Dry Chemistry Analyzer Market Forecast 2034: Rising Demand for Personalized Diagnostics to Drive Global Industry Beyond USD 33.2 Billion

The global dry chemistry analyzer market is witnessing significant momentum due to the growing burden of chronic diseases, rising adoption of personalized medicine, and increasing demand for rapid diagnostic testing services across hospitals and laboratories. Dry chemistry analyzers have become essential tools in modern clinical diagnostics as they provide precise, contamination-free, and cost-effective biochemical analysis without the need for liquid reagents.

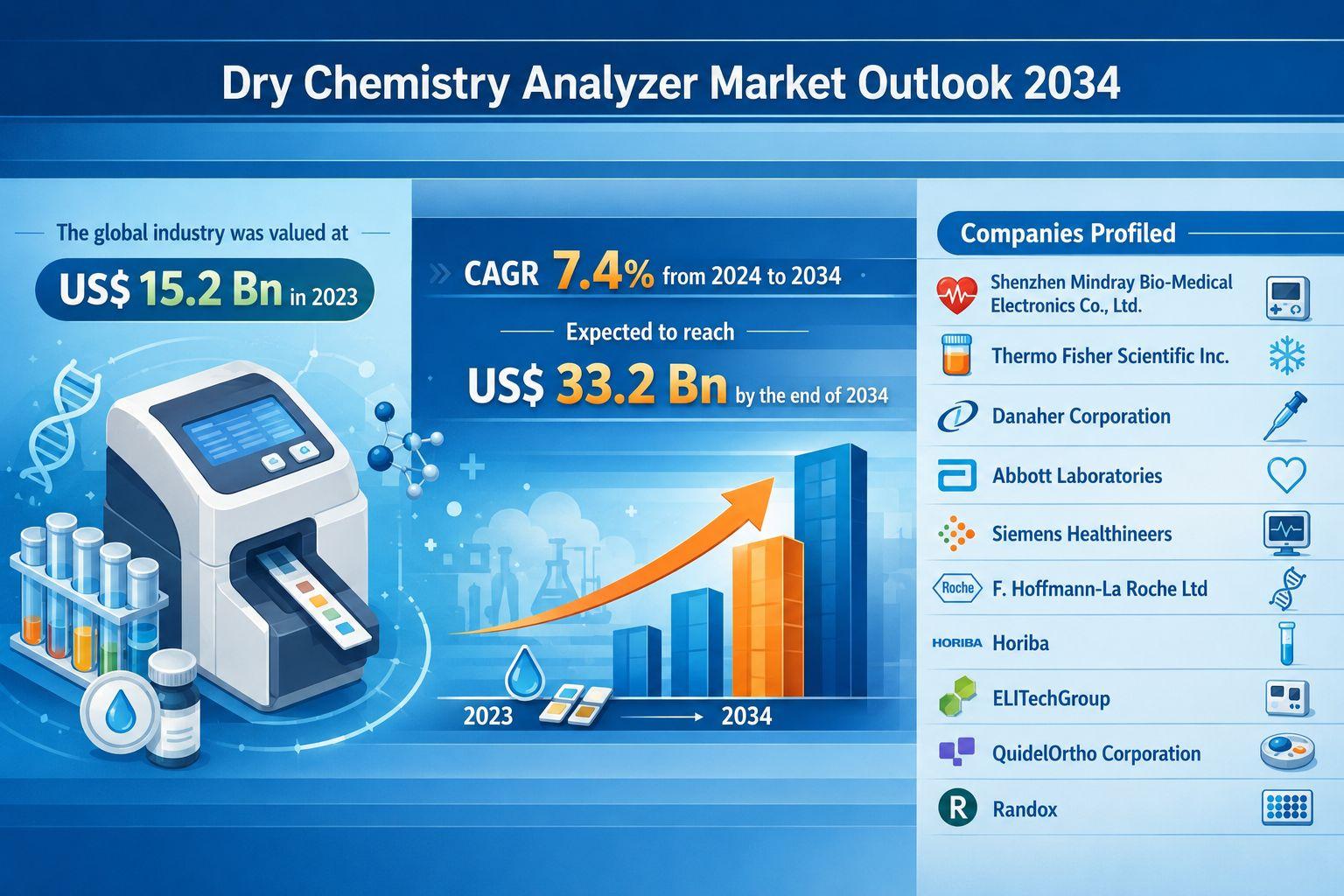

According to industry estimates, the global dry chemistry analyzer market was valued at US$ 15.2 Bn in 2023 and is projected to reach US$ 33.2 Bn by the end of 2034, expanding at a CAGR of 7.4% during the forecast period from 2024 to 2034. The market is benefiting from technological advancements, growing healthcare expenditures, and increasing preference for decentralized diagnostic systems.

