Deciphering the Architecture of Qualifications for FHA Loan Approvals

The landscape of modern real estate often feels like a shifting maze, where the walls move just as you think you have found the exit. For many aspiring homeowners, the traditional banking system can feel cold and exclusionary, but there is a structural alternative designed to foster growth and stability. By examining the nuances of the qualifications for fha loan programs, we can see a deliberate effort by the government to lower the drawbridge for those who have been locked out of the castle. This is not just a loan; it is a specialized financial tool designed to balance risk with the human desire for a permanent place to call home.

The Socioeconomic Framework of Accessible Lending

At its core, the mortgage market functions on the assessment of risk versus reward. Traditional lending models often prioritize high-liquid assets and flawless fiscal histories, which can create a systemic barrier for middle-class families and younger generations. However, the federal government’s intervention provides a layer of insurance to private lenders, which fundamentally alters the analytical approach to borrower evaluation. This safety net allows for a more holistic view of an applicant’s life, focusing on the consistency of their income rather than the sheer volume of their savings account.

One must consider the long-term impact of property standards within this framework. Because the government is backing the debt, they require the asset to maintain a baseline level of structural integrity. This analytical requirement serves a dual purpose: it ensures the collateral remains valuable and it protects the buyer from predatory situations where they might purchase a home that is fundamentally unsafe. It is a protective measure that forces a level of quality control on the lower end of the housing market, ensuring that entry-level homes are still high-quality living spaces.

Strategic Re-evaluations of Home Equity

As market cycles progress and property values fluctuate, the role of a homeowner evolves from a resident to an investor. When a property appreciates significantly, it creates a pool of "dead" capital that can be revitalized through specific financial maneuvers. An analytical look at the fha cash out refinance guidelines reveals a system designed to help families leverage their home’s growth to solve other financial equations. Whether it is paying for higher education or eliminating high-interest consumer debt, this tool allows for the conversion of illiquid home equity into liquid capital, provided the borrower maintains a certain threshold of equity in the property.

Conversely, the market often presents opportunities for simple optimization without the need for additional capital. When examining the mechanics of how interest rates affect monthly overhead, one must ask what is a streamline in the context of portfolio management. This particular vehicle is an analytical masterpiece of efficiency, stripping away the redundant layers of traditional refinancing to allow for a rapid adjustment to current market conditions. It prioritizes the continuation of a successful payment history over a re-valuation of the borrower’s entire life, recognizing that a proven track record is often the best indicator of future performance.

The Mathematics of Credit and Debt

The most significant data point in any lending decision is the borrower's history of managing credit. While conventional logic suggests that a high score is the only way to secure a favorable rate, an analysis of the credit score needed for fha loan programs tells a different story. The system is calibrated to accept a wider range of scores, recognizing that life events—such as medical emergencies or temporary unemployment—can create statistical anomalies that do not necessarily reflect a person's character or current financial capability.

|

Metric |

Analytical Threshold |

Financial Implications |

|

Debt-to-Income (DTI) |

Standard 43% (up to 50%+) |

Determines the borrower's remaining monthly liquidity. |

|

Loan-to-Value (LTV) |

Up to 96.5% |

Reflects the government's high appetite for risk-sharing. |

|

Mortgage Insurance (MIP) |

Required for most terms |

The cost of the safety net that enables lower entry barriers. |

|

Cash Reserves |

Often zero required |

Increases accessibility for those without liquid wealth. |

Variables Influencing Loan Performance

-

The ratio of revolving debt to total available credit limits.

-

The duration of the borrower's longest-standing credit accounts.

-

The impact of recent inquiries on the overall credit profile.

-

The presence of "compensating factors" like significant savings or low debt.

-

The geographical stability of the borrower’s employment and residence.

An analytical approach to debt-to-income ratios reveals that lenders are looking for a "margin of safety." They calculate your total monthly obligations against your gross income to ensure that a slight increase in the cost of living won't result in a default. By keeping other debts low, a borrower effectively increases their purchasing power, allowing them to qualify for a more valuable asset within the same income bracket. It is a game of numbers where every dollar of existing debt has a magnified impact on your future borrowing capacity.

