Scanning Electron Microscopes (SEM) for Semiconductor Industry: The Invisible Infrastructure That Measures Every Nanometer Before a Chip Becomes Real

A chip fab does not only manufacture silicon; it manufactures certainty. In a 300 mm wafer line carrying 50,000 to 100,000 wafer starts per month, one small patterning drift can multiply into millions of defective transistors before the next shift ends. That is why Scanning Electron Microscopes (SEM) for Semiconductor Industry have moved from laboratory instruments to production infrastructure. They are not sitting at the edge of the fab as analytical machines; they are embedded inside the rhythm of lithography, etch, deposition, cleaning, defect review, and yield ramp.

Semple Request At : https://datavagyanik.com/reports/scanning-electron-microscopes-sem-for-semiconductor-industry-market/

The logic is simple: when a transistor gate, contact hole, via, trench, metal line, or EUV pattern moves by even a few nanometers, electrical behavior changes. A 2 nm to 5 nm deviation may look invisible to optical systems, but it can alter leakage, resistance, overlay behavior, and yield. Scanning Electron Microscopes (SEM) for Semiconductor Industry convert these hidden variations into measurable signals by scanning electron beams across wafer surfaces and converting secondary electron response into dimensional, defect, and morphology data. Hitachi High-Tech describes CD-SEM as a dedicated system for measuring fine semiconductor wafer patterns, mainly used in manufacturing lines, with automated cassette-based wafer handling and recipe-driven measurement.

The infrastructure behind Scanning Electron Microscopes (SEM) for Semiconductor Industry starts with tool placement. In a modern fab, SEM capacity is not planned like a general inspection room; it is planned by process control intensity. A fab running 40 to 60 critical layers may need SEM checkpoints after lithography development, after etch, after hard-mask transfer, after contact opening, after metal patterning, and during excursion investigation. If only 5% to 10% of lots require high-resolution SEM review at a given layer, a high-volume fab can still generate hundreds of SEM jobs every day. That turns SEM from a “microscope” into a traffic-managed production asset.

The first use case is critical dimension control. Scanning Electron Microscopes (SEM) for Semiconductor Industry measure line width, hole diameter, pitch behavior, line-edge roughness, line-width roughness, and local pattern collapse. In EUV layers, the problem is not only whether the printed line exists; it is whether the line is stable across the wafer, across the field, across exposure dose, and across resist chemistry. Hitachi notes that CD-SEM uses SEM image contrast and line profiles to calculate dimensions automatically, with measurement operations commonly applied after development and after etching for contacts, vias, and wiring width.

The second use case is defect review. Optical inspection can flag a wafer location at high speed, but the fab still needs to know whether the signal is a killer defect, nuisance defect, particle, bridge, void, residue, pattern collapse, scratch, or voltage-contrast issue. Scanning Electron Microscopes (SEM) for Semiconductor Industry provide the image evidence that converts a defect coordinate into a process decision. KLA’s e-beam review systems, for example, are positioned for high-resolution defect imaging, automatic inline defect classification, wafer dispositioning, hotspot discovery, EUV print check, process-window discovery, and bevel-edge review.

The third use case is yield learning. A fab does not buy Scanning Electron Microscopes (SEM) for Semiconductor Industry only to inspect bad wafers; it buys them to reduce the time between “something changed” and “the root cause is known.” In ramp-up, every hour matters. If a line is producing 2,000 wafers per day and a yield excursion affects even 3% of lots, the economic exposure can reach thousands of die within one production window. SEM review compresses the feedback loop: lithography engineers see whether a focus-dose issue created bridging, etch engineers see whether profile transfer failed, and integration teams see whether a recurring defect maps to a specific module.

The market-size paragraph should sit here because the reader already understands the operational dependency. According to DataVagyanik, the Scanning Electron Microscopes (SEM) for Semiconductor Industry market in 2026 is positioned as a specialized high-value segment inside semiconductor metrology, inspection, and process-control infrastructure, with the forecast shaped by EUV adoption, 3 nm and 2 nm node development, advanced packaging, SiC/GaN power devices, and AI/HBM capacity expansion. DataVagyanik attributes the forward growth of Scanning Electron Microscopes (SEM) for Semiconductor Industry to higher SEM sampling density per wafer, more defect-review loops per critical layer, and broader use of SEM imaging in both front-end wafer fabs and advanced wafer-level packaging lines.

