A Thorough Examination of Conventional Mortgage Loan Requirements

The modern housing market operates on a foundation of risk assessment and capital allocation that can often seem opaque to the casual observer. When we dissect the underlying structures of home financing, the primary benchmark for most lenders remains the standard set of conventional mortgage loan requirements used to filter applicants. This analytical approach to lending is not merely about checking boxes; it is a sophisticated method of predicting future financial behavior based on historical data. By understanding the variables that lenders prioritize, prospective buyers can better position themselves within a competitive economic landscape where credit is both a tool and a gatekeeper.

Quantitative Measures of Risk

Lenders utilize a variety of data points to build a risk profile for every borrower. The most significant of these is the credit score, which serves as a proxy for financial character. In the conventional lending space, this metric is scrutinized more heavily than in government-sponsored programs. A higher score typically correlates with a lower probability of default, which in turn allows the lender to offer more favorable interest rates. This relationship between creditworthiness and cost of capital is the cornerstone of private mortgage lending, ensuring that the market remains liquid and that investors can accurately price the risk of the assets they are purchasing.

Beyond credit, the "capacity" to repay is evaluated through various ratios. An analyst must look at how much of a borrower's income is consumed by existing liabilities. When examining the broader market, it is interesting to note that the fha debt to income ratio is frequently adjusted by policymakers to stimulate homeownership among lower-income brackets, whereas conventional ratios remain more tethered to private market stability. The following table illustrates the typical mathematical boundaries used during financial analysis of an applicant:

|

Risk Variable |

Conventional Threshold |

Analytical Significance |

|

Loan-to-Value (LTV) |

80% (for best terms) |

Measures equity cushion against market dips |

|

Front-End Ratio |

28% - 31% |

Evaluates housing cost vs. gross income |

|

Back-End Ratio |

43% - 45% |

Assesses total debt burden on lifestyle |

Verifying Financial Integrity

Once the initial data is gathered, the file must undergo a period of rigorous verification. The mortgage underwriting process acts as the quality control mechanism for the entire banking industry. In this stage, an analyst or automated system confirms the existence and stability of the assets and income reported. This is not just about catching fraud; it is about ensuring the sustainability of the loan. If a borrower has significant assets but they are not "seasoned"—meaning they recently appeared in the account—the underwriter must determine if those funds are a liability in disguise or a legitimate gift.

Consider these critical points analyzed during this phase:

-

Verification of Employment (VOE): Ensuring the income stream is likely to continue for at least three years.

-

Appraisal Analysis: Determining if the market value of the collateral supports the loan amount.

-

Title Review: Confirming the property is free of liens that could jeopardize the bank's position.

-

Reserve Requirements: Analyzing if the borrower has enough liquid cash left over after closing to survive several months of unemployment.

Structural Contrasts in Lending Products

A comprehensive analysis of the mortgage industry requires a comparison of the different "engines" that drive home sales. For many, the decision-making process hinges on the difference between fha and conventional loan structures. From an analytical standpoint, the former is a social tool designed to provide accessibility, while the latter is a profit-driven product designed for efficiency and long-term stability. The choice between them has a profound impact on the borrower’s net worth over time, particularly when considering how insurance premiums are calculated and paid.

|

Feature |

Private (Conventional) Analysis |

Government (FHA) Analysis |

|

Risk Mitigation |

Private Mortgage Insurance (PMI) |

Mutual Mortgage Insurance (MMI) |

|

Cost Structure |

Risk-based pricing (higher score = lower cost) |

Flat-rate pricing (mostly independent of score) |

|

Equity Path |

Faster equity build-up through insurance removal |

Slower equity build-up due to permanent fees |

Synthesizing the Data for Success

The ultimate goal of this analysis is to provide a roadmap for financial readiness. By viewing the mortgage process as a series of data-driven hurdles, it becomes clear that preparation is the most significant variable under the borrower's control. Reducing revolving debt, stabilizing income sources, and improving credit scores are not just "good ideas"—they are strategic moves that alter the mathematical outcome of a loan application. When a borrower aligns their financial reality with the expectations of the market, the probability of a successful, low-cost closing increases exponentially.

In summary, while the path to a home can feel personal and emotional, it is governed by a cold, analytical framework. Understanding the mechanics of debt ratios, the scrutiny of the audit phase, and the structural differences in loan types allows a buyer to navigate the system with a level of sophistication that ensures long-term fiscal health. By mastering these variables, you move from being a mere applicant to becoming a smart investor in your own future.

