Automotive Clean Cold Technology Market Growth Forecast 2025–2034

Automotive Clean Cold Technology Market Size

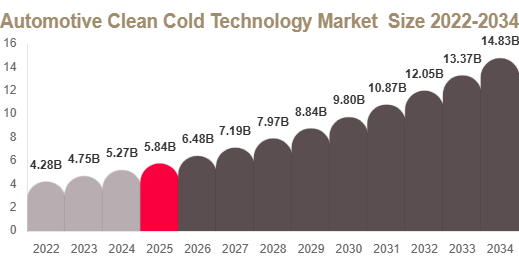

The Automotive Clean Cold Technology market size was valued at USD 5.92 billion in 2025 and is projected to reach USD 6.48 billion in 2026. By 2034, the market is expected to attain USD 14.87 billion, registering a CAGR of 10.9% during 2025–2034.

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-clean-cold-technology-market/request-sample

Buy Now: https://www.redlinepulse.com/report/automotive-clean-cold-technology-market

Market Size & Forecast: https://www.redlinepulse.com/report/automotive-clean-cold-technology-market

The market is growing due to increasing demand for low-emission engine technologies, stricter environmental regulations, and rising adoption of fuel-efficient and hybrid vehicle systems.

Market Overview

The Automotive Clean Cold Technology Market is expanding due to global emission reduction policies and increasing focus on improving engine efficiency during cold-start conditions. Automakers are adopting advanced thermal management and predictive engine systems to reduce harmful emissions.

Hybrid and electric vehicles are further boosting demand as they require advanced cold-start emission control technologies for improved efficiency and compliance with regulations.

Market Drivers and Challenges

Market Drivers

Strict global emission regulations are a major driver, forcing automakers to adopt electrically heated catalysts, thermal management systems, and advanced fuel optimization technologies.

Rising demand for hybrid and fuel-efficient vehicles is also boosting adoption as these vehicles require advanced cold-start emission control systems.

Market Challenges

High development and integration costs remain a key challenge due to complex system design, advanced sensors, and software-based engine control technologies.

Market Trends

Intelligent Thermal Management Systems

Automakers are integrating smart thermal systems and predictive heating technologies to improve catalyst efficiency during engine startup.

Predictive Engine Control Systems

AI-based predictive engine systems are being used to optimize fuel usage and reduce emissions based on driving behavior and temperature conditions.

Market Segmentation

By Technology Type

Thermal management systems dominate with 39.41% share due to strong use in emission control. Predictive engine control systems are the fastest-growing segment with 13.1% CAGR.

By Vehicle Type

Passenger vehicles dominate with 58.36% share due to high production volume. Commercial vehicles are growing fastest with 12.7% CAGR due to fleet modernization.

By Component Type

Sensors and control modules lead with 29.63% share due to real-time monitoring needs. Electrically heated catalysts are the fastest-growing segment with 13.4% CAGR.

By Fuel Type

Hybrid vehicles dominate the segment due to frequent engine restart cycles requiring advanced cold-start systems.

Regional Analysis

North America

North America holds 34.82% share due to strict emission regulations and strong adoption of hybrid vehicles and advanced engine technologies.

Europe

Europe accounts for 28.16% share driven by strict carbon emission rules and strong automotive engineering capabilities, especially in Germany.

Asia Pacific

Asia Pacific is the fastest-growing region with 12.4% CAGR due to rapid vehicle production, EV expansion, and rising environmental regulations in China and India.

Middle East & Africa

Growth is driven by increasing adoption of fuel-efficient vehicles and gradual implementation of emission standards.

Latin America

Growth is supported by rising demand for fuel-efficient vehicles and expanding automotive manufacturing base in Brazil.

Competitive Landscape

Robert Bosch GmbH

A leading provider of automotive thermal management systems, sensors, and engine control technologies.

Continental AG

Focuses on advanced emission control systems and intelligent vehicle technologies.

Denso Corporation

Develops thermal systems and engine control technologies for improved efficiency and emissions reduction.

Valeo SA

Specializes in automotive thermal systems and energy-efficient mobility solutions.

BorgWarner Inc.

Provides advanced powertrain and emission control technologies for global automotive markets.

MAHLE GmbH

Focuses on thermal management and engine system efficiency solutions.

Hitachi Astemo Ltd.

Develops integrated automotive systems including emission control and thermal technologies.

ZF Friedrichshafen AG

Specializes in mobility systems and advanced automotive control technologies.

Aptiv PLC

Focuses on intelligent vehicle architecture and software-based mobility solutions.

Schaeffler AG

Provides precision automotive components and engine efficiency technologies.

Conclusion

The Automotive Clean Cold Technology Market is expected to grow strongly due to tightening emission regulations, rising hybrid vehicle adoption, and increasing demand for fuel-efficient engine technologies. With a CAGR of 10.9%, the market will continue expanding across OEM and advanced mobility ecosystems.

الأقسام

إقرأ المزيد

The impression die forging market is witnessing significant growth due to increasing demand for high strength metal components across automotive, aerospace, construction, industrial machinery, and energy industries. Impression die forging is a manufacturing process that shapes heated metal into desired forms using specially designed dies under high pressure. The process is widely preferred for...

Patch 2.5.3 for Season 11: Divine Intervention is now live! Explore all the newest hotfix updates included in this release on Maxroll! An issue that blocked players from claiming reward caches during the Lunar New Year event has been fixed. Fixed a problem where some purchased cosmetics couldn't be accessed. Dive into the Season of Divine Intervention with our updated Season 11 compendium....

Achieving ce certification is a major milestone for any manufacturer looking to sell products in the European market. This mark not only represents compliance with EU safety, health, and environmental requirements but also builds customer trust and expands market access. However, many businesses find the journey confusing, especially if they are new to regulatory processes. This guide breaks...

Jake Hoffmeister may be a present-day religious professor best known meant for this interpretations associated with a System during Delights (ACIM), a good copy guided toward forgiveness, inborn peace of mind, together with non-dual interest. Gradually, he has crafted a worldwide adhering to thru r david hoffmeister reviews etreats, on line teachings, training books, together with network...

As men grow older, maintaining optimal health becomes a priority, especially when it comes to prostate wellness. Many men begin to experience uncomfortable symptoms such as frequent urination, poor bladder control, interrupted sleep, and reduced confidence in daily life. These issues often arise due to changes in prostate health and hormonal balance. Fortunately, natural wellness solutions are...