What is the Role of TPA in Health Insurance? A Complete Guide

When you buy or renew bike insurance online, one term you'll encounter repeatedly is IDV. Most riders either ignore it or simply accept the default value suggested by the insurer — and that's a costly mistake.

Understanding IDV in bike insurance can be the difference between receiving fair compensation after a total loss and walking away significantly short-changed. Whether you're a first-time buyer or a seasoned rider comparing the best two wheeler insurance plans, this guide will give you a complete, clear understanding of IDV — what it means, how it's calculated, and why it matters more than you think.

What is IDV in Bike Insurance?

IDV stands for Insured Declared Value. In the context of bike insurance, IDV is the maximum amount your insurance company will pay you if your two-wheeler is stolen or damaged beyond repair (total loss).

Think of IDV as the current market value of your bike — not the price you paid for it when it was new, but the price it would fetch today, accounting for depreciation due to age and usage.

In even simpler terms: IDV is the sum insured for your bike.

If your motorcycle is completely destroyed in an accident or stolen and never recovered, your insurer will pay you the IDV — not a rupee more. This is why setting the right IDV when buying bike insurance online is one of the most important decisions you'll make as a policyholder.

What Does IDV Mean in Bike Insurance — A Practical Example

Let's say you purchased a bike for ₹1,20,000 two years ago. Due to depreciation, its current market value is approximately ₹85,000. If you declare an IDV of ₹85,000 and your bike is stolen, your insurer will compensate you with ₹85,000 — helping you buy a comparable replacement vehicle.

If, however, you had declared a lower IDV of ₹60,000 (to save on premium), you'd receive only ₹60,000 — leaving a ₹25,000 shortfall out of your own pocket.

This is the core reason IDV means in bike insurance far more than just a number on your policy document — it is your financial safety net.

How is IDV Calculated in Bike Insurance?

The IDV in bike insurance is calculated using a standard depreciation formula mandated by the Insurance Regulatory and Development Authority of India (IRDAI). The formula is:

IDV = (Manufacturer's Listed Selling Price) – (Depreciation as per IRDAI Schedule)

IRDAI Depreciation Schedule for Bikes

|

Age of the Vehicle |

Depreciation Rate |

|

Less than 6 months |

5% |

|

6 months to 1 year |

15% |

|

1 year to 2 years |

20% |

|

2 years to 3 years |

30% |

|

3 years to 4 years |

40% |

|

4 years to 5 years |

50% |

For bikes older than 5 years, the IDV is determined by mutual agreement between the insurer and the policyholder, based on the condition of the vehicle.

Note: IDV is calculated on the ex-showroom price of the bike, not the on-road price. Accessories like registration, insurance, and road tax are not included in the base IDV calculation. However, additional accessories fitted to the bike can be covered separately.

IDV and Your Bike Insurance Premium — The Direct Connection

There's a straightforward relationship between IDV and your bike insurance online premium:

-

Higher IDV = Higher Premium

-

Lower IDV = Lower Premium

This creates a temptation for many policyholders to declare a lower IDV to reduce their annual premium cost. While this saves a small amount upfront, it exposes you to a significant financial loss in the event of theft or total loss of your vehicle.

Conversely, some policyholders try to declare an inflated IDV to receive more compensation. Insurers do not allow this — IDV cannot exceed the current market value of the bike, and an unrealistically high IDV claim will be rejected during settlement.

The sweet spot is an accurate IDV — one that reflects the true current market value of your bike.

Why IDV Matters More Than You Think

1. It Determines Your Theft Compensation

If your bike is stolen and not recovered within 90 days, your insurer settles the claim at the IDV. A correctly set IDV ensures you can afford a comparable replacement without dipping into your savings.

2. It Defines Total Loss Payouts

If repair costs exceed 75% of your bike's IDV, the claim is treated as a total loss or constructive total loss. In this case, your insurer pays the full IDV. An undervalued IDV means a smaller payout — even for severe accident damage.

