The Step-by-Step Guide to Acquiring an FHA Loan Multifamily Property

The transition from a tenant to a property owner is a significant milestone, but jumping straight into the world of multiple units requires a precise plan. Many people find that an fha loan multifamily purchase is the logical first step because it combines a home with an investment. However, you cannot simply wing a deal involving hundreds of thousands of dollars. Success requires following a chronological sequence of events to ensure you don't miss critical deadlines or financial requirements.

Step 1: Financial Stabilization and Pre-Approval

Your journey begins long before you look at a listing. You must first ensure your debt-to-income ratio is within the acceptable 43 to 50 percent range. This involves calculating your monthly debt obligations against your gross income. Once your finances are in order, you need a pre-approval letter from a lender who specifically understands the nuances of multi-unit financing. Without this letter, most sellers of duplexes or triplexes won't even let you through the front door for a tour.

During this initial phase, it is common to encounter properties that are priced low because they need work. You should investigate what is a rehab loan during your pre-approval process to see if you qualify for the additional borrowing power. Being approved for both the purchase price and a renovation budget allows you to act quickly when you find a distressed quadplex that other buyers are too afraid to touch because they lack the ready cash for repairs.

The Document Checklist for Your Lender

Lenders will require a mountain of paperwork to verify your eligibility. Having these ready in a digital folder will shave weeks off your closing time. Use the following table to track your progress as you gather your materials.

|

Document Type |

Quantity Needed |

Why It Is Critical |

|

Tax Returns |

Last 2 Years |

Proves consistent income history. |

|

Pay Stubs |

Last 30-60 Days |

Verifies current employment status. |

|

Bank Statements |

Last 2-3 Months |

Shows the source of your down payment funds. |

|

Identification |

Driver’s License/Passport |

Standard KYC (Know Your Customer) requirement. |

Step 2: Selecting the Right Type of Financing

Once you are pre-approved, you need to decide which of the various types of fha loans fits the specific property you are targeting. This decision is usually made after you find a property and have a general idea of its condition. If the building is in pristine shape, you go with the standard path. If the building has "good bones" but needs a new roof or HVAC systems, you pivot to the renovation path. Matching the loan to the property’s needs is the difference between a smooth closing and a rejected application.

-

Identify the Property Grade: Determine if the building is "Turnkey," "Cosmetic Fixer," or "Full Gut."

-

Consult Your Contractor: If choosing a 203(k), get a licensed professional to give you a formal estimate early.

-

Check Loan Limits: Ensure the total price plus repairs stays under the local county limit for that specific unit count.

-

Verify Zoning: Confirm with the city that the property is legally registered as a multifamily dwelling.

Step 3: Navigating the Inspection and Appraisal

This is the most technical part of the process. Unlike a standard home loan, a multifamily appraisal includes a "Comparable Rent Schedule." The appraiser isn't just looking at what the house is worth; they are looking at what the other units can earn. For properties with three or four units, this is where the Self-Sufficiency Test happens. You must be prepared for the possibility that the appraiser's rent estimate is lower than the seller's claims, which could affect your loan amount.

If the inspection reveals safety issues—like missing handrails or peeling lead paint—these must be fixed before the loan can close. This is why many buyers prefer the 203(k) route; it allows those repairs to happen after the sale using the loan proceeds rather than forcing the seller to pay for them out of pocket. Understanding this tactical shift allows you to negotiate more effectively with sellers who are tired of dealing with their old building.

Managing the Closing Process

As you approach the finish line, you will receive a Closing Disclosure. This document outlines every penny you need to bring to the table. This is the time to double-check that your interest rate and insurance premiums are correct. Once you sign the final papers and receive the keys, your role officially shifts from "Buyer" to "Landlord." You should have your tenant screening process and lease agreements ready to go the moment you take ownership.

-

Set Up Utilities: Ensure all common area meters are in your name.

-

Notify Current Tenants: Introduce yourself as the new owner and provide clear instructions on how to pay rent.

-

Change the Locks: For security, always re-key every unit and common entrance immediately.

-

Final Walkthrough: Ensure no new damage occurred between the inspection and the closing date.

Step 4: Future Optimization and Refinancing

The work doesn't stop once you move in. After you have established a history of on-time payments and perhaps improved the property’s value, you should look for ways to decrease your monthly expenses. The most efficient way to do this is through a streamline fha loan. This step usually occurs 6 to 12 months after the initial purchase if interest rates have moved in your favor. By lowering your rate, you increase the "spread" between your mortgage payment and the rent you collect.

This tactical maneuver is often the "secret sauce" of successful house hackers. By reducing the largest fixed cost—the mortgage interest—you effectively increase your personal income without having to work more hours. It also makes the property more resilient to market downturns because your "break-even" point is lower. Always keep a close eye on the market and stay in touch with your loan officer to time this move perfectly.