The spending trend around this infrastructure is supported by the wider equipment cycle. SEMI projected wafer fab equipment sales to grow from a record $104 billion in 2024 to $115.7 billion in 2025, then expand 9.0% in 2026, with WFE reaching $135.2 billion in 2027. The same SEMI forecast links equipment growth to DRAM, HBM, advanced logic, China capacity build-out, and leading-edge technologies moving toward 2 nm gate-all-around manufacturing. This matters because Scanning Electron Microscopes (SEM) for Semiconductor Industry follow the same physical driver: when process complexity increases, measurement density increases.

In logic fabs, SEM demand is tied to EUV and GAA. A 3 nm or 2 nm device does not give process engineers the luxury of wide margins. EUV stochastic defects, contact edge variation, buried pattern distortion, and local CD variation require high-resolution review. ASML’s HMI eScan 1100 is designed for 3 nm and beyond, using 25 beams and targeting up to 15 times higher throughput than single e-beam inspection tools. It is positioned for high-throughput, high-resolution e-beam inspection in volume manufacturing environments. That is the infrastructure story: speed is being engineered into SEM because fabs cannot wait for slow nanometer visibility.

In memory fabs, Scanning Electron Microscopes (SEM) for Semiconductor Industry behave differently. DRAM and HBM need SEM for patterning control, capacitor structures, contacts, vias, and overlay-sensitive features. 3D NAND adds another workload: high-aspect-ratio channels, staircase structures, multilayer etch behavior, and defect classification across vertically stacked layers. SEMI projected DRAM equipment sales to rise 15.4% in 2025, followed by 15.1% growth in 2026, while NAND equipment was expected to grow 45.4% in 2025 and 12.7% in 2026. Each of these capacity cycles increases the need for electron-beam review because vertical complexity creates failure modes that are difficult to interpret through optical inspection alone.

In advanced packaging, Scanning Electron Microscopes (SEM) for Semiconductor Industry are becoming equally relevant. The semiconductor industry is shifting from single-die scaling to system-level scaling through chiplets, 2.5D interposers, hybrid bonding, fan-out packaging, microbumps, through-silicon vias, and redistribution layers. A 10 µm bump, a 2 µm RDL line, or a sub-micron bonding defect can create reliability risk in an AI accelerator package costing hundreds or thousands of dollars. KLA positions its eDR7380 e-beam review system for advanced wafer-level packaging, wide-bandgap semiconductors, and multiple wafer sizes including 150 mm, 200 mm, and 300 mm.

The technical infrastructure also includes environmental control. Scanning Electron Microscopes (SEM) for Semiconductor Industry need vibration isolation, stable temperature, clean vacuum architecture, contamination control, high-speed wafer stages, recipe libraries, defect classification software, and connection to factory automation systems. A SEM tool is not productive if it only captures sharp images; it must move wafers through FOUP handling, align coordinates from optical inspectors, execute recipes, classify defects, and return data to manufacturing execution systems. Hitachi’s CG7300 highlights EUV-era mass-production metrology, improved tool-to-tool matching by around 10% versus its previous model, anti-charging high-speed scanning, and improved CD uniformity scanning.

This is why Scanning Electron Microscopes (SEM) for Semiconductor Industry are best understood as data infrastructure, not imaging hardware. Every SEM image becomes part of a control loop. One image supports defect pareto creation. One wafer map supports excursion containment. One CD trend supports dose correction. One review recipe supports process-window qualification. One voltage-contrast image can expose an electrical failure before final test. In a fab where a single advanced lithography scanner can cost hundreds of millions of dollars and a single wafer can carry thousands of high-value die, SEM is the instrument that tells the fab whether expensive process steps are still inside the economic window.