3. It Affects the Value of Your Policy

The best two wheeler insurance policy isn't just the cheapest one — it's the one that offers meaningful financial protection. A policy with an accurate IDV provides real value; an undervalued one offers false security.

4. It Impacts Annual Renewals

When you renew bike insurance online, the IDV is recalculated based on the bike's current age and depreciation. Reviewing and confirming the IDV at every renewal is critical — never auto-renew without checking this figure.

IDV for Bikes Older Than 5 Years

Once your bike crosses the 5-year mark, IRDAI depreciation tables no longer apply. The IDV for older bikes is determined by mutual agreement between you and the insurer, typically based on:

-

The physical condition of the vehicle

Autos & Vehicles -

Service and maintenance history

-

Market resale value of that make and model

-

Any recent repairs or upgrades

For vintage or collector bikes, the agreed IDV can sometimes be higher than standard depreciation would suggest. Always get multiple quotes when renewing bike insurance online for older vehicles to ensure a fair IDV is being offered.

Can You Negotiate IDV in Bike Insurance?

Yes — within limits. IRDAI allows a flexibility band of ±10–15% on the calculated IDV when purchasing or renewing bike insurance. This means:

-

You can increase the IDV by up to ~10–15% for better protection (at a slightly higher premium).

-

You can decrease the IDV by up to ~10–15% for a lower premium (at the risk of underinsurance).

For most riders, the wisest approach is to keep the IDV as close to the actual market value of the bike as possible — ideally at the upper end of the permissible range. This is especially important if your bike is relatively new or in excellent condition.

When comparing the best two wheeler insurance plans online, use IDV as a primary comparison metric — not just the premium amount.

IDV vs Market Value vs Invoice Value — Key Differences

|

Term |

Definition |

Used For |

|

Invoice Value |

Original purchase price (on-road) |

Covered under Zero Depreciation add-on |

|

IDV (Insured Declared Value) |

Current market value after depreciation |

Theft & total loss claims |

|

Market Value |

Actual resale value of the bike today |

Basis for IDV calculation |

Understanding these distinctions helps you make smarter decisions when customising your bike insurance online policy with add-ons like zero depreciation cover, return to invoice cover, and engine protection.

IDV and Zero Depreciation Cover — How They Work Together

Zero Depreciation (also called Nil Depreciation or Bumper-to-Bumper cover) is a popular add-on for bike insurance online that eliminates depreciation deductions on parts during partial loss claims (repairs). However, it does NOT affect the IDV.

Even with zero depreciation cover, your theft or total loss payout is still based on the IDV. This is why:

-

Zero depreciation protects you on repair claims

-

Correct IDV protects you on theft and total loss claims

Both work together to give you the most comprehensive protection — which is why the best two wheeler insurance plans often bundle both features.

How to Check and Set the Right IDV When Buying Bike Insurance Online

Follow these steps when purchasing or renewing your policy:

-

Check current market value — Look up your bike's resale price on platforms like OLX, BikeWale, or dealer quotes to understand its current market value.

-

Compare IDV across insurers — When buying bike insurance online, compare not just premiums but also the IDV offered by each insurer for the same bike.

-

Don't default to the lowest IDV — The cheapest premium option often comes with an undervalued IDV. Evaluate the trade-off carefully.

Bicycles & Accessories -

Review IDV at every renewal — Depreciation changes every year. Confirm the updated IDV reflects your bike's actual current value.

-

Declare additional accessories — If you've added custom accessories (alloy wheels, GPS, crash guards), declare them separately to ensure they're covered and factored into your compensation.

Catégories

Lire la suite

A Complete Query Guide: Choosing the Right Base and Mattress in NZ Are you searching for the perfect Base and Mattress for your bedroom? Wondering what makes a quality Bed Base With Mattress deal worth it? Or trying to decide which queen bed base NZ option suits your space best? This guide answers all your common questions...

OverviewIncorporation is just one step to running a private limited company in India. If you want to get a company legally sustainable, besides statutory filings, disclosures, and governance, you need to take care of discipline and time as well. It is a must to have knowledge for those who are starting a compliance for pvt ltd company, or are directors or investors who find ways to avoid...

