The Building Blocks of Modern Real Estate Financing Explained

Entering the world of home ownership involves learning a new language filled with acronyms, percentages, and complex regulations. One of the most significant lessons a prospective buyer can learn is how to leverage specialized financial instruments to improve their living conditions. For many, renovation loans serve as an essential curriculum in wealth building, allowing individuals to acquire properties that might otherwise be overlooked. These programs are specifically designed to help buyers purchase a home and fund necessary repairs or upgrades simultaneously, using the projected value of the home after the work is completed as the basis for the loan. This educational approach to financing turns a dilapidated structure into a viable long-term asset.

A crucial part of the learning curve involves understanding how the government ensures these properties are safe for occupancy. Before any funds are released for a purchase, a professional must conduct an fha inspection to evaluate the home against specific safety criteria. This is a distinct process from a general home inspection, as it focuses strictly on the Minimum Property Requirements set by the Department of Housing and Urban Development. Students of the real estate market should view this as a protective layer that prevents them from buying a home with life-safety issues, such as faulty wiring, structural instability, or inadequate sanitation systems. Understanding these requirements early can save a buyer from entering a contract on a house that cannot be financed under these specific terms.

Understanding Borrowing Boundaries and Regional Variations

One of the first variables to master in your financial education is the concept of lending ceilings. The federal government does not offer a one-size-fits-all loan amount across the country. Instead, the fha maximum loan amount is determined by the specific economic conditions of the county where the property is located. These limits are designed to ensure that the program remains accessible to low-to-moderate-income earners while adjusting for the high costs of certain metropolitan areas. If you are looking at homes in an expensive coastal city, your borrowing limit will be significantly higher than if you were shopping in a rural Midwestern town. Keeping track of these annual adjustments is vital for maintaining an accurate budget during your home search.

|

Loan Element |

Purpose and Function |

|

Primary Financing |

Covers the base purchase price of the home. |

|

Improvement Escrow |

Funds held back specifically for the planned renovations. |

|

Contingency Reserve |

A mandatory safety net for unexpected construction costs. |

|

Mortgage Insurance |

A monthly premium that protects the lender against default. |

For existing homeowners, the educational journey often involves learning how to optimize their current debt. When market conditions change, knowing the fha refinance requirements can lead to significant monthly savings or the ability to switch from a risky loan product to a stable, fixed-rate mortgage. The requirements usually include a minimum credit score, a specific amount of equity in the property, and a clean history of mortgage payments over the previous year. By staying educated on these benchmarks, homeowners can strike when interest rates are favorable, ensuring they are always in the best possible financial position regarding their primary residence.

The Essential Checklist for Property Quality

When evaluating a potential home, it is helpful to look through the eyes of a professional assessor. There are specific non-negotiables that must be addressed to satisfy federal standards. Educating yourself on these points can help you spot "deal-breakers" before you even pay for an official report. Consider the following structural and safety priorities:

-

The presence of lead-based paint in any home built before 1978 must be addressed or stabilized.

-

Roofing must have a remaining life expectancy of at least two years and be free of leaks.

-

Water heaters must be equipped with a pressure relief valve and be properly vented.

-

Crawl spaces and attics must have adequate ventilation to prevent moisture buildup and mold.

-

All bedrooms must have an egress window for emergency exits in case of fire.

-

Electrical panels must be properly labeled and free of exposed or frayed wiring.

By learning these specific points, you become a much more savvy shopper. You can walk into a "fixer-upper" and immediately estimate whether the budget provided by your financing will be enough to bring the house up to code while still leaving room for the cosmetic changes you desire. This prevents the common mistake of spending your entire budget on a beautiful kitchen while the roof still needs a five-figure repair that you cannot afford.

Strategic Management of the Renovation Process

The education continues once the loan is closed and the contractors arrive. Managing a large-scale project requires a different set of skills than simply choosing a house. You must learn to read a work write-up, which is a detailed document outlining every single repair, its cost, and the materials to be used. This document acts as the bible for your project, and the lender will use it to verify that work is being completed before releasing funds. Learning how to manage these "draws" is essential; if a contractor falls behind or does not provide the proper receipts, the flow of money can stop, which can halt your project entirely.

It is also important to understand the role of the consultant in certain loan types. These experts act as an intermediary between the homeowner, the contractor, and the bank. They perform progress inspections and ensure that the quality of work meets the required standards. While their fee is an additional cost, the education and oversight they provide are often invaluable for first-time renovators who might not know how to spot a shortcut or a structural error made by a subcontractor.

