Highway Driving Assist Market Analysis and Opportunities

Highway Driving Assist Market Size

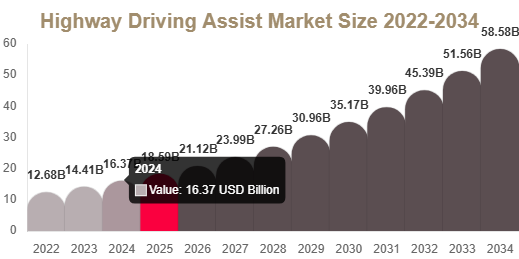

The Highway Driving Assist market size was valued at USD 18.64 billion in 2025 and is projected to reach USD 21.12 billion in 2026. By 2034, the market is expected to attain USD 58.47 billion, registering a CAGR of 13.6% during 2025–2034.

Get Your Sample Report Here: https://www.redlinepulse.com/report/highway-driving-assist-market/request-sample

Buy Now: https://www.redlinepulse.com/report/highway-driving-assist-market

Market Size & Forecast: https://www.redlinepulse.com/report/highway-driving-assist-market

The market is growing due to increasing adoption of advanced driver assistance systems, rising demand for vehicle safety, and rapid advancements in semi-autonomous driving technologies across passenger and commercial vehicles.

Market Overview

The Highway Driving Assist Market is expanding as automakers integrate adaptive cruise control, lane centering, collision avoidance, and automated steering systems into modern vehicles. These systems improve highway safety, reduce driver fatigue, and enhance driving comfort.

Growing demand for connected and intelligent vehicles is accelerating adoption, especially in electric and premium vehicle segments.

Market Drivers and Challenges

Market Drivers

Rising focus on road safety and accident prevention is a key driver, as highway driving assist systems help reduce collisions caused by driver fatigue and distraction.

Growing demand for connected and luxury vehicles is also boosting adoption, as consumers prefer advanced driving comfort and semi-autonomous features.

Market Challenges

High system cost and technical complexity remain major challenges due to expensive sensors, radar, LiDAR, and AI-based control systems required for implementation.

Market Trends

Expansion of Level 2 and Level 3 Automation

Automakers are rapidly integrating Level 2 and Level 3 autonomous systems that enable lane centering, adaptive cruise control, and semi-automated steering functions.

Sensor Fusion and Connectivity Growth

Increasing use of radar, cameras, LiDAR, and V2X communication is improving object detection, real-time decision-making, and highway navigation accuracy.

Market Segmentation

By Component Type

Sensors dominate the market with 44.36% share due to critical role in detection and navigation. LiDAR is the fastest-growing segment with 15.7% CAGR due to high accuracy in autonomous driving systems.

By Vehicle Type

Passenger vehicles dominate with 69.14% share due to high adoption of ADAS features. Commercial vehicles are growing rapidly with 14.3% CAGR due to fleet safety adoption.

By Automation Level

Level 2 automation dominates with 57.28% share due to widespread OEM integration. Level 3 automation is the fastest-growing segment with 16.2% CAGR due to autonomous driving expansion.

By Propulsion Type

Electric vehicles lead adoption with strong integration of ADAS and smart driving systems, followed by hybrid and ICE vehicles.

Regional Analysis

North America

North America holds 36.42% share due to strong adoption of advanced safety technologies and luxury vehicle penetration.

Europe

Europe accounts for 28.17% share driven by strict safety regulations and rapid adoption of intelligent mobility systems.

Asia Pacific

Asia Pacific is the fastest-growing region with 15.1% CAGR due to rapid vehicle production, EV adoption, and smart highway infrastructure in China and India.

Middle East & Africa

Growth is driven by luxury vehicle demand and smart mobility investments in countries like UAE and Saudi Arabia.

Latin America

Growth is supported by rising adoption of connected vehicles and increasing focus on road safety technologies.

Competitive Landscape

Tesla Inc.

A leader in autonomous driving software and AI-based highway navigation systems.

Robert Bosch GmbH

Provides advanced sensors, radar systems, and ADAS solutions for automotive applications.

Continental AG

Focuses on integrated driver assistance systems and intelligent mobility technologies.

Denso Corporation

Develops advanced automotive electronics and safety systems for global OEMs.

ZF Friedrichshafen AG

Specializes in ADAS technologies and automated driving systems.