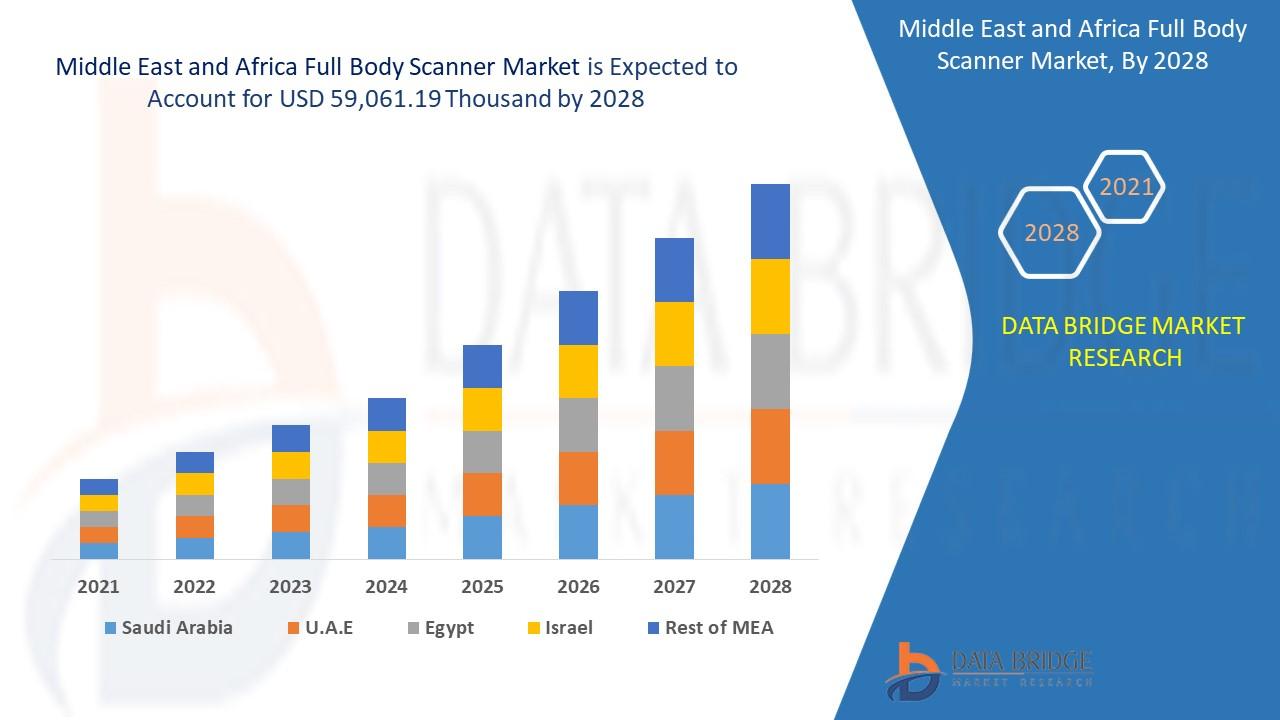

"Executive Summary Middle East and Africa Full Body Scanner Market Size and Share Forecast CAGR Value Data Bridge Market Research analyses that the market is growing at a CAGR of 7.3% in the forecast period of 2021 to 2028 and is expected to reach USD 59,061.19 thousand by 2028. This Middle East and Africa Full Body Scanner Market Research Report also conducts analysis on...

Fashion in 2026 is taking a noticeable turn toward individuality, sustainability, and meaningful design. While mass-produced accessories still exist, they no longer define style the way they once did. Instead, handmade jewelry is emerging as a powerful expression of identity and creativity. People are choosing pieces that feel personal, tell a story, and stand out in a crowd. If you’re a...

Organizar una boda es una de las experiencias más emocionantes en la vida de una pareja. Cada detalle cuenta, desde la decoración hasta el lugar donde se celebra. En este contexto, las masías boda Barcelona se han convertido en una de las opciones más demandadas por quienes buscan una celebración auténtica, elegante y rodeada de naturaleza. En este...