Europe Automotive Composites Market Growth Drivers, Challenges, and Forecast

The Europe Automotive Composites Market is witnessing consistent growth, driven by the rapid structural transformation of the transport sector, stringent regional regulatory mandates regarding vehicle emissions, and the extensive adoption of advanced lightweight materials to boost fuel efficiency and driving range. As European automotive original equipment manufacturers (OEMs) aggressively transition toward electric vehicles (EVs) and sustainable assembly lines, the demand for high-strength, low-density composite alternatives to traditional steel and aluminum is accelerating.

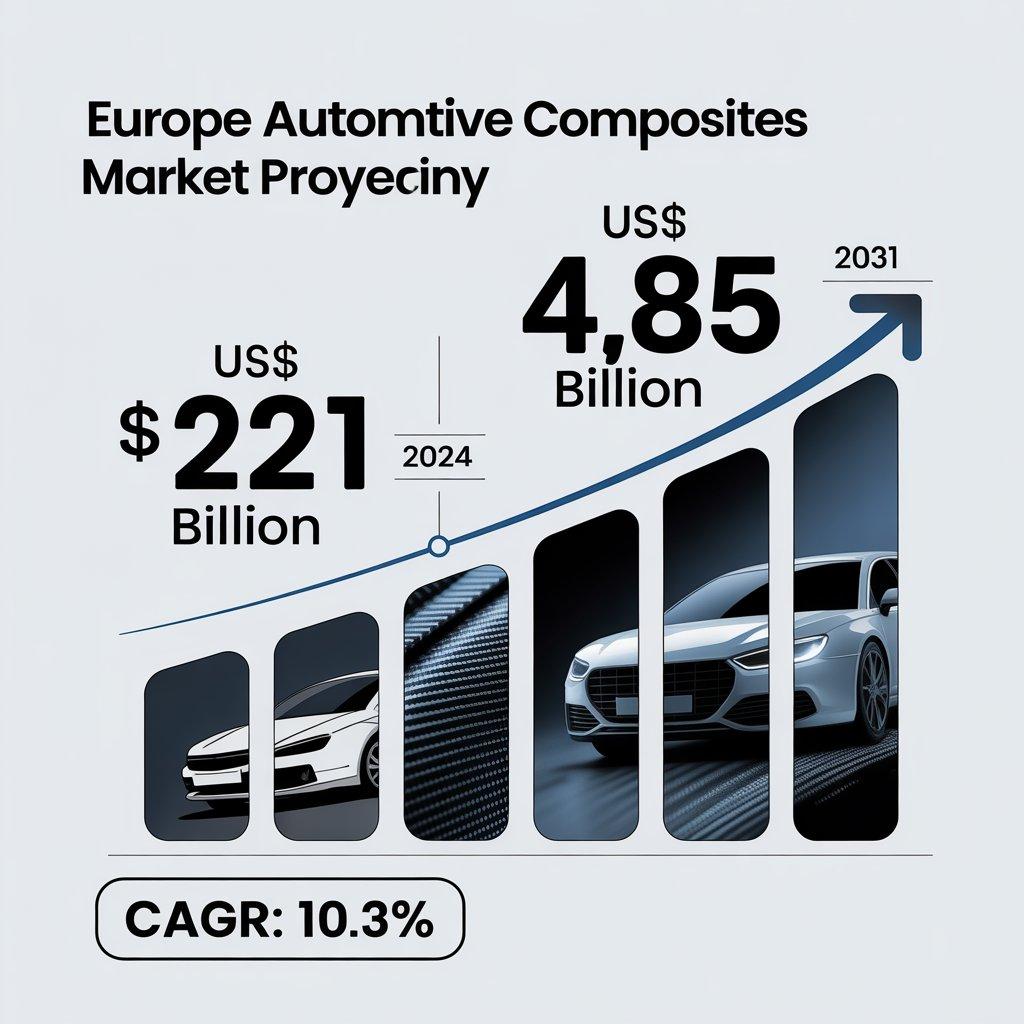

The market was valued at approximately US$ 2.05 billion in 2025 and is projected to reach nearly US$ 2.85 billion by 2033, registering a steady CAGR of 4.2% during the forecast period from 2026 to 2033. The rapid scaling of battery electric vehicle architectures, which require intense weight reduction to compensate for heavy structural battery packs, represents a foundational factor supporting market expansion. As tier-1 suppliers invest in sophisticated high-volume production methods to shorten cycle times, the integration of specialized composites continues to expand across high-performance passenger vehicles and commercial fleets.Understanding Automotive Composites

Automotive composites are highly engineered material systems produced by combining a reinforcing fiber (such as glass, carbon, or natural fibers) with a polymer matrix resin (such as thermoset epoxies or thermoplastics). The resulting synergistic material exhibits mechanical properties far superior to its individual base elements, offering exceptional strength-to-weight ratios, dimensional stability, and structural endurance.

Modern automotive composites are extensively utilized to fabricate complex, multi-functional automotive assemblies that would be difficult or impossible to manufacture using traditional sheet metal stamping. By embedding advanced resin formulations into automated molding workflows, component suppliers can produce unified structural parts that minimize secondary assembly requirements and significantly drop long-term vehicle weight profiles.

