Clear Steps for Navigating and Applying for a Rehabilitation Loan

Taking a house from a state of disrepair to a stunning sanctuary is a journey that requires a solid roadmap. While the idea of remodeling a fixer-upper is exciting, the financial logistics can feel overwhelming if you do not have a clear sequence of events to follow. Many people find that the fha renovation loan provides the perfect structure for this adventure, allowing for a streamlined approach to funding both the acquisition and the construction. By following a specific set of steps, you can ensure that your project stays on track and that you move into your improved home without unnecessary delays or financial surprises.

Step 1: Financial Prequalification and Planning

Before you ever pick up a hammer or even a real estate brochure, you must establish your borrowing power. This involves meeting with a lender who specializes in government-backed rehabilitation products. They will look at your credit history, income, and overall debt levels to provide a pre-approval letter. This document is essential because it tells sellers that you are a serious buyer with the backing to close a complex deal. During this phase, you should also decide if you are looking for a Limited loan for minor repairs or a Standard loan for major structural changes.

Initial Preparation Tasks

-

Gather your last two years of tax returns and recent pay stubs.

-

Review your credit report for any errors that might affect your interest rate.

-

Determine your maximum comfortable monthly payment including taxes and insurance.

-

Interview at least two lenders to compare their experience with renovation products.

Step 2: Finding the Right Property and Setting the Scope

Once you have your pre-approval, the search begins. You are looking for a house that has potential but perhaps lacks the modern finishes that others desire. As you walk through potential homes, take notes on what needs to be fixed. Once you find the right one and your offer is accepted, you must quickly move into the planning phase. This involves hiring a general contractor to provide a detailed, line-item bid for all the work you intend to perform. This bid is a cornerstone of your loan application.

Step 3: Undergoing the Valuation Process

With your purchase contract and contractor bids in hand, the lender will order an fha home appraisal. This step is unique because the appraiser evaluates the property in its current state while also projecting what it will be worth after the work is completed. They will carefully check that the home meets safety requirements once the repairs are finished. If the appraiser identifies additional safety issues not included in your original bid, such as faulty wiring or roofing issues, you must add those to your contractor's work write-up to move forward.

Understanding the Appraisal Review

|

Sub-Step |

Action Required |

Desired Outcome |

|

On-site Visit |

Appraiser visits the physical property. |

Identification of all health and safety risks. |

|

Plan Review |

Appraiser looks at contractor bids and floor plans. |

Validation that the upgrades justify the cost. |

|

Valuation Report |

Appraiser issues the final estimated value. |

Confirmation that the loan-to-value ratio is acceptable. |

Step 4: Respecting Regional Funding Caps

As your loan moves through underwriting, the lender will verify that your total mortgage amount stays within the hud fha loan limits for your specific area. Every county has a maximum dollar amount that the government is willing to insure. If your purchase price plus your construction budget exceeds this number, the loan will not be approved unless you pay the difference in cash. Staying within these limits is a crucial step in ensuring your financing remains secure and that you are not over-leveraging yourself in a particular market.

Factors to Watch During Underwriting

-

Double-check the current year's limit for your specific county.

-

Ensure the contractor's bid includes a required contingency buffer.

-

Confirm that the total loan includes any required consultant fees.

-

Verify that the property type matches the limit category (e.g., duplex vs. single family).

Step 5: Closing and Beginning the Transformation

After your loan is approved, you will attend a closing where you officially become the owner. At this point, the funds for the purchase are paid to the seller, and the funds for the renovation are placed in an escrow account. Work must usually begin within thirty days of closing. Your lender will release payments, or draws, to your contractor at specific milestones throughout the project. This ensures that the work is being done correctly and that the money is being used exactly as planned in your original bid.

Step 6: Evaluating Future Opportunities

Once the renovation is complete and you have lived in the home for a while, it is wise to revisit your financial strategy. Many people eventually ask: can i refinance an fha loan if market conditions change? This is the final step in the long-term management of your home investment. If your renovations have significantly boosted your home's value, you might find that you can refinance into a conventional loan to remove mortgage insurance or secure a lower interest rate, further improving your financial position.

Steps for a Successful Future Refinance

-

Maintain a clean record of on-time mortgage payments for at least one year.

-

Keep receipts and photos of all renovations to show the appraiser.

-

Watch the market for a drop in interest rates that justifies the closing costs.

-

Check your home's estimated equity to see if you have reached the 20 percent mark.

Final Walkthrough of the Process

Following these steps turns a complex construction and finance project into a manageable series of tasks. The secret to success lies in your preparation and your choice of partners. By working with experienced professionals and staying organized with your documentation, you can navigate the hurdles of appraisals and loan limits with confidence. The result is not just a house, but a home that has been carefully crafted to meet your needs and a financial asset that is built to grow in value over time.

