VA Interest Rate Reduction Refinance Loan Hacks for Maximum Savings

Locking in a lower mortgage payment is a top priority for any homeowner, but military families have a unique advantage that often goes overlooked. Utilizing a va interest rate reduction refinance loan can slash monthly housing costs without the typical hurdles of a standard refinance. Since this program is designed specifically for those with existing VA mortgages, the red tape is minimal, allowing you to focus on the numbers rather than the paperwork. To get the most out of this benefit, you need to look beyond the advertised rates and understand the moving parts that determine your actual savings.

Timing Your Move with Precision

One of the most effective strategies is to monitor the market for at least 30 days before pulling the trigger. Rates fluctuate daily, and even a 0.25 percent difference can save you thousands over the life of the loan. However, avoid the trap of waiting for the absolute bottom; if the numbers make sense today and offer a clear net tangible benefit, it is often better to secure the win. Many lenders allow you to lock in a rate for 60 days, giving you a safety net while the administrative work moves forward.

The Truth About Upfront Charges

A common question among veterans is what is a va funding fee and how it impacts the overall value of the refinance. For an IRRRL, this fee is a flat 0.5 percent of the loan amount, which is significantly lower than the fees for initial home purchases. A pro tip for those with a service-connected disability: you may be entirely exempt from this charge. Always verify your status on your Certificate of Eligibility (COE) before signing the final documents to ensure you aren't paying a fee you don't actually owe.

Navigating Geographic Loan Standards

While the VA does not technically set a hard limit on how much you can borrow if you have full entitlement, your lender might still reference va loan limits by county to determine their own risk levels. In 2026, the national baseline for many areas has risen to $832,750, with high-cost regions like San Francisco or parts of Hawaii reaching well over $1.2 million. If your loan amount is particularly high, shopping for a lender that specializes in VA jumbo loans can help you find more competitive terms and fewer internal restrictions.

Managing Out of Pocket Expenses

Many advertisements claim no-cost refinancing, but it is important to look at the fine print. The closing cost for va loans usually totals between 2 percent and 5 percent of the loan amount. To keep cash in your pocket, you can choose to roll these costs into the principal of the loan. While this increases your total debt slightly, it removes the need for a large upfront payment at the closing table. Just be sure to calculate your break-even point—the month where your total savings finally exceed the costs you rolled into the mortgage.

Avoid Common Refinancing Pitfalls

A major tip for a smooth transition is to avoid taking on new debt, like a car loan or large credit card balance, right before or during the refinance process. Even though the IRRRL has relaxed credit requirements, lenders still perform a "soft pull" to ensure your financial situation hasn't drastically changed. Keeping your credit profile stable ensures that the rate you were quoted on day one is the same rate you get on closing day. By staying proactive and informed, you turn a government benefit into a powerful engine for your family's financial freedom.

Catégories

Lire la suite

Chanel is one of the most iconic luxury brands in the world, known for its timeless elegance and exceptional craftsmanship. From the Classic Flap to the Boy Bag, Chanel handbags are not only fashion statements but also valuable assets in the luxury resale market. Today, chanel回收 recycling (resale/buyback) is becoming increasingly popular as more people recognise the strong value retention of...

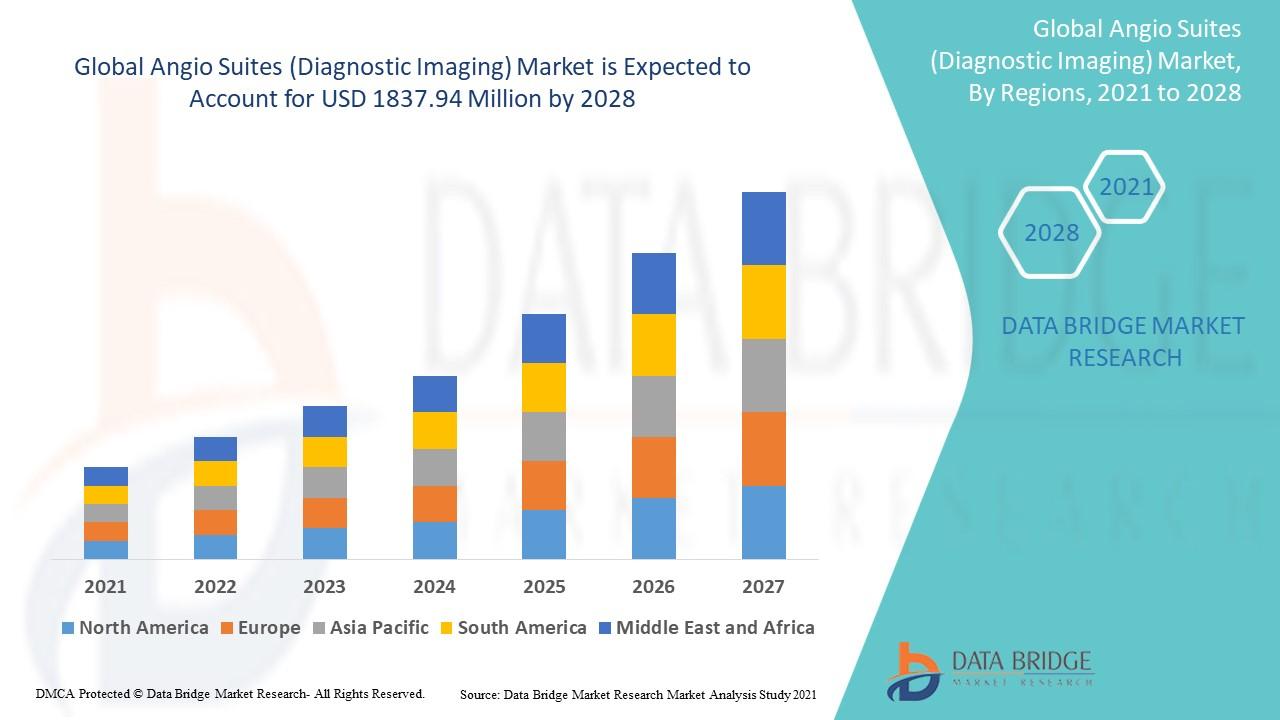

"Executive Summary Angio Suites (Diagnostic Imaging) Market: Share, Size & Strategic Insights CAGR Value Data Bridge Market Research analyses the market to account to USD 1837.94 million by 2028 and will grow at a CAGR of 6.75% in the above mentioned forecast period. The Angio Suites (Diagnostic Imaging) report makes available a thoughtful overview of product specification,...

"Adipic Acid Market Summary: According to the latest report published by Data Bridge Market Research, the Adipic Acid Market CAGR Value Global adipic acid market size was valued at USD 6.41 billion in 2024 and is projected to reach USD 9.40 billion by 2032, with a CAGR of 5.5% during the forecast period of 2025 to 2032. An influential Adipic Acid Market report contains a...

In today’s fast-paced world, many people struggle with poor focus, mental fatigue, and memory challenges. Long work hours, constant screen exposure, and daily stress can make it difficult for the brain to perform at its best. Because of this, many individuals are searching for natural ways to support cognitive health and mental clarity. One innovative approach gaining attention is The...

In the relentless race for innovation, the difference between market domination and missed opportunity often comes down to one critical step: knowing exactly what already exists. If you’re not leveraging a chemical structure search patent, you’re not just behind—you’re invisible. In today’s hyper-competitive landscape, every second counts, and every overlooked...