Rubber Processing Chemicals Market Growth to Reach USD 12.5 Billion by 2032

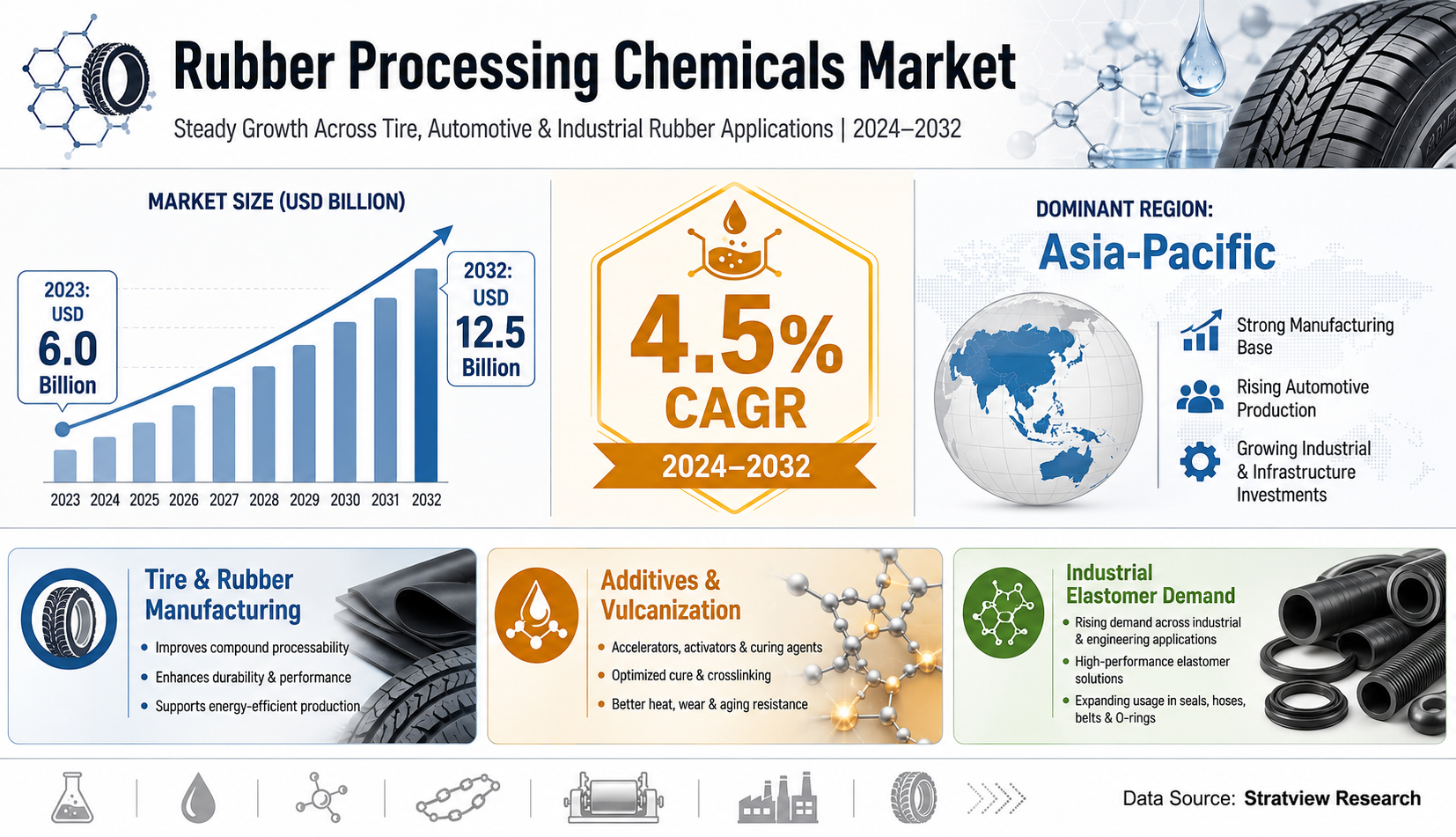

The Rubber Processing Chemicals Market was valued at USD 6.0 billion in 2023 and is projected to reach USD 12.5 billion by 2032. Growth during 2024–2032 is supported by demand for stronger, more durable, and higher-performing rubber products. The Rubber Processing Chemicals Market is expected to grow at a CAGR of 4.5% during 2024–2032.

Demand is increasing because rubber processing chemicals improve physical, chemical, and mechanical characteristics. These additives make rubber more durable, flexible, and resistant to heat, UV rays, ozone, and chemical exposure. That functional value supports demand across automotive, industrial, and consumer goods applications mentioned on the source page.

Request a free sample report:

https://www.stratviewresearch.com/Request-Sample/rubber-processing-chemicals-market#form

The strategic relevance of Rubber Processing Chemicals Market growth lies in its close connection with tire performance and industrial rubber requirements. As manufacturers seek products that last longer and perform better under stress, additives such as anti-degradants and accelerators become important enablers of quality, consistency, and lifecycle value.

Market Segmentation Analysis

The market is segmented by Product Type into Anti-degradants, Accelerators, Flame Retardants, Processing Aids/Promoters, and Others. Anti-degradants are the dominant product type, accounting for over 50% share in 2023. Their dominance reflects their role in preventing oxidative degradation, ozone exposure damage, and environmental stress-related deterioration.

