Best Practices for Achieving Success With FHA Rehab Loans

Embarking on a home renovation project is a major life event that requires a mix of vision, grit, and financial savvy. For many, the most effective way to finance this dream is through an fha rehab loan, which allows you to purchase a property and renovate it using a single mortgage. While the prospect of custom-building your living space is exciting, the process involves navigating specific regulations and managing a complex timeline. Success depends on your ability to stay organized and proactive from the moment you start scouting properties until the final coat of paint dries.

Preparation is the secret ingredient to a smooth renovation experience. You need a team of professionals who are not only skilled in their trades but also familiar with the specific paperwork requirements of government-backed lending. This isn't the time for shortcuts or handshake deals. By following a structured approach, you can avoid the common pitfalls that often derail first-time renovators and turn a stressful process into a rewarding investment in your future.

Prepare for the Inspection Phase

One of the first hurdles you will encounter is ensuring the property can actually be transformed into a safe residence. You should familiarize yourself with the fha appraisal guidelines early in the process. These are not just suggestions; they are the minimum standards a home must meet to be considered habitable. If you walk into a potential house and see exposed wiring or a cracked foundation, you need to be ready to address those issues in your formal renovation plan.

Working with a qualified inspector can save you thousands of dollars in the long run. They can identify "red flag" items that must be fixed to satisfy the lender. Common areas of focus include:

-

Structural integrity including the roof, walls, and foundation

-

Operational HVAC, plumbing, and electrical systems

-

Lead-based paint mitigation for older properties

-

Adequate drainage and site grading to prevent flooding

-

General health and safety hazards like mold or asbestos

Budget Within Your Regional Boundaries

Every borrower needs to know exactly how much they can spend before they start picking out tile patterns. Your total loan amount, which includes the purchase price and the renovation budget, is capped by a specific fha limit. This number is determined by the county where the home is located and is updated annually to reflect market trends. If you exceed this amount, you will have to pay the difference out of your own pocket, which can significantly impact your cash flow during the project.

To help you plan, here is a comparison of how these boundaries might look in different market types:

|

Market Type |

Cost Considerations |

Impact on Renovation |

|

Low-Cost Area |

Lower entry price |

More room for extensive upgrades within the cap |

|

Moderate-Cost Area |

Balanced pricing |

Requires careful prioritization of repairs |

|

High-Cost Area |

High entry price |

Limit may be reached quickly with minor repairs |

Select Your Team Wisely

The success of your project rests largely on the shoulders of your general contractor. Because the funds are released in stages, your contractor must be financially stable enough to start work before receiving the first payment. They also need to be comfortable with the administrative side of the loan, including providing detailed bids and sticking to a strict timeline. Here are a few tips for choosing the right partner:

-

Verify licenses and insurance coverage for all subcontractors

-

Ask for references specifically from clients who used renovation loans

-

Ensure the contractor provides a highly detailed "Scope of Work" document

-

Establish a clear communication schedule for weekly updates

Plan Your Long-Term Financial Exit

Once the dust has settled and you are living in your beautiful new home, it is time to look at the bigger financial picture. Many homeowners find that the value of their renovated property has increased significantly. This newfound equity opens the door for refinancing an fha loan in the future. Moving into a conventional mortgage can be a great way to eliminate the monthly mortgage insurance premiums that stay with these loans for their entire term if you put down less than ten percent.

Timing your refinance is a strategic move. You should keep an eye on interest rates and your local property values. If your home has appreciated enough that you now own 20% equity, a refinance could lower your monthly overhead and put you in a stronger financial position. Thinking about this "exit strategy" before you even start the renovation ensures that you are treating your home not just as a shelter, but as a growing asset.

Mastering the Move-In

The final weeks of a renovation are often the most hectic. You will be coordinating final inspections, signing off on the last draw requests, and planning your actual move. Stay diligent with your paperwork until the very end. Once the final inspection is passed and the lender closes the renovation escrow, you can breathe a sigh of relief. You have successfully navigated a complex system to create a home that is uniquely yours, likely at a better price point than if you had bought a turnkey property in the same neighborhood.

