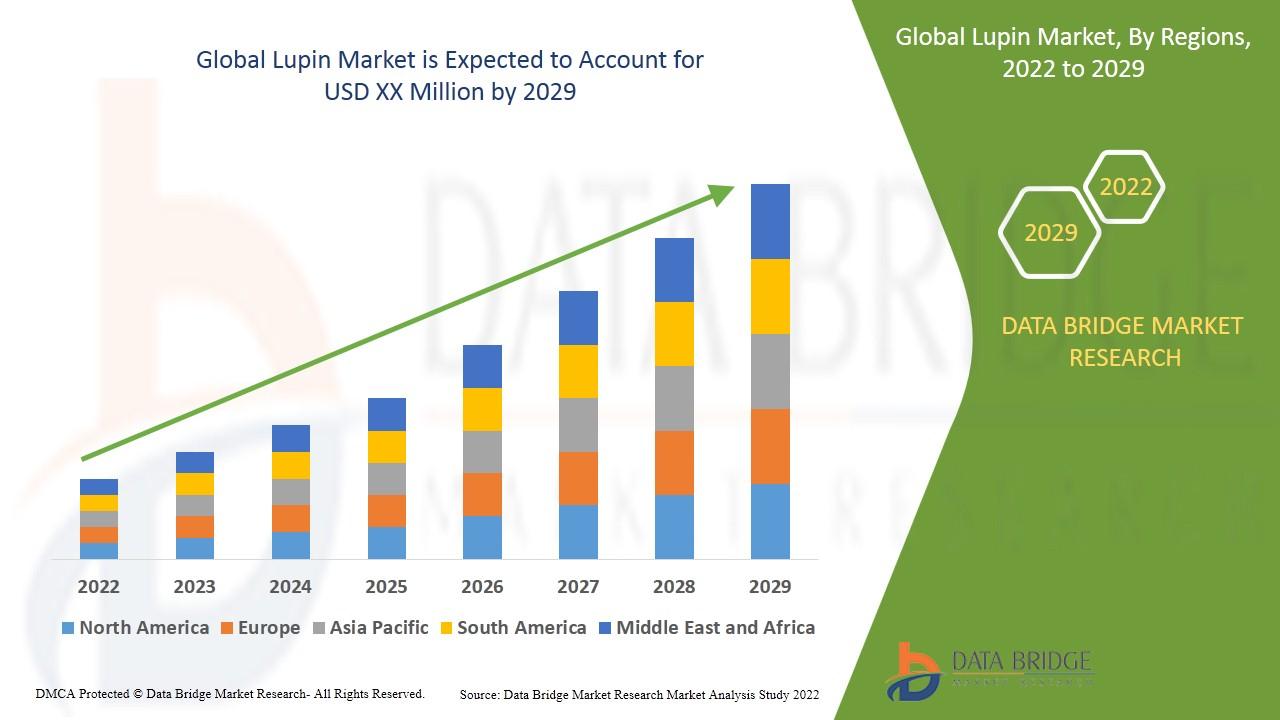

"Executive Summary Lupin Market Size and Share Forecast CAGR Value Data Bridge Market Research analyses that the global lupin market will grow at a CAGR of 4.45% during the forecast period of 2022-2029. This Lupin Market research report is a great resource that makes available current as well as upcoming technical and financial details of the Lupin Market industry for the...

Halloween is no longer limited to costumes worn for just one night. Modern fashion has transformed Halloween into a full seasonal style moment, especially for men who want to look festive without going over the top. Halloween jackets and coats have become a popular choice, blending spooky aesthetics with everyday wearability. From subtle dark tones to bold statement pieces, Halloween...

Premier League TOTS 2026 Kurzfassung: In Woche zwei der Team of the Season-Events von EA FC 26 stehen die englischen Ligen im Zentrum: Premier League TOTS, Women’s Super League (BWSL) TOTS und das EFL Combined TOTS. Viele Top-Spieler der Saison 2025/2026 sind für eine Woche als Special-Karten in Ultimate Team erhältlich.\n Highlights: Bei den Herren finden sich Namen wie Erling...

If you’re looking to start online betting in India, getting a Mahadev Book ID is your first step. With the growing popularity of cricket betting and live sports platforms, Mahadev Book has become one of the most searched platforms in 2026. In this beginner-friendly guide, you’ll learn how to get a Mahadev Book ID, how it works, and important tips to get started...

In the confectionery industry, the Automatic Rainbow Lollipop Machine has become an essential tool for producing vibrant, high-quality lollipops efficiently. By automating critical stages such as candy forming, color layering, and stick insertion, this equipment allows manufacturers to maintain consistent quality while increasing production capacity. Its precise control systems enable...