How SEM Turns Semiconductor Manufacturing Into a Nanometer-Level Control System

The fourth use case is voltage contrast inspection. Scanning Electron Microscopes (SEM) for Semiconductor Industry are not limited to surface shape; they can also reveal electrical behavior by showing charging differences across features. In semiconductor manufacturing, a visually correct structure can still fail electrically because of an open contact, incomplete via, local isolation failure, or buried connection problem. Voltage contrast SEM helps identify these issues before the wafer reaches final electrical testing. If one failed via chain repeats across even 1% of a 300 mm wafer lot, the hidden yield loss can become significant because the failure is not always visible through optical review.

The fifth use case is process recipe qualification. When a fab introduces a new resist, etch chemistry, hard mask, cleaning sequence, or deposition stack, Scanning Electron Microscopes (SEM) for Semiconductor Industry provide the before-and-after evidence. For example, a line that measures 18 nm after lithography may shift to 15 nm after etch if the etch bias is too aggressive. A contact hole designed at 28 nm may show footing, taper, or incomplete opening depending on plasma conditions. SEM images quantify these changes and help engineers lock recipes before the process moves into high-volume manufacturing.

The sixth use case is material interface understanding. Semiconductor devices are now built from dozens of material systems: silicon, silicon germanium, silicon nitride, silicon oxide, low-k dielectrics, high-k dielectrics, copper, cobalt, ruthenium, tungsten, titanium nitride, tantalum nitride, photoresists, hard masks, and compound semiconductor layers. Scanning Electron Microscopes (SEM) for Semiconductor Industry help engineers study whether these material interfaces are clean, rough, cracked, over-etched, under-etched, contaminated, or mechanically stressed. In a 3D NAND structure with more than 200 stacked layers, even a small profile distortion can affect channel performance across millions of memory cells.

A modern SEM workflow usually begins with another inspection system. Optical inspection scans the wafer quickly and produces defect coordinates. The SEM then revisits selected coordinates with higher magnification. In a high-volume fab, this means Scanning Electron Microscopes (SEM) for Semiconductor Industry must integrate with defect maps, wafer IDs, lot histories, product recipes, and process-step metadata. A defect is not only an image; it is a coordinate, layer, process chamber, recipe version, exposure field, wafer slot, and time stamp. When these data points are connected, the SEM becomes a manufacturing intelligence node.

This explains why throughput has become as important as resolution. A single-beam SEM can deliver exceptional detail, but fabs need faster review when defect density rises or when sampling plans expand. Multi-beam e-beam platforms exist because the industry cannot trade all speed for resolution. In advanced logic and memory fabs, the relevant question is not “Can we see the defect?” The more important question is “Can we see enough defects quickly enough to control the line?” Scanning Electron Microscopes (SEM) for Semiconductor Industry are therefore being engineered around beam current, landing energy, stage speed, automation, image processing, and classification accuracy.

The infrastructure cost also extends beyond the tool itself. A semiconductor-grade SEM cell requires cleanroom floor space, sub-fab utility support, chilled water, vacuum systems, stable power, vibration damping, controlled electromagnetic interference, wafer handling modules, calibration wafers, maintenance kits, and software integration. If one production SEM occupies several square meters of cleanroom space, its real cost includes the opportunity cost of that space inside a fab where every square meter competes with lithography, etch, deposition, metrology, and inspection tools. Scanning Electron Microscopes (SEM) for Semiconductor Industry therefore carry both capital cost and fab-layout cost.

The people infrastructure is equally important. SEM output is only useful when process engineers, yield engineers, defect engineers, metrology teams, equipment engineers, and data scientists interpret it correctly. A 24-hour fab may need multiple engineers and technicians trained in recipe setup, image review, defect classification, charging behavior, beam damage risk, and tool matching. In a large semiconductor site, the number of SEM-related workflows can easily span lithography control, etch control, contamination review, failure analysis, packaging inspection, and customer-return investigation. Scanning Electron Microscopes (SEM) for Semiconductor Industry create a specialist layer inside the fab workforce.