Growing Demand for Diagnostic Services Accelerating Market Expansion

The increasing prevalence of chronic diseases such as diabetes, cardiovascular disorders, kidney diseases, and cancer is one of the major factors propelling demand for dry chemistry analyzers globally. These analyzers are widely used for evaluating cholesterol levels, blood glucose, liver function, electrolyte balance, and various biomarkers critical for clinical decision-making.

The growing diabetic population continues to create substantial opportunities for diagnostic equipment manufacturers. According to the International Diabetes Federation (IDF) Diabetes Atlas Tenth Edition 2021, around 537 million adults worldwide were living with diabetes in 2021, and this number is expected to rise to 643 million by 2030. This sharp increase in chronic disease cases is directly contributing to higher demand for advanced diagnostic systems capable of delivering accurate and rapid results.

Dry chemistry analyzers are preferred because they minimize contamination risks and require less maintenance compared to conventional wet chemistry systems. Their ability to handle multiple sample types including blood, plasma, cerebrospinal fluid, and urine makes them highly versatile across clinical environments.

Personalized Medicine Creating New Growth Opportunities

The shift toward precision medicine and biomarker-based diagnostics is playing a pivotal role in transforming the dry chemistry analyzer industry. Healthcare providers are increasingly relying on patient-specific molecular and biochemical information to design personalized treatment plans.

Dry chemistry analyzers support personalized medicine by delivering highly accurate biomarker analysis while eliminating the complexity associated with fragile liquid reagents. These systems use electricity, light, or heat to induce chemical reactions within samples, enabling healthcare professionals to obtain reliable diagnostic outcomes in less time.

The growing emphasis on individualized therapies, targeted drug formulations, and customized dosages is expected to further boost adoption of dry chemistry analyzers in clinical laboratories and hospitals worldwide. Moreover, the ability of these analyzers to assist in detecting cardiovascular risks through C-reactive protein analysis from dried blood spots is opening new pathways for innovation.

Manufacturers are also exploring applications in metabolite analysis and food quality evaluation, expanding the technology’s potential beyond traditional healthcare diagnostics.

Advantages of Dry Chemistry Analyzers Supporting Wider Adoption

Dry chemistry analyzers offer several operational and economic advantages that are fueling their adoption across healthcare settings. One of the key benefits is their high level of analytical accuracy achieved through techniques such as colorimetry, potentiometry, and titration.

These systems are capable of handling both liquid and solid samples, enabling laboratories to perform a broad range of diagnostic tasks using a single platform. Reduced contamination risk and lower maintenance requirements also make them cost-efficient solutions for hospitals and diagnostic laboratories.

In addition, dry chemistry analyzers help streamline laboratory workflows by delivering rapid turnaround times and minimizing manual intervention. This is particularly important in emergency care and point-of-care testing environments where quick diagnostic decisions are essential.

The rise in decentralized healthcare infrastructure and demand for portable diagnostic systems is further supporting the market’s long-term expansion.

Technological Advancements Driving Industry Innovation

Continuous technological advancements and regular product launches are reshaping the competitive landscape of the dry chemistry analyzer market. Companies are focusing on improving automation, throughput capacity, workflow efficiency, and multi-parameter testing capabilities.

In July 2022, EDAN Instruments, Inc. introduced its fluorescence-based point-of-care blood gas and chemistry analysis system called i20. The analyzer is capable of measuring more than 45 parameters including blood gases, electrolytes, and CO-oximetry, demonstrating the industry’s move toward integrated diagnostic platforms.

Similarly, in May 2022, Mindray launched the BS-600M chemistry analyzer designed to improve reliability, productivity, and efficiency in medium-volume laboratories. Such innovations are enabling laboratories to handle growing testing volumes while maintaining diagnostic accuracy.

Automation is becoming increasingly important in hematology and clinical chemistry testing. In May 2023, Siemens Healthineers introduced the Atellica HEMA 570 and 580 analyzers equipped with intuitive interfaces, automation connectivity, and rules-based testing functionalities aimed at optimizing laboratory workflows.

The integration of artificial intelligence, cloud connectivity, and digital healthcare technologies is expected to further revolutionize diagnostic operations during the forecast period.

North America Dominates the Global Market

North America accounted for the largest share of the global dry chemistry analyzer market in 2023 and is expected to maintain its leadership position through 2034. The region’s dominance is attributed to the high incidence of chronic diseases, advanced healthcare infrastructure, and strong adoption of innovative diagnostic technologies.