Κατηγορίες

Διαβάζω περισσότερα

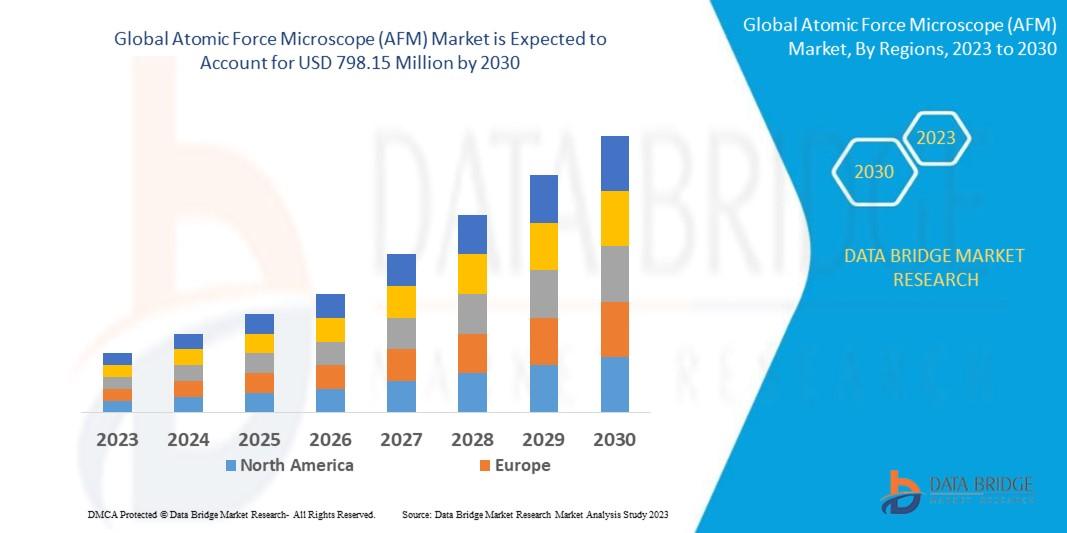

"Executive Summary Atomic Force Microscope (AFM) Market Size and Share Forecast Data Bridge Market Research analyses that the global atomic force microscope (AFM) market which was USD 504.60 million in 2022, is expected to reach USD 798.15 million by 2030, and is expected to undergo a CAGR of 5.9% during the forecast period of 2023 to 2030 The Atomic Force Microscope (AFM) report also...

The haunting world of 'All The Sinners Bleed' will soon pulse with a score from a master. Hans Zimmer and his collective, Bleeding Fingers Music, are set to provide the sonic landscape for the Netflix adaptation of S.A. Cosby's novel. ' This series delves into profound moral conflicts, and music has a powerful voice in such spaces," Zimmer remarked on the project's thematic depth. Showrunner...

x"In-Depth Study on Executive Summary Webcam Market Size and Share The global webcam market size was valued at USD 9.48 billion in 2024 and is expected to reach USD 20.48 billion by 2032, at a CAGR of 20.10% during the forecast period Webcam Market research report contains a key data about the market, emerging trends, product usage, motivating factors...

Good oral health is often associated with a bright smile and fresh breath, but its importance goes far beyond appearance. In reality, the condition of your teeth and gums is closely linked to your overall health. Numerous studies have shown that poor oral hygiene can contribute to serious health issues affecting the heart, diabetes management, respiratory system, and even mental well-being....

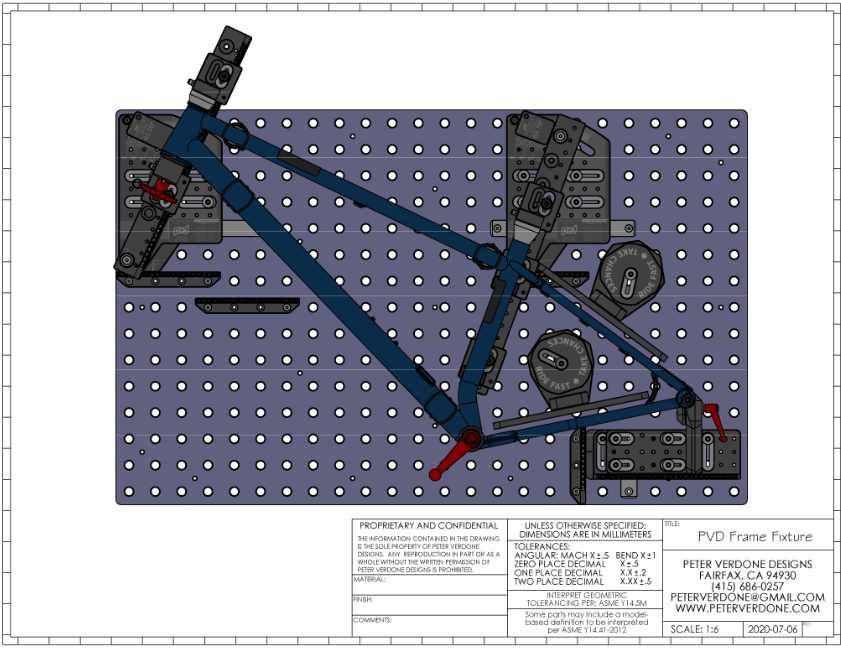

The manufacturing of modern sports equipment requires a high level of precision, repeatability, and quality control. From fitness machines and training systems to bicycle components and structural sports hardware, manufacturers must ensure that every part meets strict dimensional and performance requirements. Achieving this level of consistency depends heavily on well-designed manufacturing...