The application map can be divided into five manufacturing zones. First is lithography, where SEM checks photoresist CDs, pattern fidelity, bridging, scumming, and line-edge roughness. Second is etch, where SEM validates pattern transfer, sidewall shape, trench depth signals, residue, and microloading. Third is deposition and CMP, where SEM helps investigate film roughness, voids, dishing, erosion, and particle-related defects. Fourth is electrical yield learning, where voltage contrast and defect review connect physical structures with device behavior. Fifth is advanced packaging, where SEM validates microbumps, RDL, hybrid bonding, TSV structures, and wafer-level package defects. Across these zones, Scanning Electron Microscopes (SEM) for Semiconductor Industry support both control and diagnosis.

The node dependency is clear. At older nodes such as 90 nm, 65 nm, and 45 nm, SEM remains useful but optical tools can cover a large share of routine control. At 28 nm, 14 nm, 7 nm, 5 nm, 3 nm, and upcoming 2 nm nodes, SEM becomes more deeply embedded because the physical features are closer to the limits of optical resolution. A mature-node fab may use SEM heavily for power devices, analog structures, MEMS, or compound semiconductors, but a leading-edge logic fab uses it as part of daily process control. Scanning Electron Microscopes (SEM) for Semiconductor Industry therefore scale not only with wafer volume but with pattern complexity.

The strongest growth logic comes from three structural shifts. The first is EUV lithography. EUV reduces multi-patterning steps, but it creates stochastic defects, random microbridges, missing contacts, and local CD variability that must be reviewed at high resolution. The second is gate-all-around transistor manufacturing, where nanosheet and nanowire structures increase the importance of profile control and local process uniformity. The third is heterogeneous integration, where multiple dies are assembled in packages with increasingly fine interconnect structures. Each shift increases the number of points where Scanning Electron Microscopes (SEM) for Semiconductor Industry can protect yield.

Regional infrastructure also matters. Taiwan, South Korea, Japan, the United States, Europe, and mainland China all use SEM differently because their semiconductor ecosystems are different. Taiwan’s demand is weighted toward advanced foundry logic and advanced packaging. South Korea’s demand is heavily tied to DRAM, HBM, NAND, and logic investments. Japan remains important through equipment, materials, metrology expertise, and specialty semiconductor manufacturing. The United States is adding demand through new logic, memory, and advanced packaging capacity. Europe brings demand from automotive chips, power devices, compound semiconductors, and research-to-production facilities. China’s demand is broad because domestic fabs are expanding mature-node, memory, power, analog, and packaging capacity. In all these ecosystems, Scanning Electron Microscopes (SEM) for Semiconductor Industry follow wafer capacity, node difficulty, and yield sensitivity.

The supplier ecosystem is concentrated around companies with deep electron optics, wafer automation, software, and fab integration capability. Hitachi High-Tech is one of the most visible CD-SEM suppliers in semiconductor manufacturing. KLA is strong in defect review and inspection-linked workflows. Applied Materials participates in e-beam metrology and inspection through its process-control portfolio. ASML, through its HMI e-beam platform, connects electron-beam inspection with lithography-driven process control. JEOL and Thermo Fisher Scientific are important in SEM and electron microscopy broadly, with relevance in semiconductor labs, failure analysis, and materials characterization. This supplier structure shows that Scanning Electron Microscopes (SEM) for Semiconductor Industry are not a commodity instrument market; they are a precision equipment ecosystem.

Semple Request At : https://datavagyanik.com/reports/scanning-electron-microscopes-sem-for-semiconductor-industry-market/

Категории

Больше

Introduction The spaces we live and work in have a direct impact on our comfort, productivity, and overall well-being. A thoughtfully designed environment can transform an ordinary room into a place that feels welcoming, organized, and purposeful. As lifestyles continue to evolve, people are placing greater emphasis on creating interiors that reflect their personalities while supporting...

Planning a major celebration in the Bay Area? Whether it is a milestone birthday, a bachelorette party, or a corporate night out, organizing group transportation can quickly become a logistical headache. Between navigating steep hills, hunting for impossible parking, and dealing with ride-share surge pricing, managing a crowd is tough. Choosing a San Francisco party bus rental solves all of...