Remember that the timeline for these loans is often longer than a standard purchase, so patience is a requirement. However, the reward of seeing your vision come to life is well worth the extra effort. Keep your goals in sight, stay in close contact with your lender, and enjoy the process of watching your fixer-upper transform into the best house on the block.

الأقسام

إقرأ المزيد

Market Overview According To The Research Report Published By Polaris Market Research, The Global Human Augmentation Market Was Valued At Usd 130.71 Billion In 2021 And Is Expected To Reach Usd 725.25 Billion By 2030, To Grow At A Cagr Of 22.0% During The Forecast Period. Market SummaryThe Human Augmentation Market is experiencing rapid advancements due to breakthroughs in robotics,...

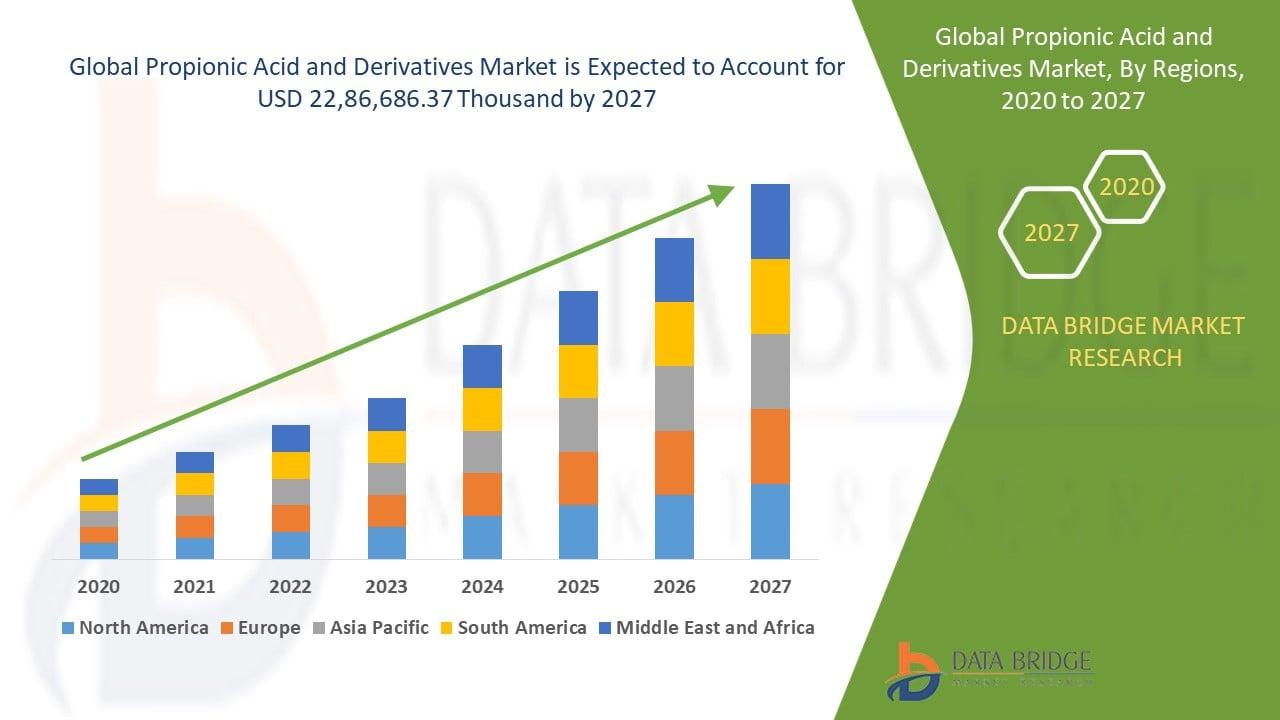

"Comprehensive Outlook on Executive Summary Propionic Acid and Derivatives Market Size and Share The global propionic acid and derivatives market size was valued at USD 1.90 billion in 2024 and is projected to reach USD 3.05 billion by 2032, with a CAGR of 6.10% during the forecast period of 2025 to 2032 The Propionic Acid and Derivatives report encompasses thorough analysis of market...

When buying or selling a property in Danville, a certified termite inspection is a crucial step in the real estate process. Termites and other wood-destroying organisms can cause extensive structural damage long before visible signs appear. Partnering with a certified termite inspection company in Danville, CA ensures your property is carefully evaluated, accurately documented, and...

The Russian lubricants market is witnessing significant growth due to increased industrialization and modernization across multiple sectors. Industrial machinery, automotive engines, and energy systems require high-performance lubricants to ensure smooth operation, reduce friction, and prevent mechanical failures. This has led to heightened demand for premium-grade oils and specialty...

BloomChic women’s plus size clothing has quickly become a favorite among women who want fashion that feels great, looks stylish, and fits real bodies. One of the main reasons shoppers love this brand is the ability to save with abloomchic discount code available through trusted platforms like DealsZo. This allows women to enjoy trendy outfits without overspending while still getting...