Stay focused on the goal. There will be days when the noise and the dust feel overwhelming, but the reward is a modern, safe, and personalized space. By keeping these tips in mind—staying within the loan caps, following safety guidelines, and planning for a future refinance—you turn a complicated real estate transaction into a masterpiece of personal and financial achievement.

Категории

Больше

Introduction The Indian Premier League is known for its electrifying rivalries, where every match carries extra pressure, emotion, and excitement. From historic clashes like Mumbai vs Chennai to high-intensity contests such as Bangalore vs Kolkata, these games always attract massive attention from cricket fans. During such moments, Dafabet login becomes a highly searched keyword as fans look...

B52 Club is an exciting and user-friendly gaming platform that brings together a wide range of reward-based games for players who enjoy fun, challenge, and entertainment. Whether you are using iOS, Android, or a PC, this platform offers smooth access and a comfortable experience for everyone. With its diverse game collection, including popular options like Tien Len, Poker, Phom, and Slot...

AFK Journey Season 4 is set to launch on 23 May 2025, running for four months with a restructured three‑phase format. The first two phases each last five weeks, while the third phase remains active until the season ends. Each phase introduces its own AFK Stages, a new Resonance Level, and a distinct Primal Lord boss, with maximum stage progression unlocking special challenge stages, server‑wide...

Many buyers spend time comparing different cannabis options before making a purchase decision. Product quality often depends on cultivation methods, storage practices, and harvesting standards. Reading descriptions carefully helps people understand what they are getting before placing any order. Reliable sellers usually provide detailed information about cannabinoid content, appearance, aroma...

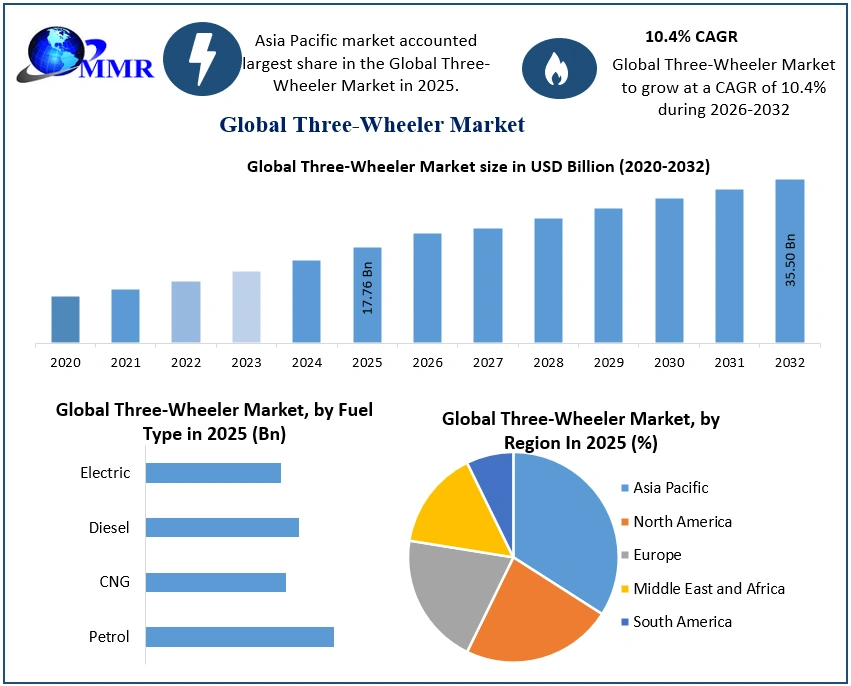

Global Three-Wheeler Market Worth USD 12.8 Billion in 2024 to Reach USD 24.6 Billion by 2033 at 7.5% CAGR Amid EV Revolution and Smart Mobility Transformation The global Three-Wheeler Market is entering a transformative growth era as electric mobility adoption, smart transportation ecosystems, connected vehicle technologies, and sustainable urban mobility solutions redefine the...