ROI Benchmark Framework™: Measuring Technology Value with Precision

What are digital banking platforms?

How many of you can remember when you visited your bank physically? We now do most of our banking activities on our mobile devices or PCs. What we are doing is described as Digital Banking, where traditional banking services are digitized. Note that it is digital banking and not mobile banking. Because Mobile Banking is just one type of digital banking. The types of digital banking are:

1. Online banking: This is your traditional banking that swaps the physical location for the bank’s website. It allows the users to perform traditional banking activities like checking balance, transferring funds, and paying bills.

2. Mobile banking: This is the ubiquitous type that allows users to perform banking activities through smartphone apps.

3. Neobanks: These are digital-first banking platforms with little or no branch presence. Some well-known neo banks include Chime, Revolut, Monzo, and N26.

4. Challenger banks: These are digital banks that directly compete with traditional banks using newer technology, digital-first service, and lighter branch networks.

Or ATM

5. UPI-based real-time payments: These are instant bank-to-bank payments through apps using UPI IDs, QR codes, or linked bank accounts. This type of digital banking is especially central in India.

What about ROI Benchmark Framework™?

Buying software is an investment. It is but natural that the buyers want to know about the Return On Investment (ROI). Digital banking software ROI is usually expected in four areas: lower operating costs, better customer acquisition and conversion, higher revenue from deeper digital engagement, and faster internal processes like onboarding and servicing. So instead of looking for one fixed ROI percentage, banks usually ask whether the software can reduce cost-to-serve, improve digital sales, speed up operations, and strengthen customer retention enough to justify the investment. Vendors should help clients achieve optimum ROI by making digital banking software easier to integrate, easier to adopt, easier to govern, and easier to connect to hard business outcomes.

If the vendors are using ROI as a part of their sales pitch, the model, or framework, must be grounded in the client’s real business conditions, not generic promises. It should start with a clear baseline: current onboarding time, servicing costs, digital adoption, conversion rates, branch dependency, and call-center volumes. It must also include the full cost of ownership, covering software, implementation, integration, migration, training, testing, and support. On the benefit side, the calculator should quantify outcomes that matter to banks, such as faster onboarding, lower servicing costs, better activation, stronger cross-sell, and higher digital sales. A strong model should present proper financial outputs like ROI, NPV, payback period, and multi-year cash flow, ideally over three to five years. It should also use risk-adjusted assumptions, scenario analysis, and full formula transparency. Otherwise, the calculator is just a sales aid, not a credible decision-making tool. It should let buyers challenge assumptions and tailor inputs to reality.

Catégories

Lire la suite

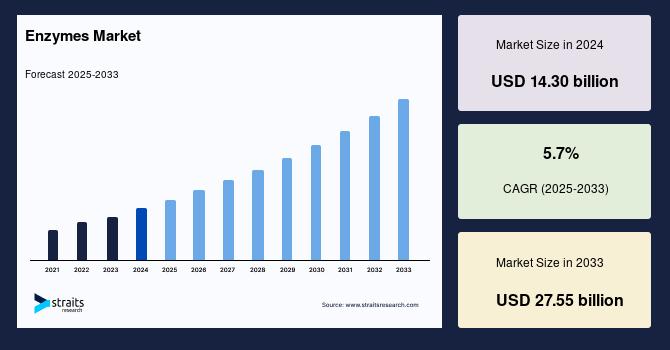

Enzymes Industry Insights: Straits Research recently introduced the latest update on the Enzymes Market that provides an extensive outlook of the market, analyzing key growth opportunities, challenges, risk factors, and emerging trends across diverse geographic regions. The report offers a definitive and meticulous analysis of the Enzymes industry size, share, demand, key growth...

Career success is influenced by many factors, but one often-overlooked element is visual presentation. In today's digital-first world, people frequently encounter your photograph before they ever meet you in person. Investing in professional headshots helps create an immediate sense of trust and professionalism while enhancing your overall personal brand. Whether you're applying for new...

Hoodies That Turn Minimalism into Art. Stussy Milano Hoodie In a world dominated by bold prints, loud logos, and over-the-top designs, minimalism has emerged as a breath of fresh air in fashion. When it comes to hoodies, this understated approach to design turns simple garments into art. Minimalist hoodies focus on clean lines, subtle details, and a less-is-more philosophy, allowing the...

Strong Growth Outlook for Copper Scrap Market Driven by Recycling and Industrial Demand The Copper Scrap Market is experiencing remarkable growth as industries worldwide increasingly turn to recycled materials to meet sustainability goals. The Copper Scrap Market size was valued at USD 63.52 Billion in 2024 and is projected to reach USD 124.88 Billion by 2032, growing at a CAGR of...

" According to the latest report published by Data Bridge Market Research, the E-Discovery Market The global e-discovery market size was valued at USD 16.87 billion in 2024 and is expected to reach USD 39.53 billion by 2032, at a CAGR of 11.23% during the forecast period. This E-Discovery Market research report is a resource, which offers current as well as upcoming technical...