Expert Advice on Obtaining a COE for VA Loan and Saving Money

Buying a home while balancing military life or transitioning to a civilian career is a high-stakes mission. One of the most effective strategies you can employ is getting your paperwork organized before you even look at a listing. Specifically, securing a coe for va loan early in the process gives you the leverage needed to negotiate with confidence. This document is the only way a lender can verify that you have the federal backing required for a zero-down mortgage, making it the bedrock of your entire home-buying strategy.

Waiting until you are under contract to find this form is a common mistake that can lead to unnecessary stress and delays. By being proactive, you position yourself as a serious buyer in a market where timing is everything. Beyond the paperwork, there are several nuances to the program that can save you thousands of dollars if you know how to navigate them correctly. Here is a breakdown of the best tips to streamline your experience.

Mastering the Eligibility Maze

Success starts with knowing exactly where you stand with the Department of Veterans Affairs. It is a smart move to review the specific criteria for va home loan eligibility based on your era of service. While most modern service members need 90 days of active duty, those who served in earlier decades or within the National Guard might have different benchmarks to hit. The following table helps clarify these time-based requirements.

|

Service Type |

Active Duty Requirement |

Alternative Requirement |

|

Gulf War to Present |

24 continuous months |

90 total days (active) |

|

National Guard |

90 days (30 consecutive) |

6 creditable years |

|

Reserve Members |

90 days (Title 10) |

6 creditable years |

A great tip for Guard and Reserve members is to ensure your "Points Statement" is up to date alongside your discharge papers. Lenders often need this extra layer of proof to verify your service years if you were never activated for long-term federal missions. Keeping these documents in a digital folder makes the application phase nearly effortless.

Financial Strategies for the Closing Table

Many veterans are surprised by the final numbers because they focus entirely on the zero-down payment benefit. To stay ahead, you should ask your lender early on: how much is closing cost on a va loan? On average, you can expect these costs to range between 3 percent and 5 percent of the total loan amount. However, you have a secret weapon: seller concessions.

-

Tip: Request the seller to pay your closing costs. The VA allows sellers to contribute toward these expenses, which can keep your out-of-pocket costs at zero.

-

Tip: Check your disability status. If you have a service-connected disability rating of 10 percent or higher, you are exempt from the VA Funding Fee, saving you thousands.

-

Tip: Watch out for non-allowable fees. The VA protects you from paying "junk fees" like attorney fees charged by the lender or document preparation fees.

-

Tip: Compare lenders. Not all VA lenders offer the same interest rates or credit overlays, so shopping around can result in a better monthly payment.

By implementing these financial tactics, you ensure that the mortgage works for your budget rather than against it. It is about more than just getting the loan; it is about getting the best possible terms for your family's future.

Maximizing Your Buying Power

In high-cost areas, you might worry that a standard loan won't be enough to secure a property. However, the modern maximum va loan amount is no longer capped by the government for those with full entitlement. This is a massive advantage in 2026, as conforming loan limits have risen to $832,750 in many counties and over $1.2 million in high-cost regions. Even then, the VA does not strictly limit your borrowing—only the amount they will guarantee to the lender.

The real tip here is to focus on your residual income. The VA uses a unique calculation to ensure you have enough money left over after paying your mortgage and debts to cover daily life like food and gas. If your residual income is strong, lenders are much more likely to approve higher loan amounts, even if your debt-to-income ratio is a bit higher than traditional standards. This focus on "real-world" affordability is what makes this benefit so resilient and valuable for the military community.

Final Checklist for Success

To keep your home-buying mission on track, follow this simple routine:

-

Download your documents from the VA portal at the start of your search.

-

Get a pre-approval letter from a lender who understands military income like BAH and BAS.

-

Work with a real estate agent who has the "Military Relocation Professional" (MRP) certification.

-

Always get a home inspection, even though the VA appraisal covers safety and habitability.

Using these tips will help you avoid the typical hurdles and move into your new home with the peace of mind you deserve. Your service earned you this benefit; using it wisely is the best way to honor that dedication.

Categorie

Leggi tutto

Wearable EEG devices have significantly transformed neurological monitoring by offering portable, non-invasive solutions for tracking brain activity in real time. These devices integrate electroencephalography sensors into compact and lightweight headsets, enabling continuous monitoring across clinical and non-clinical settings. Their applications span healthcare, neuroscience research, gaming,...

People talk about digital growth like one tactic does everything, but that is rarely how it works. Usually several signals push together. Content matters, authority matters, and brand mentions matter too. That is part of why media releases still have value when used well. Some people act releases stopped mattering, though that feels exaggerated. Used properly, they can still support...

