An Analytical Guide to Understanding Conventional Loan Options

Analyzing the modern real estate market requires a deep look at how debt functions as a tool for wealth creation. When we examine various types of conventional loans, we are looking at the primary engine behind private property acquisition in the United States. These financial instruments are not mere transactions; they are sophisticated contracts between individuals and private institutions. Unlike public programs that prioritize accessibility for higher-risk profiles, the private market rewards fiscal stability and high creditworthiness with lower long-term costs and greater flexibility in property selection. Understanding the underlying data of these mortgages allows a borrower to optimize their personal balance sheet for decades to come.

Evaluating the Risk and Reward of Private Lending

From a technical standpoint, the private mortgage market is divided into segments based on the size of the debt and the level of risk the lender assumes. Conforming mortgages are those that meet the specific acquisition criteria of the secondary market, which provides a level of liquidity and stability to the banking system. When we look at the data, borrowers who choose this path often benefit from more competitive pricing because their loans are standardized and easily traded. This efficiency in the market is what keeps interest rates relatively low for the average consumer with a solid financial background.

A critical point of analysis for any potential homeowner is what is the difference between a conventional loan and a fha loan in terms of equity accumulation and total interest paid. While a government-backed option might seem attractive due to lower entry barriers, the analytical view shows that the requirement for permanent mortgage insurance can significantly erode a homeowner's net worth over time. In contrast, private financing allows for the eventual removal of insurance premiums, which redirects that monthly cash flow back into the pocket of the owner. This makes the private route a superior choice for those who view their residence as an investment vehicle rather than just a place to live.

Comparative Analysis of Market Options

|

Metric |

Conforming Private |

Non-Conforming (Jumbo) |

Public/Government |

|

Typical Interest Rate |

Moderate to Low |

Slightly Higher |

Varies by Credit |

|

Insurance Structure |

Cancelable at 80% LTV |

Varies by Lender |

Often Life of Loan |

|

Underwriting Speed |

High Efficiency |

Comprehensive Review |

Moderate/Bureacratic |

Data-Driven Requirements for Borrowers

Lenders utilize specific mathematical formulas to determine the likelihood of a borrower defaulting on their obligations. One of the most heavily weighted metrics is the debt to income ratio fha or conventional lenders use to verify affordability. By analyzing the relationship between what you earn and what you owe, banks can predict financial stress before it happens. In the current economic climate, keeping this ratio lean is more important than ever. A lower ratio not only makes you more likely to get approved but also provides a safety net during periods of economic volatility where income might fluctuate but mortgage payments remain constant.

The liquidity required to enter the market is another area ripe for analysis. There is a persistent misconception that a massive capital outlay is the only way to secure a private mortgage. However, data indicates that the minimum down payment for conventional loan structures has shifted toward inclusivity to reflect the changing financial landscape of younger generations. Many qualified borrowers can secure a home with a three percent stake, allowing them to enter the market sooner and begin building equity. This strategy can be particularly effective in appreciating markets where the cost of waiting to save twenty percent far exceeds the cost of paying temporary private mortgage insurance.

Optimizing Your Financial Profile

-

Analyze your credit utilization to ensure it remains below thirty percent of available limits.

-

Compare the total interest cost of a fifteen-year term versus a thirty-year term to see the long-term ROI.

-

Monitor the local housing index to ensure the loan-to-value ratio is moving in a favorable direction.

-

Evaluate the opportunity cost of putting down a large sum versus investing that capital elsewhere.

Structural Variations in Interest and Terms

The choice between a fixed-rate and an adjustable-rate mortgage is essentially a bet on the future of the economy. A fixed-rate mortgage provides a locked-in cost of capital, which is a powerful hedge against inflation. Over time, as wages generally rise and the value of currency fluctuates, the real cost of a fixed mortgage payment actually decreases. This is a primary reason why long-term owners prefer the stability of a fixed term. It allows for precise long-term financial forecasting and protects the household from sudden spikes in market interest rates that could otherwise disrupt their standard of living.

Conversely, the adjustable-rate model can be analyzed as a short-term liquidity play. If the spread between the fixed rate and the initial adjustable rate is significant, a borrower could save thousands in the early years of the mortgage. This capital can then be deployed into other high-yield investments. However, this requires a disciplined exit strategy, such as selling the property or refinancing before the adjustment period begins. For the analytical borrower, the decision is based on the anticipated "hold time" of the asset and a calculated assessment of where interest rates might head in the medium term.