The Evolution of Modern Homeownership

The final stage of the lending process involves a detailed look at the closing statement. This document serves as the final ledger, accounting for every cent that passes between the buyer, the seller, and the lender. Analytically, the ability for a seller to contribute up to six percent of the purchase price toward the buyer’s closing costs is a massive lever. It allows for a transaction to occur with significantly less out-of-pocket capital from the buyer, essentially shifting the cost of entry onto the equity of the sale. This maneuver is a key reason why these programs remain the cornerstone of the entry-level housing market.

Looking forward, the health of the housing market depends on the continuous flow of new buyers into the system. These specialized loan programs provide the necessary lubrication for that engine. By analyzing the requirements and understanding the underlying philosophy of the program, prospective owners can position themselves to take full advantage of the opportunities presented. It is a complex system, certainly, but it is one that rewards those who take the time to understand its mechanics and align their financial behavior with its goals.

In conclusion, the path to owning a home is paved with data, documentation, and a bit of strategy. By moving beyond the surface-level definitions and looking at the structural benefits of government-backed lending, we see a path that is both logical and attainable. Success in this arena is not about having the most money; it is about having the best understanding of the rules and the patience to follow them to their logical conclusion: a set of keys and a deed in your name.

Catégories

Lire la suite

The pet care market is evolving rapidly as digital platforms and integrated service ecosystems transform how pet owners manage animal care. The market, valued at 289500.0 USD Billion in 2024, is projected to reach 551000.0 USD Billion by 2035, expanding at a CAGR of 6.1%. Rising technology adoption and increased pet ownership are key drivers supporting this structural transformation....

In today’s fast-paced, hyper-competitive marketplace, first impressions are everything—and nothing delivers a lasting impression quite like a premium business card. If you’re searching for business card printing Singapore that goes beyond ordinary and launches your brand into a league of its own, it’s time to act now. Landmark Print is redefining what it means to stand...

Trong thời đại giải trí số phát triển mạnh mẽ, các cổng game trực tuyến ngày càng trở nên phổ biến và thu hút đông đảo người chơi. NoHu là một trong những nền tảng nổi bật, được cộng đồng game thủ Việt Nam tin tưởng lựa chọn nhờ chất lượng dịch vụ vượt trội và hệ thống trò chơi hấp dẫn. Nổ...

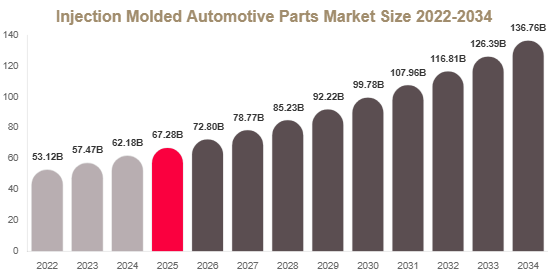

Injection Molded Automotive Parts Market Size, Growth, and Outlook Market Overview Market Size The global injection molded automotive parts market size is estimated at USD 67.4 billion in 2025, rising to USD 72.8 billion in 2026. By 2034, the market is projected to reach approximately USD 138.6 billion, growing at a CAGR of 8.2% during 2025–2034. The market is witnessing strong expansion...

オンラインカジノランキングは、数多く存在するオンラインカジノを「人気度」「安全性」「ボーナス内容」「ゲームの種類」などの観点から比較し、分かりやすく整理したものです。初心者から上級者まで、自分に合ったサイトを選ぶための重要な参考情報として広く利用されています。近年は比較サイトも増え、ユーザーはより効率的にサービスを選べるようになっています。情報収集の際には**オンラインカジノ ランキング**が参考にされることもあり、サイト選びの判断材料として役立ちます。 オンラインカジノは種類が非常に多いため、ランキングを活用することで自分に合ったサービスを効率よく見つけることができます。 ランキングの基本的な評価基準 オンラインカジノランキングでは、単なる人気だけではなく複数の要素を総合的に評価しています。 ボーナスとプロモーション...