Automotive composites are widely used in the manufacture and development of:

- Exterior panels, hoods, roofs, and liftgates for body-in-white (BIW) reduction

- Chassis and structural cross-members requiring high impact energy absorption

- EV battery enclosures, trays, and protective structural covers

- Interior dashboards, trim pieces, door panels, and seat structures

- Under-the-hood components, engine covers, and intake manifolds

Market Drivers

Enforcement of Strict European Union Fleet-Wide CO2 Emission Targets

Automakers face heavy financial penalties if their vehicle portfolios exceed regulatory carbon limits. This structural constraint forces a systematic reliance on advanced vehicle lightweighting strategies, where shedding vehicular mass directly translates to lower fuel consumption and limited tailpipe discharge across internal combustion engines.

Explosive Expansion of the European Electric Vehicle (EV) Ecosystem

Because EV battery arrays add hundreds of kilograms of structural weight to a vehicle's chassis, OEMs must compensate to safeguard driving range per single charge cycle. Utilizing ultra-light, highly rigid composite matrices in structural areas allows manufacturers to maximize battery capacity while keeping total vehicle weight within manageable boundaries.

Structural Shift Toward Rapidly Recyclable Thermoplastic Solutions

Material science advancements are facilitating a major shift from legacy thermoset matrices toward thermoplastic composites. Thermoplastics can be rapidly injection-molded or compression-molded, drastically reducing manufacturing cycle times to align with high-volume assembly lines while simultaneously meeting the EU’s strict end-of-life vehicle (ELV) recyclability directives.

Growing Consumer and Fleet Demand for Enhanced Safety and Crash Protection

Advanced fiber composites display excellent specific energy absorption properties under dynamic impact scenarios compared to traditional metals. This allows engineering teams to design crumple zones and cabin safety cages that protect passengers effectively while significantly reducing the bulk material thickness required.

Market Segmentation

By Fiber Type

- Glass Fiber Composites (Dominant Segment)

- Carbon Fiber Composites

- Natural Fiber & Other Composites

By Resin Type

- Thermoset Composites

- Thermoplastic Composites (Fastest Growing)

By Application

- Exterior Panels & Body Components

- Interior Components & Trims

- Chassis, Powertrain & Structural Components

- Other Specialized Parts

By Manufacturing Process

- Compression Molding

- Injection Molding

- Resin Transfer Molding (RTM)

- Other Specialized Processes

Regional Insights

| Country / Region | Market Dynamic & Development Landscape |

|---|---|

| Germany | Germany commands a dominant position in the European market, sustained by its massive domestic automotive production base, immediate adaptation of premium CFRP engineering by luxury auto groups, and a high density of specialized tier-1 material suppliers. |

| France | France is experiencing steady expansion fueled by active governmental green transportation initiatives and automotive design clusters focused on integrating lightweight natural fibers and bio-resins into urban mobility applications. |

| United Kingdom | The UK exhibits a highly sophisticated premium and motorsport engineering framework, which drives the localized development of high-performance, automated resin transfer molding (RTM) techniques for low-volume, high-value composite parts. |

| Italy | Italy is characterized by robust technology integration across the sports car and high-end passenger vehicle segments, creating a highly specialized, margin-resilient demand market for sophisticated aesthetic and structural carbon composites. |

| Rest of Europe | Comprising nations like Spain, the Czech Republic, and Poland, this segment shows consistent scaling due to the shifting of manufacturing facilities by Western OEMs looking to optimize localized component supply networks. |

Top Players in the Europe Automotive Composites Market

The European market features a highly consolidated and technically demanding competitive field, with major chemical conglomerates, multi-national textilers, and specialized tier-1 auto suppliers driving cross-industry co-development programs.

Some of the major players operating in the market include:

- Toray Industries, Inc.

- SGL Carbon SE

- Solvay S.A.

- Teijin Limited

- Owens Corning

- BASF SE

- Huntsman International LLC

- Hexcel Corporation

- Gurit Holding AG

- Lanxess AG

These primary market entities consistently dedicate substantial capital to R&D for perfecting fast-curing resin formulations, automated tape laying machinery, and closed-loop carbon recycling loops to satisfy stringently regulated automotive manufacturing demands.

Technological Innovations

Manufacturing and chemical advancements are transforming historical component cycle times. High-pressure resin transfer molding (HP-RTM) systems are successfully compressing part cycle numbers down to under two minutes per piece, breaking open the capability to use advanced carbon fiber matrices on mass-production vehicle platforms instead of limiting them to boutique supercars.

Additionally, the commercial integration of bio-based resins combined with hemp or flax natural fibers is gaining strong traction for interior door cards and structural floor linings. These hybrid composites offer comparable stiffness to traditional glass matrices while dramatically lowering the total cradle-to-gate carbon footprint of vehicle assembly plants.