Closing Thoughts on Financial Strategy

In summary, the world of private lending offers a diverse set of tools for those who are willing to do the math. By understanding the benchmarks that lenders use and the long-term impact of various loan structures, you can move beyond the emotional aspects of home buying and make a purely rational financial decision. The goal is to minimize your cost of capital while maximizing the growth of your equity. Whether you are looking for the lowest possible entry point or the most aggressive path to full ownership, the private market has a solution that can be tailored to your data-driven goals.

As you move forward, continue to evaluate how your mortgage fits into your broader financial picture. A home is often a person's largest asset, but it is also their largest liability. Managing that liability with precision—by keeping an eye on your debt ratios and understanding the nuances of your loan agreement—is the hallmark of a savvy investor. Stay informed, remain flexible, and always look at the numbers behind the house. This analytical approach will ensure that your path to homeownership is not just a dream realized, but a sound financial victory.

Categorías

Read More

The continuous development of global electrical networks requires advanced equipment that can deliver stable performance, improved reliability, and efficient energy management. In modern power applications, the High Voltage Capacitor Unit integrates advanced material technology, optimized structural design, and precision manufacturing processes to support the evolving requirements of electrical...

https://www.boycat.co/blogs/149846/Expedia-booking-confirmed-but-ticket-not-issued-Dial-1-866

Nasal drug delivery systems have emerged as an important alternative to conventional methods of drug administration. By delivering medications through the nasal cavity, these systems enable rapid absorption through the nasal mucosa, often resulting in quicker therapeutic effects. The approach is gaining attention across healthcare settings because it offers a non-invasive option that can...

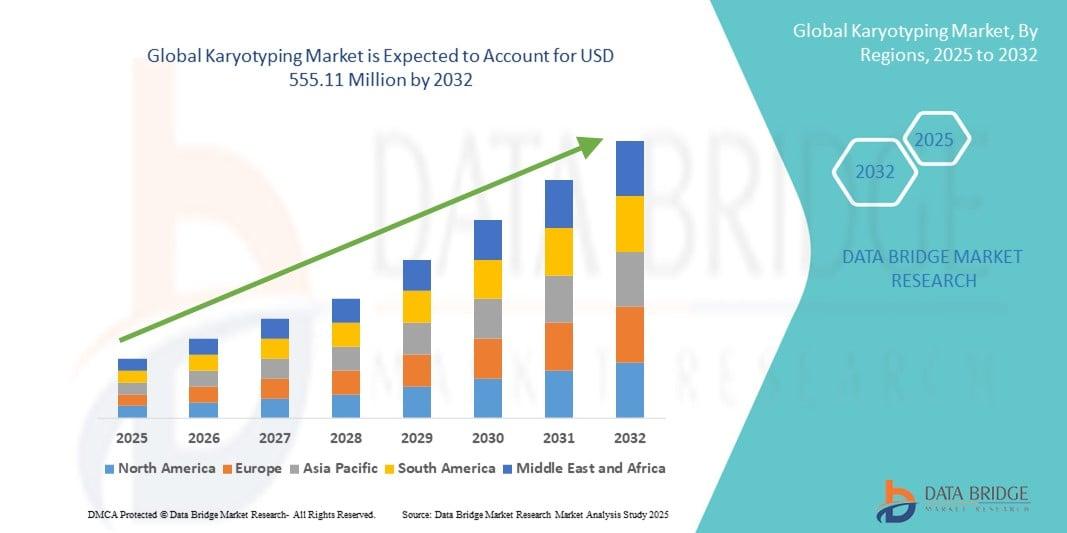

"Karyotyping Market Summary : According to the latest report published by Data Bridge Market Research, the Karyotyping Market The global karyotyping market size was valued at USD 350.92 million in 2024 and is expected to reach USD 555.11 million by 2032, at a CAGR of 5.9% during the forecast period The universal Karyotyping Market research report is a...

The Foliar Spray Market Size is gaining significant traction as modern agriculture shifts toward more efficient and sustainable crop nutrition methods. Foliar sprays—applied directly to plant leaves—enable faster nutrient absorption, improved crop health, and higher yields compared to traditional soil fertilization. With increasing global food demand and the need for...