Building Your Long-Term Management System

To keep the property running like a clock, you need a system for maintenance and tenant relations. Being a "step-by-step" person means having a protocol for everything. Create a digital folder for each unit to store leases, repair receipts, and communication logs. This level of organization makes it much easier to file your taxes at the end of the year and provides a clear "paper trail" should you ever decide to sell the property or use it as collateral for a second investment.

Every successful real estate empire was built one unit at a time. By following this structured path, you minimize the "rookie mistakes" that plague most new investors. You are not just buying a building; you are implementing a business plan. Stay diligent, stay organized, and keep your focus on the long-term equity growth that comes from owning a well-managed multifamily asset.

Conclusion: The Strategic Exit

While this guide focuses on the "how-to" of getting started, always keep your end goal in mind. Whether you plan to live there for one year or ten, the fha loan multifamily strategy is your launchpad. By mastering these steps, you have gained a skill set that will serve you for the rest of your life. Real estate is a journey of constant learning, and your first multifamily deal is the most important lesson you will ever take. Follow the process, trust the data, and enjoy the rewards of your hard work.

Catégories

Lire la suite

The Tuna Market continues to expand rapidly as consumer demand for high-protein, convenient, and affordable seafood products accelerates worldwide. Tuna remains one of the most consumed fish species across Europe, North America, and Asia-Pacific, supported by its versatility in culinary use, strong presence in packaged food categories, and rising adoption across the foodservice...

The most popular AviaGames titles include Solitaire Clash, Bingo Tour, Bingo Clash, and 8 Ball Strike. These games stand out for combining familiar formats with structured competition, especially within the space of skill-based real money games. If you’ve explored mobile games recently, you’ve probably come across at least one of them. Each...

In today’s fast-paced digital world, computer knowledge is no longer optional—it is essential. Whether you are a student, job seeker, entrepreneur, or working professional, having strong computer skills can significantly improve your career opportunities. Businesses across industries rely on technology for daily operations, communication, and data management. Because of this,...

Rencontrez-vous des difficultés avec Valorant ? Savoir comment contacter le support de Valorant est essentiel pour garantir une expérience de jeu fluide et agréable. Que ce soit pour des problèmes de connexion, des bugs ou des questions relatives à votre compte, Riot Games offre plusieurs options pour obtenir de l’aide. Pour commencer, consultez la...

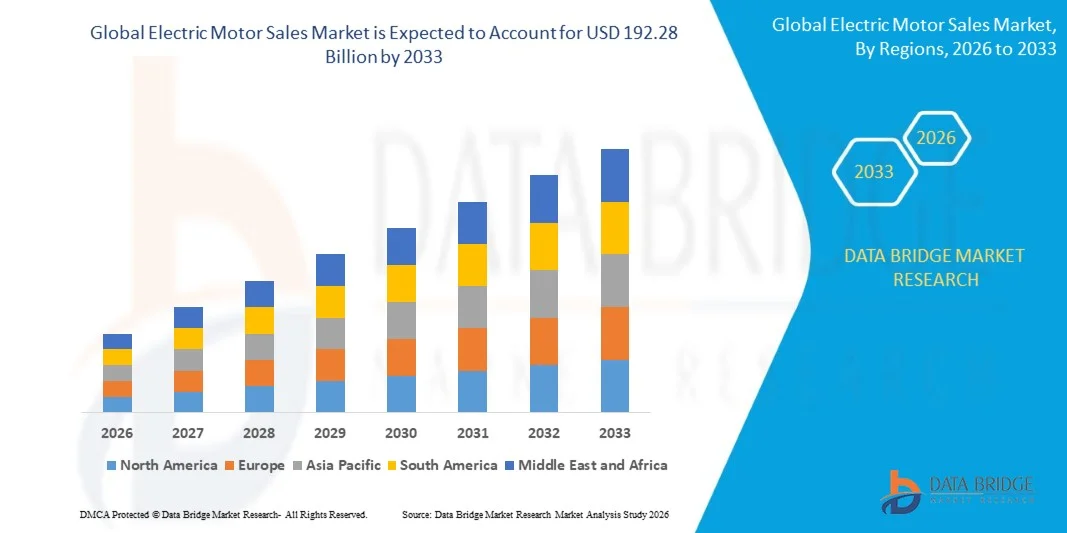

"Latest Insights on Executive Summary Electric Motor Sales Market Share and Size The global electric motor sales market size was valued at USD 118.83 billion in 2025 and is expected to reach USD 192.28 billion by 2033, at a CAGR of 6.20% during the forecast period The study and analysis conducted in this industry report also helps to figure out types of...