The United States and Canada continue to witness increasing cases of cancer, diabetes, and cardiovascular disorders, creating sustained demand for diagnostic testing services. According to the Canadian Cancer Society, nearly 299,200 new cancer cases were diagnosed in Canada in 2021 alone.

Technological collaborations and partnerships are also strengthening the regional market landscape. In February 2021, Thermo Fisher Scientific partnered with Mindray to provide advanced clinical chemistry analyzers to forensic and clinical laboratories across the U.S. and Canada. The partnership included deployment of the BA-800M and BS-480 analyzers capable of performing 800 and 400 tests per hour respectively.

Meanwhile, Asia Pacific is anticipated to emerge as a highly lucrative market due to expanding healthcare infrastructure, increasing healthcare awareness, rising disposable income, and growing investments in diagnostic laboratories across countries such as China and India.

Hospitals and Diagnostic Laboratories Remain Major End-users

Hospitals and diagnostic laboratories collectively represent the largest end-user segment in the dry chemistry analyzer market. The growing patient pool, increasing laboratory testing volumes, and rising focus on early disease diagnosis are driving adoption across these facilities.

Diagnostic laboratories prefer dry chemistry analyzers due to their operational efficiency, reduced reagent handling requirements, and ability to process high sample volumes with improved accuracy. Hospitals are increasingly deploying fully automated analyzers to enhance patient care and minimize diagnostic turnaround times.

Biopharmaceutical companies and research institutes are also contributing to market growth by utilizing dry chemistry analyzers in drug development, biomarker discovery, and clinical research applications.

Competitive Landscape Remains Highly Dynamic

The global dry chemistry analyzer market is highly competitive with major players focusing on product innovation, acquisitions, partnerships, and geographical expansion strategies.

Leading companies operating in the market include Thermo Fisher Scientific, Siemens Healthineers, Abbott Laboratories, Danaher Corporation, F. Hoffmann-La Roche Ltd, Shenzhen Mindray Bio-Medical Electronics Co., Ltd., Horiba, QuidelOrtho Corporation, Randox, and ELITechGroup.

Strategic acquisitions are also shaping the competitive environment. In March 2023, Thermo Fisher Scientific completed the acquisition of Binding Site Group for US$ 2.8 Bn to strengthen its specialized diagnostics portfolio and meet rising demand for advanced diagnostic solutions.

Future Outlook

The future of the dry chemistry analyzer market appears highly promising as healthcare systems worldwide continue emphasizing early disease detection, precision diagnostics, and personalized treatment approaches. Rising geriatric population levels are expected to significantly contribute to market growth, with the World Health Organization estimating that nearly 16.5% of the global population will be aged 60 years and above by 2030.

Advancements in automation, point-of-care testing, and biomarker analysis are expected to transform diagnostic workflows and create new commercial opportunities for market participants. The growing preference for rapid, reliable, and low-maintenance diagnostic solutions will continue driving demand across hospitals, laboratories, and research facilities.

As healthcare providers increasingly prioritize efficiency, accuracy, and patient-centric care, dry chemistry analyzers are expected to become indispensable components of modern diagnostic infrastructure over the next decade.

Κατηγορίες

Διαβάζω περισσότερα

Adding collagen to your routine doesn’t need to involve messy powders or oversized capsules. That’s why Your Gummy Vitamins created premium gummy collagen designed for people who want a simple, enjoyable, and consistent way to include collagen in their daily lifestyle. This chewable option offers a modern alternative to traditional formats. Instead of measuring scoops or swallowing...

Homeowners today are increasingly focused on improving energy efficiency, reducing utility costs, and creating more comfortable indoor living spaces. One of the most effective ways to achieve all three is through modern window upgrades designed for insulation and performance. In particular, Energy-Efficient Windows in Sachse, TX have become a popular solution for homeowners looking to...

When traveling internationally, your Netflix library may shrink due to regional restrictions. Windscribe offers specialized servers labeled “Windflix” designed to securely access specific Netflix libraries—including those of the US, UK, Canada, and Japan—from anywhere in the world. By masking your real IP address, these servers let you stream as if you were back home....

Exactitude Consultancy has just released a new report that dives into the global Monoethylene Glycol (MEG) market. It explores everything from market size and share to demand and forecasts all the way through 2033. By analyzing historical data alongside current trends, the report sheds light on competitive strategies and the key factors driving market growth. Get FREE Sample Copy of...

The Essentials Fear of God collection has become a global streetwear phenomenon, merging high-end fashion aesthetics with everyday comfort. As a sub-line of Jerry Lorenzo’s iconic Fear of God brand, Essentials delivers timeless silhouettes, premium fabrics, and minimalist designs that redefine modern casualwear. In this guide, we dive deep into everything you need to know—from...