Building Equity Through Knowledge and Persistence

The ultimate goal of this educational journey is to create a home that is both a sanctuary and a source of financial strength. Real estate is historically one of the most reliable ways to build generational wealth, but it requires a commitment to maintenance and smart upgrades. By staying informed about the market and the various financial tools available, you can navigate the complexities of home ownership with confidence. Whether you are using your initial loan to save a historic home from demolition or you are meeting the necessary criteria to lower your monthly payments, the knowledge you gain along the way is your most valuable asset.

Getting a renovated home is paved with information. From knowing the local limits of your borrowing power to understanding the nuances of property inspections, every piece of data helps you make better decisions. Take the time to ask questions of your lender, your inspector, and your contractor. A well-informed homeowner is a successful homeowner, and the effort you put into learning the process today will pay dividends in the form of a beautiful, safe, and valuable home tomorrow.

Categorías

Read More

The Din Rail Ethernet Switches Market Analysis provides a comprehensive overview of the current state and future potential of this critical sector. The analysis highlights key drivers, challenges, and opportunities that shape the market landscape. As industries increasingly adopt automation and IoT technologies, the demand for reliable networking solutions is on the rise. Din Rail Ethernet...

LV88 – Play Smart, Win Big is becoming a popular name in the online gaming and betting industry. Designed for players who want excitement, security, and rewarding opportunities, LV88 combines modern technology with a user-friendly experience to deliver smooth and enjoyable gameplay. A Complete Online Gaming Experience LV88 offers a wide range of gaming options to suit different types...

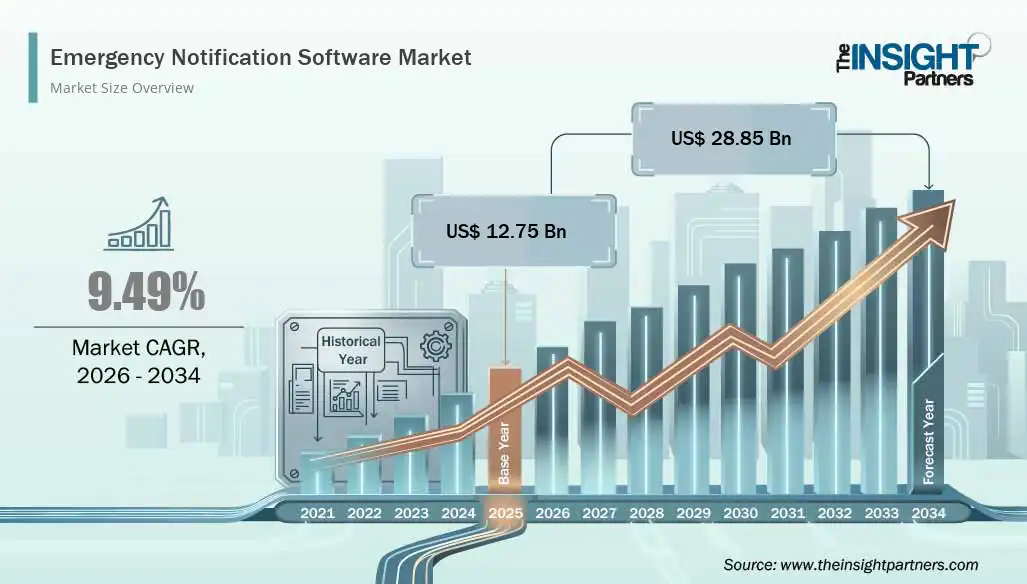

The United States Emergency Notification Software represents a significant share landscape, supported by widespread adoption of advanced communication technologies and increasing emphasis on emergency preparedness. According to The insight Partners, The Emergency Notification Software Market size is expected to reach US$ 28.85 Billion by 2034 from US$ 12.75 Billion in 2025. The...

Maintaining healthy blood sugar balance is an important part of overall metabolic wellness. Blood sugar naturally changes throughout the day based on food choices, physical activity, stress, sleep, and other lifestyle factors. For adults looking for additional daily support, natural supplements such as GlycoFree have become increasingly popular. In this GlycoFree review, we examine what...

"Regional Overview of Executive Summary Macular Degeneration Treatment Market by Size and Share The Global Macular Degeneration Treatment Market size was valued at USD 1.86 Billion in 2024 and is expected to reach USD 3.17 Billion by 2032, at a CAGR of 6.90 %during the forecast period Macular Degeneration Treatment Market analysis gives a clear idea on various...