The market is segmented by Application Type into Tire and Non-Tire. The tire application dominates the market because the automotive industry is the largest consumer of rubber processing chemicals. Tires require chemicals that enhance durability, resistance to wear and tear, and performance across terrain conditions.

The market is segmented by Region into North America, Europe, Asia-Pacific, and The Rest of the World. This segmentation enables industry intelligence across key geographic demand clusters. Regional performance is closely linked to automotive manufacturing, tire production, industrial growth, and demand for rubber products.

Regional Market Insights

Asia-Pacific is the largest and fastest-growing market. The region’s leadership is driven by strong demand from automotive and industrial industries. China, India, and Japan have large automotive manufacturing bases, and the region also benefits from the presence of large tire manufacturers.

North America remains a well-established market for rubber processing chemicals. Its demand is supported by automotive and industrial industries seeking sustainable and high-performance rubber chemicals. This reinforces North America’s role as a mature market for durable and environmentally friendly rubber products.

Emerging Trends Shaping the Rubber Processing Chemicals Market

Sustainability-oriented development is becoming an important industry trend. Eastman Chemical Company entered a joint venture with several major tire manufacturers in 2023 to focus on sustainable rubber processing chemicals. The initiative aims to improve environmental performance amid rising regulatory demand for eco-friendly chemicals.

Low-emission manufacturing is also influencing product development. Lanxess launched low-VOC rubber additives in 2023, while SI Group introduced an advanced rubber antioxidant in 2022. These developments highlight how environmental performance and product durability are shaping chemical innovation.

Key Growth Drivers of the Market

- Automotive production raises tire demand, creating direct consumption growth for rubber processing chemicals.

- Tire manufacturers need specialized chemicals to improve durability, wear resistance, and terrain performance.

- Industrial applications require advanced rubber products, supporting demand for additives that improve strength and lifecycle performance.

- Environmental stressors such as heat, UV radiation, ozone, and oxidation increase the importance of anti-degradants.

- Sustainability requirements are pushing chemical suppliers toward low-VOC and eco-friendly product development.

Competitive Landscape

Top Companies in the Market

Akzo Nobel N.V.

Arkema

BASF SE

Behn Meyer

Eastman Chemical Company

KUMHO PETROCHEMICAL

Lanxess

Paul & Company

R.T. Vanderbilt Holding Company, Inc.

Solvay

Conclusion and Strategic Outlook

The Rubber Processing Chemicals Market is set to grow from USD 6.0 billion in 2023 to USD 12.5 billion by 2032, at a CAGR of 4.5% during 2024–2032. The market’s growth analysis shows demand concentrated around tire manufacturing, automotive output, industrial rubber products, and product durability. Future industry strategy will likely center on performance and sustainability.

FAQs – Rubber Processing Chemicals Market

What is the forecast for the Rubber Processing Chemicals Market?

The Rubber Processing Chemicals Market is likely to reach USD 12.5 billion by 2032. It was valued at USD 6.0 billion in 2023.

What CAGR will the Rubber Processing Chemicals Market record?

The Rubber Processing Chemicals Market is expected to grow at a CAGR of 4.5% during 2024–2032. This indicates steady demand across tire and non-tire applications.

Why is demand increasing?

Demand is increasing because rubber processing chemicals improve durability, flexibility, and resistance to environmental factors. Tire manufacturing and industrial rubber products are key demand areas.

Which region is growing fastest?

Asia-Pacific is both the largest and fastest-growing region in the Rubber Processing Chemicals Market. Growth is supported by automotive production, industrial demand, and large tire manufacturing activity.

What should investors monitor?

Investors should monitor tire demand, automotive production, industrial rubber consumption, and sustainability-led product development. These factors shape the long-term market outlook and competitive landscape.

Catégories

Lire la suite

Exactitude Consultancy has just released a new report that dives into the global Liquid fertilizers market. It explores everything from market size and share to demand and forecasts all the way through 2033. By analyzing historical data alongside current trends, the report sheds light on competitive strategies and the key factors driving market growth. Get FREE Sample Copy of this...

Global Automotive Steering Systems Market Advances with Electrification, Safety Innovations, and Precision Driving Technologies Next-Generation Steering Solutions Enhance Vehicle Control, Autonomous Driving Capabilities, and Driver Assistance Systems Across Global Automotive Platforms The Automotive Steering Systems Market is witnessing steady transformation as automotive...

Hos os tilbyder vi en komplet og professionel vaskeservice, der gør hverdagen nemmere for virksomheder i alle brancher. Vi specialiserer os i vask og leje af linned, håndklæder, måtter og meget mere – altid med fokus på kvalitet, hygiejne og fleksible løsninger. Uanset om du driver hotel, restaurant, klinik, fitnesscenter eller...

Crosslinking Agent Market Growth Surges as Industrial and Polymer Applications Expand Globally The Crosslinking Agent Market is witnessing strong growth as industries worldwide continue to adopt advanced materials and polymer solutions. The Crosslinking Agent Market Size was valued at USD 8.86 Billion in 2024 and is expected to reach USD 17.19 Billion by 2032, growing at a CAGR of...

RR88 is a trusted and exciting online gaming platform built for players who enjoy fun, rewards, and smooth gameplay. With the inspiring motto “Bet for fun – Win big,” RR88 focuses on delivering a positive, safe, and enjoyable environment for all users. Whether you are new to online gaming or already experienced, this platform offers something special for everyone. From...