Historically, Japan has dominated Asia’s video game scene, producing numerous globally acclaimed titles for decades. These flagship titles have shaped the industry’s reputation, leaving other nations in their shadow. However, recent years have marked a shift, as countries like South Korea and China have begun to make significant strides beyond their traditional markets. While...

A fictional president finds his place among historical leaders The Smithsonian's National Portrait Gallery now displays an image of power from popular culture Artist Jonathan Yeo captures Kevin Spacey's transformative performance as Frank Underwood This portrait blurs the lines between actor, character, and the presidency itself The unveiling ceremony mirrored a real presidential event Spacey...

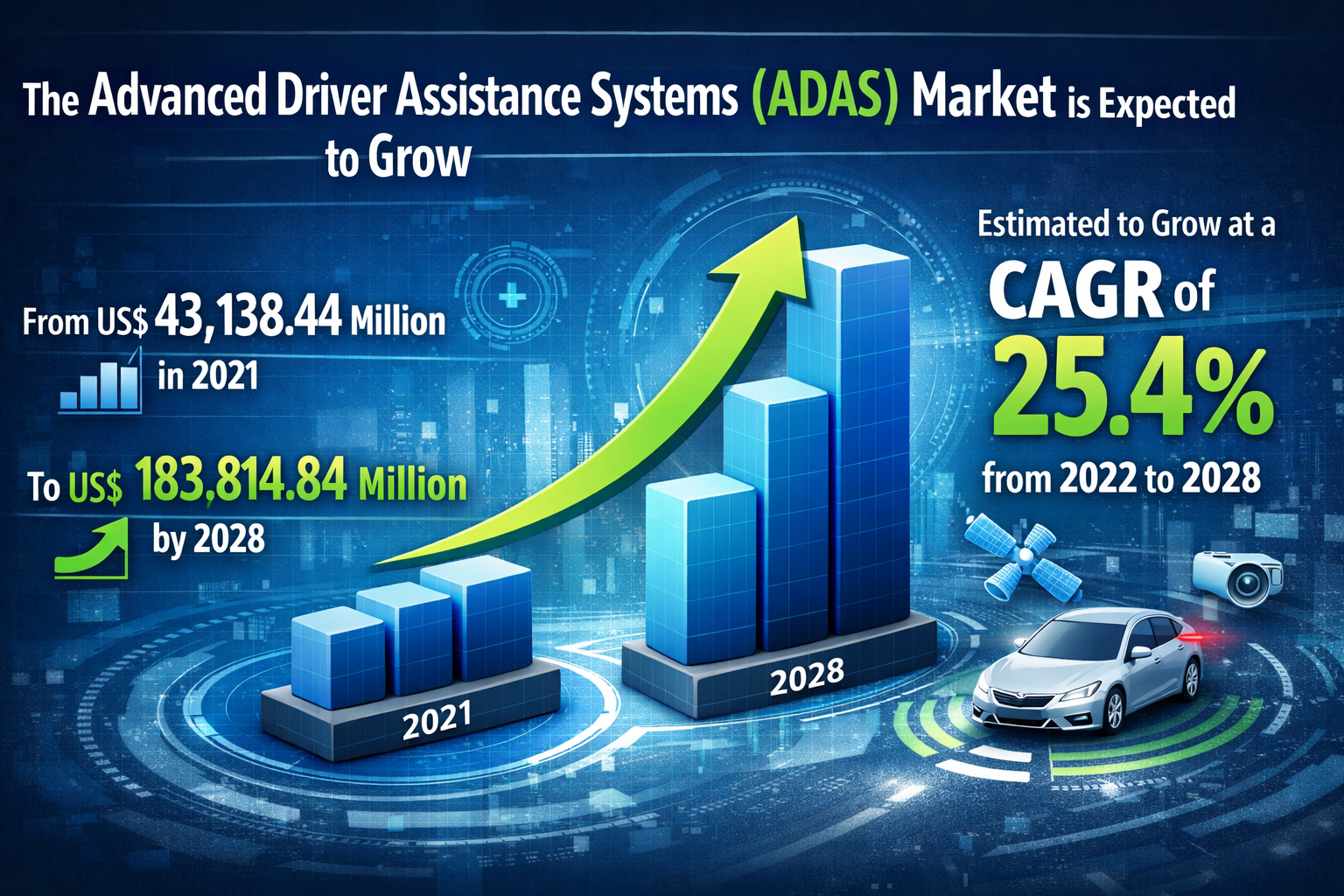

Advanced Driver Assistance Systems (ADAS) are electronic technologies in vehicles that help drivers drive more safely and comfortably. They use sensors, cameras, radar, and software to monitor the surroundings and assist in tasks like braking, steering, and parking. ADAS features include lane departure warning, adaptive cruise control, and automatic emergency braking. These systems reduce...