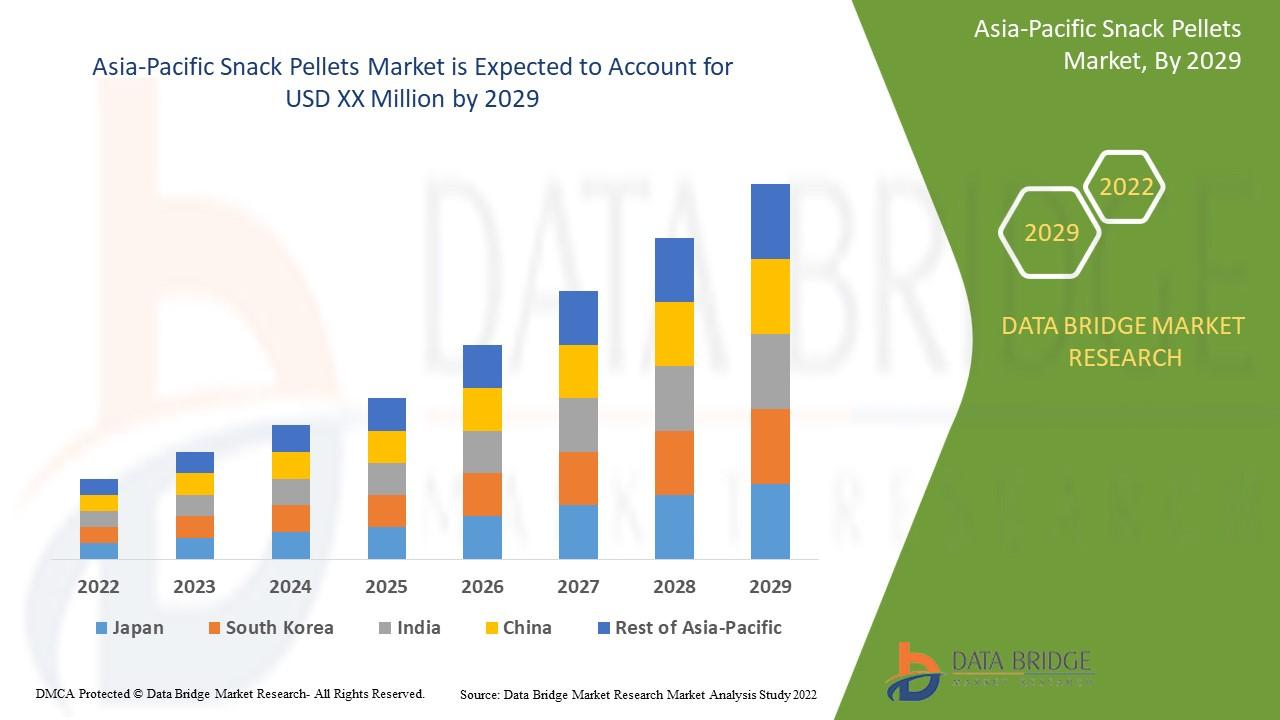

"Executive Summary Asia-Pacific Snack Pellets Market Size and Share Forecast Data Bridge Market Research analyses that the Asia-Pacific snack pellets market will grow at a CAGR of 6.4% during the forecast period of 2022 to 2029. The Asia-Pacific Snack Pellets Market report gives strength to the organization and makes better decisions for steering the business on the right track. A...

In your journey through UIUC student apartments, you'll find a well-thought-out blend of meeting rooms, study spaces, and social events that cater to diverse needs. You can choose between quiet study nooks for focused work or vibrant lounges perfect for group projects. Additionally, engaging social events encourage connections that extend beyond academics. This harmonious balance raises...

In today’s fast-paced world, maintaining a healthy weight has become increasingly challenging. Sedentary lifestyles, processed foods, stress, and inconsistent routines all contribute to weight gain and metabolic imbalance. As a result, many individuals are turning to natural supplements to support their health goals without resorting to extreme diets or exhausting workout plans. One such...