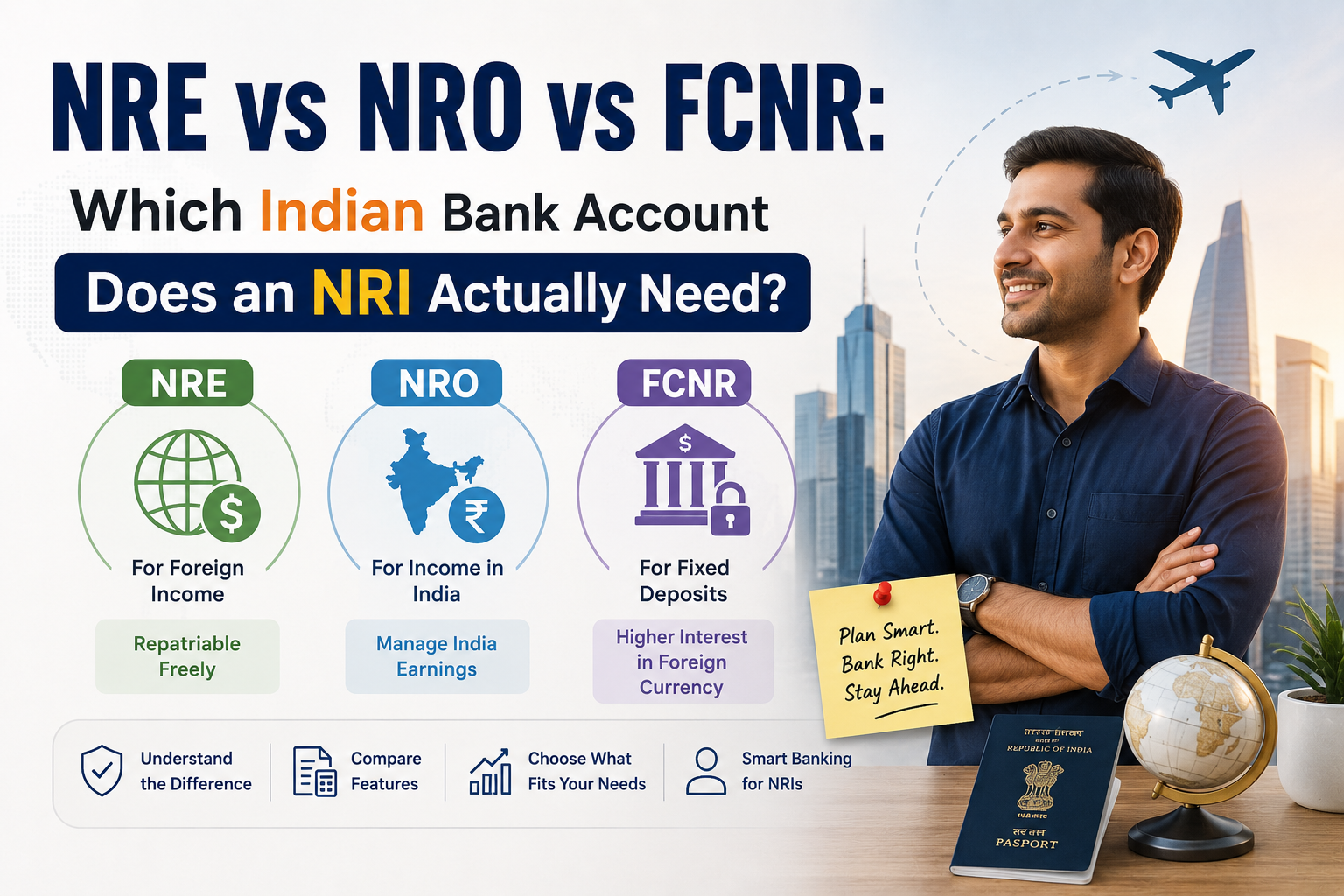

NRE vs NRO vs FCNR: Which Indian Bank Account Does an NRI Actually Need?