Future Market Outlook

The forward trajectory of the Europe automotive composites market remains exceptionally promising, structurally secured by the irreversible transition of the region’s transport network toward zero-emission powertrains. The continuous evolution of automated multi-material joining tech will allow engineers to cleanly bond composite structures directly onto metal chassis lines without galvanic corrosion risks.

As circular economy principles become deeply embedded within the industrial fabric of the continent, the optimization of mass thermoplastic recycling will dictate long-term market dominance. Companies that introduce cost-effective, high-yield material architectures that satisfy strict automotive durability benchmarks will capture the most significant market share over the coming decade.

Frequently Asked Questions (FAQs)

What is the primary factor accelerating the growth of the Europe automotive composites market?The market expansion is heavily driven by rigid European Union fleet CO2 emission regulations, the need to offset battery weights in electric vehicles, and the continuous push for lightweighting to improve vehicle performance and driving ranges.

Why are thermoplastic composites gaining market share over traditional thermoset alternatives?Thermoplastics can be reheated and remolded rapidly, which allows for vastly shorter manufacturing cycle times suitable for mass-production lines. They also support complete end-of-life recycling, aligning closely with EU circular economy mandates.

Which fiber segment commands the highest demand volume in automotive manufacturing?Glass fiber reinforced polymers (GFRP) dominate the volume market due to their excellent balance of mechanical performance, ease of processing, and highly cost-competitive pricing structures compared to premium carbon configurations.

What major engineering barrier is the industry working to overcome?The primary barrier is reducing the high raw material costs of carbon fiber matrices and optimizing mass production processing speeds to compete effectively with the low cost and mature manufacturing footprints of traditional steel and aluminum stamping lines.

Browse More Reports:

https://www.businessmarketinsights.com/reports/asia-pacific-airway-management-devices-market

https://www.businessmarketinsights.com/reports/gcc-airway-management-devices-market

https://www.businessmarketinsights.com/reports/benelux-self-injection-device-market

About Us

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications.

Contact Us

If you have any questions about this report or would like further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Categorias

Leia Mais

Trải Nghiệm Mượt Mà Tại Hi88: Địa Chỉ Tin Cậy Cho Người Đam Mê Cá CượcTrong thời đại công nghệ số phát triển vượt bậc, việc lựa chọn một nền tảng cá cược trực tuyến đáng tin cậy trở nên ngày càng quan trọng. Hi88 đã nhanh chóng khẳng định vị thế của mình trong lĩnh vực này với những trải nghiệm mượt...

The Change Kheloyar Bets into real wins Imagine putting down Rs100 on Kheloyar, getting an extra bonus, then taking out Rs500 following placing an IPL bet. Does that sound easy? Many newbies lose out on payments and rewards because of hidden rules. Kheloyar (also known as) is the main force behind India's top gaming, with cricket bets as well as casino spins. This guide explains everything from...

"Nanotechnology Market Summary: According to the latest report published by Data Bridge Market Research, the Nanotechnology Market The global nanotechnology market size was valued at USD 14.56 billion in 2024 and is expected to reach USD 227.54 billion by 2032, at a CAGR of 41.00% during the forecast period This Nanotechnology Market research report is a...

The latest business intelligence report released by Polaris Market Research on Automotive Powertrain Systems Market Size, Share, Trends, Industry Analysis Report: By Propulsion Type (Internal Combustion Engine and Electric Vehicle), Vehicles Type, and Region (North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa) – Market Forecast, 2025–2034. It...

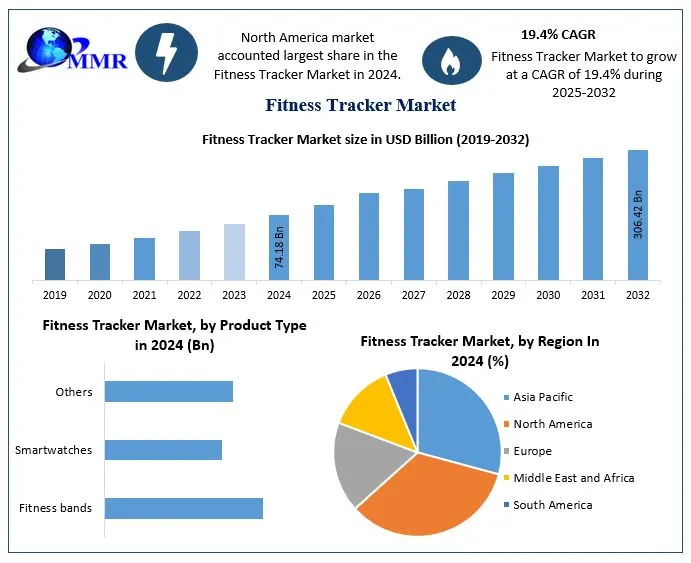

Fitness Tracker Market to Reach USD 306.42 Billion by 2032 at 19.4% CAGR | AI-Driven Healthcare, Digital Health Transformation & Future of Lifesciences Revolution The global Fitness Tracker Market is entering a high-growth transformation era as digital healthcare ecosystems, AI-powered wellness platforms, and preventive healthcare technologies reshape the future of connected...