Aptiv PLC

Focuses on software-defined vehicle architecture and intelligent driving systems.

Mobileye Global Inc.

Leader in computer vision and autonomous driving technology.

Valeo SA

Develops radar, LiDAR, and sensor fusion technologies for ADAS systems.

NVIDIA Corporation

Provides AI computing platforms for autonomous and assisted driving systems.

Qualcomm Technologies Inc.

Delivers connectivity and chip solutions for connected vehicle ecosystems.

Conclusion

The Highway Driving Assist Market is expected to grow rapidly due to increasing adoption of semi-autonomous driving systems, rising safety awareness, and expansion of connected vehicle technologies. With a CAGR of 13.6%, the market offers strong growth opportunities across OEM and software-driven automotive ecosystems.

Категории

Больше

Dans le paris sportif, l’analyse des données est essentielle pour élaborer des stratégies efficaces. Les plateformes fournissent des statistiques détaillées, des comparatifs d’équipes et des probabilités calculées. Les parieurs qui utilisent ces informations peuvent prendre des décisions rationnelles et augmenter leurs...

Micro Nasdaq futures have become increasingly popular among traders who want to engage in futures markets with smaller contract sizes. These contracts allow traders to gain exposure to the Nasdaq index while managing risk more effectively. Understanding how the best futures trading platforms support micro Nasdaq futures trading is essential for both beginner and experienced traders who want to...

IPL is not just cricket—it’s full of excitement, fast decisions, and non-stop action. Many users now use an online betting id to stay more connected with matches. But here’s the truth—most people make simple mistakes that cost them time, money, or even their accounts. If you are using or planning to use an online betting ID, this guide will help you avoid common errors....

"Pet Oral Care Products Market Summary: According to the latest report published by Data Bridge Market Research, the Pet Oral Care Products Market Data Bridge Market Research analyzes that the global pet oral care products market which was USD 9.8 billion in 2022, would rocket up to USD 16.4 billion by 2030, and is expected to undergo a CAGR of 6.4% during the forecast period...

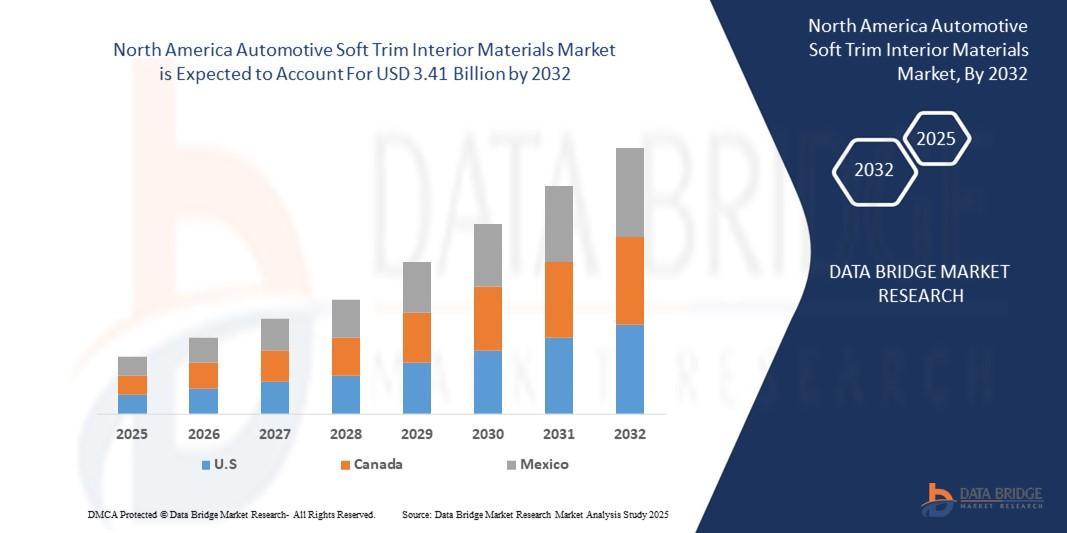

"North America Automotive Soft Trim Interior Materials Market Summary: According to the latest report published by Data Bridge Market Research, the North America Automotive Soft Trim Interior Materials Market The North America automotive soft trim interior materials market size was valued at USD 2.38 billion in 2024 and is projected to reach USD 3.41 billion by 2032, with a CAGR...