When an Indian professional moves abroad and becomes an NRI, their existing Indian savings account opened as a resident automatically becomes a status mismatch. The Reserve Bank of India requires NRIs to maintain designated NRI accounts rather than resident accounts, and the choice between them has practical consequences for taxes, repatriation, and how transferred funds can be used.

Most NRIs maintain at least one NRE or NRO account. Many maintain both. The accounts serve different purposes, and the choice of which account to receive remittances into has consequences for how freely those funds can later be moved.

The Three NRI Account Types: What Each One Does

NRE Account (Non-Resident External)

An NRE account holds funds in Indian rupees but is funded exclusively from foreign income money earned abroad and sent to India. It is the account designed specifically to receive remittances.

Key characteristics:

- Interest is tax-free in India interest earned on NRE fixed deposits and savings accounts is exempt from Indian income tax

- Fully repatriable both the principal and interest in an NRE account can be freely transferred back abroad at any time, without limit and without requiring RBI permission

- Joint holding with another NRI or a resident Indian (on a former-or-survivor basis) is permitted

- Cannot receive India-sourced income rental income from Indian property, dividends from Indian stocks, or income from business conducted in India cannot be deposited into an NRE account

The NRE account is the right choice for receiving remittances from Europe. Funds deposited here are freely repatriable if you later need to return them to your European account, you can do so without restriction.

NRO Account (Non-Resident Ordinary)

An NRO account is designed to receive and manage income earned in India: rent from property, dividends, pension, or any other India-sourced income. It can also receive remittances from abroad, but funds deposited here are subject to different rules.

Key characteristics:

- Interest is taxable in India at applicable TDS rates (typically 30% for NRIs, potentially reduced by DTAA)

- Restricted repatriation only up to USD 1 million per financial year can be repatriated from an NRO account, and this requires Form 15CA/15CB documentation and a chartered accountant certificate

- Accepts both foreign and India-sourced funds it is the only account that can receive both

- TDS on interest the bank deducts tax at source on interest earned

Detailed guidance on the repatriation rules and practical process for transferring funds from an NRO account covers the documentation requirements and common issues NRIs encounter when moving NRO funds abroad.

FCNR Account (Foreign Currency Non-Resident)

FCNR accounts hold funds in the original foreign currency euros, dollars, pounds without converting to rupees. This eliminates the currency risk that NRE and NRO accounts carry: if the rupee depreciates while funds are in an NRE account, the euro-equivalent value of those rupees falls.

Key characteristics:

- Available as fixed deposits only no current or savings account option

- Currency risk elimination funds remain in the original currency until withdrawn

- Tax-free interest in India like NRE accounts

- Fully repatriable principal and interest can be returned abroad freely

- Minimum tenure typically 1 year, maximum 5 years

FCNR accounts are most useful for NRIs holding large amounts in India for a defined future purpose a property purchase planned for 2–3 years hence, or funds being saved for return to India where currency risk is a concern.

Which Account Should You Use for Remittances?

For most NRIs sending regular monthly remittances from Europe to India, the NRE savings account is the right receiving account. Here's why:

- Tax-free interest means the funds grow without tax drag while they wait to be used

- Full repatriability preserves your options if you need the money back in Europe, you can move it without regulatory complexity

- No India-source income contamination keeping your NRE account clean for foreign-sourced funds (remittances) maintains its tax-advantaged status

- Simpler documentation for repatriation compared to NRO

If you also have India-sourced income rental income from property you own in India, dividends from Indian stocks, freelance income from Indian clients that income must go to an NRO account. Keep the two accounts separate for their intended purposes.

The Repatriation Consideration for Large Transfers

When NRIs send large sums to India — for property purchases, large gifts, or business investment — the choice of receiving account has long-term consequences if that money might later need to return abroad.

Funds received in NRE account: Can be repatriated freely, at any time, in any amount, without documentation or approvals. If you buy property in India and later sell it, the sale proceeds received in an NRE account are repatriable up to the original foreign investment amount.

