Financing Property Renovations Through Tailored Mortgage Products

Entering the world of real estate often feels like learning a new language, especially when you are looking at properties that need a little extra care. For many hopeful buyers, the standard path of buying a move-in-ready home is either too expensive or simply unappealing compared to the charm of an older house. This is where a renovation mortgage becomes a vital piece of the puzzle. It is a financial tool that allows you to borrow based on the future value of the property, meaning you can fund the purchase and the subsequent repairs through one single loan. This approach eliminates the need for separate high-interest personal loans to cover construction costs.

The Standard of Living and Safety

When you use government-backed funding to fix up a home, the goal is to create a space that is not only beautiful but also fundamentally safe. Lenders have a vested interest in ensuring the collateral for their loan is in good condition. Because of this, there are certain fha required repairs that must be addressed during the construction phase. These requirements focus on the primary functions of a home, such as a sturdy roof, a reliable heating system, and the absence of any health hazards like mold or lead paint. Ensuring these items are fixed first provides a solid foundation for the more exciting cosmetic changes you have planned.

It is helpful to view these requirements as a blueprint for a healthy home. While it might be tempting to prioritize a spa-like bathroom, the program ensures that the plumbing and electrical systems are up to modern standards first. This protects the homeowner from moving into a house that looks great on the surface but hides expensive and dangerous secrets behind the walls. By following these guidelines, you ensure that your investment is sound and your family is protected from day one.

Understanding Geographic Loan Ceilings

One of the most important pieces of information for any buyer is knowing exactly how much purchasing power they have. This power is often dictated by local economic conditions. Every year, the government sets the max fha loan amount for every county in the country. This figure represents the absolute limit of what you can borrow, including both the price of the home and the renovation escrow. If you live in an area where property values are high, your limit will be adjusted upward to reflect that reality, while more affordable markets have lower ceilings.

Knowing this number helps you filter your property search. If you know the limit in your target neighborhood is $450,000, and you find a house for $350,000 that needs $150,000 in work, you quickly realize that the project might exceed the allowable limits. Being aware of these financial boundaries early on saves time and prevents the frustration of falling in love with a project that the numbers simply won't support.

Long-Term Financial Management

The journey of homeownership does not end when the construction dust settles. As the market changes and you build equity in your newly renovated space, you may find that your initial loan terms are no longer the most beneficial. Many homeowners eventually decide to refinance an fha mortgage to take advantage of lower interest rates or to move into a conventional loan. This transition can often lead to the removal of monthly mortgage insurance, which can put a significant amount of money back into your pocket every month.

Refinancing is also a common strategy for those who want to tap into the increased value of their home for future projects. If your $300,000 fixer-upper is now worth $500,000 thanks to your renovations and a rising market, you have a wealth of equity at your disposal. This can be used for further improvements, education costs, or consolidating other debts, making your home a powerful engine for your overall financial health.

Key Features of Renovation Loans

-

Bundled costs: One application, one closing, and one monthly payment for both home and repairs.

-

Lower down payments: Accessibility is a major feature, often requiring as little as 3.5 percent down.

-

Appraisal based on future value: The loan is based on what the home will be worth after the work is done.

-

Professional oversight: Use of licensed contractors ensures the work is completed correctly and on time.

-

Escrow protection: Funds for repairs are held safely and paid out as work milestones are reached.

Comparing Improvement Priorities

|

Improvement Type |

Primary Benefit |

Urgency |

|

Roofing and Siding |

Weather protection and durability |

High |

|

HVAC and Insulation |

Energy efficiency and daily comfort |

High |

|

Interior Floor Plan |

Modern flow and usability |

Medium |

|

Landscaping and Decks |

Curb appeal and outdoor living |

Low |

Final Thoughts on Property Transformation

Building a home through a renovation process is an informative experience that teaches you the ins and outs of the real estate market. It requires patience and a willingness to work within a structured financial framework, but the rewards are substantial. You end up with a property that is tailored to your specific tastes, updated to modern safety standards, and potentially worth far more than your total investment. By staying informed about your local borrowing limits and prioritizing essential safety repairs, you can navigate the process with confidence and clarity.

Whether you are a first-time buyer looking for a way into a competitive neighborhood or a current homeowner wanting to revitalize your space, these financial tools provide a pathway to success. Keep your eye on the numbers, choose your contractors wisely, and enjoy the process of turning an overlooked house into the pride of the neighborhood. With the right information and a solid plan, the home of your dreams is well within reach.

Categories

Read More

Godspeed Clothing: In a fashion world saturated with logos and recycled trends, Godspeed Clothing stands out by offering more than just garments it delivers a mindset. The name itself carries weight. “Godspeed” is a blessing for the journey ahead, and that idea is woven directly into the brand’s identity. Every piece reflects motion, ambition, and the quiet confidence of...

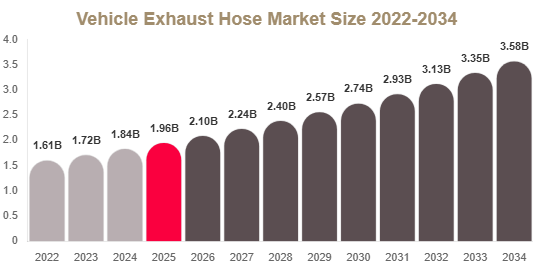

Vehicle Exhaust Hose Market Overview The global vehicle exhaust hose market is witnessing steady growth due to increasing vehicle production, rising demand for emission control systems, and growing focus on workplace safety in automotive repair and maintenance facilities. Vehicle exhaust hoses are essential components used to safely remove harmful exhaust gases and fumes generated by vehicle...

Vegetable Juice Concentrates: A Nutrient-Dense Ingredient Driving Modern Food Innovation Vegetable juice concentrates are highly concentrated forms of vegetable juice produced by removing water content through evaporation or filtration processes. This results in a dense, flavorful ingredient that retains the nutritional profile, color, and functional properties of fresh vegetables while...

Fecal Immunochemical Diagnostic Test (FIT) Market: Comprehensive Overview, Trends, and Growth Outlook Fecal Immunochemical Diagnostic Test (FIT) Market Overview The Fecal Immunochemical Diagnostic Test (FIT) Market is projected to experience significant growth between 2025 and 2035, driven largely by the increasing prevalence of colorectal cancer (CRC) worldwide and the...

In modern households, the care of pets is no longer limited to basic feeding; it is increasingly guided by convenience, precision, and wellness. The Intelligent Pet Food Dispenser by Pawtechpet brings these aspects together, offering a device that blends smart technology with thoughtful design to simplify daily routines while ensuring pets'nutrition remains consistent and timely. The rise of...