Funds received in NRO account: Subject to the USD 1 million annual repatriation limit, requiring Form 15CA/15CB and a CA certificate. Property sale proceeds from property originally purchased with NRO funds face more documentation requirements for repatriation.

Understanding NRI repatriation rules before committing large sums to India helps structure the transaction correctly from the start rather than discovering repatriation constraints later.

How to Open an NRE or NRO Account from Europe

Most major Indian banks offer NRI account opening through online or postal processes that do not require an in-person branch visit in India. The standard documentation required:

- Valid Indian passport (or OCI card for OCI holders)

- Proof of overseas address (utility bill, bank statement, or residency permit)

- Proof of NRI status (work permit, employment letter, or visa)

- Recent passport-size photographs

- Completed account opening form (bank-specific)

Some banks require notarization or attestation of documents by an Indian embassy or notary. Courier-based account opening processes typically take 2–4 weeks from document submission to account activation.

For NRIs already in India on a visit, in-branch account opening is faster typically completed within a week with original documents presented in person.

Practical Account Management Tips

Maintain a minimum balance: NRE savings accounts typically require a minimum quarterly average balance of ₹10,000–50,000 depending on the bank. Falling below minimum balance triggers penalty charges. Check the specific requirements for your bank.

Nominate a resident for the account: Nominating a resident Indian family member as nominee for your NRE/NRO accounts simplifies account access in the event of your incapacitation or death without creating ownership complexity.

Link your transfer platform to your NRE account: When setting up a remittance platform, specify your NRE account as the receiving account for remittances from abroad. This keeps the NRE account funded with foreign-source income and preserves its full tax-advantaged and repatriable status.

Keep accounts separate for their purpose: Do not deposit India-sourced income into NRE accounts. If you receive rental income or dividends, direct those to your NRO account. Commingling income sources in an NRE account can complicate the tax-advantaged treatment.

Final Thought

NRE, NRO, and FCNR accounts each serve a distinct function in an NRI's financial architecture. The account you use to receive remittances affects the tax treatment of earnings on those funds, your ability to later repatriate them, and the documentation required when you do.

Choosing the right account structure at the beginning before remittances start flowing simplifies financial management for the entire duration of your time abroad. Most NRIs benefit from maintaining both an NRE account (for remittances) and an NRO account (for India-sourced income), keeping each funded appropriately for its purpose.

Categorias

Leia mais

Get updated and reliable GDPR Dumps, GDPR Exam Dumps, and GDPR PDF Dumps from DumpsHero for effective exam preparation. Prepare smarter with expert-verified study materials designed to help you succeed in your PECB GDPR certification exam on the first attempt. GDPR Exam Dumps for Impressive Results on Your First Attempt DumpsHero provides highly reliable PECB GDPR Exam Dumps perfectly...

The Global Epigenetics Market is witnessing unprecedented growth, driven by cutting-edge research, technological innovations, and rising clinical applications. According to The Insight Partners, the Epigenetics market is projected to expand from US$ 11.12 billion in 2024 to US$ 35.84 billion by 2031, registering a strong Compound Annual Growth Rate (CAGR) of 18.3% between 2025 and 2031. This...

"Detailed Analysis of Executive Summary Argentine Wne Market Size and Share The global Argentine wine market size was valued at USD 10.45 billion in 2024 and is expected to reach USD 10.69 billion by 2032, at a CAGR of 6.8% during the forecast period Argentine Wne Market report consists of significant data that provides future forecasts and detailed...

When it comes to protecting people, property, and valuable assets, choosing the right security provider is critical. High-risk environments require trained professionals who can respond quickly, make smart decisions under pressure, and maintain a strong security presence. Noble Shields LLC offers professional Armed security guard services designed to protect businesses, facilities, and...

"3D Printing Plastic Market Summary: According to the latest report published by Data Bridge Market Research, the 3D Printing Plastic Market The global 3D printing plastic market size was valued at USD 1.53 billion in 2025 and is expected to reach USD 10.83 billion by 2033, at a CAGR of 27.70% during the forecast period. 3D Printing Plastic...