R448A Refrigerant and the Quiet Rebuild of Cold-Chain Infrastructure: How Supermarkets, Warehouses and Food Logistics Are Repricing Every Degree of Cooling

A supermarket does not announce its refrigeration transition with a ribbon-cutting. It happens behind 80 to 250 display cases, inside 2 to 6 compressor racks, across 500 to 3,000 metres of refrigerant piping, and through thousands of kilograms of food that must stay within a 2°C to 8°C chilled band or a -18°C frozen band every hour of the year. This is where R448A refrigerant has become a working-class transition fluid: not glamorous, not futuristic, but deeply practical for stores and warehouses trying to reduce high-GWP exposure without rebuilding the entire refrigeration plant.

Semple Request At: https://datavagyanik.com/reports/r448a-refrigerant-market-research-insights-market-size-analysis-and-forecast-competitive-landscape-market-share/

The story starts with the old baseline. A mid-sized supermarket using R404A may carry 500 to 1,500 kg of refrigerant charge across racks, condensers, evaporators, valves and long pipe runs. R404A’s GWP is roughly 3,900, while R448A refrigerant sits near the 1,273–1,300 range, cutting climate intensity by about two-thirds at the gas level. In infrastructure language, that means a 1,000 kg installed charge shifts from nearly 3,900 tonnes of CO₂-equivalent exposure to about 1,300 tonnes. The store does not need to sell one extra carton of milk for this math to matter.

The use-case map is narrow but economically heavy. R448A refrigerant is mostly a low- and medium-temperature commercial refrigeration fluid, so its adoption clusters around supermarkets, hypermarkets, cold rooms, food processors, convenience stores, distribution centres and industrial freezing systems. A single convenience store may need only 20 to 80 kg of charge, but a regional cold-storage warehouse can run into 1,000 to 5,000 kg depending on system architecture. That wide charge range explains why adoption is not counted only by number of sites; it is counted by kilograms installed, leakage avoided, service calls completed and compressor energy measured over 8,760 operating hours per year.

The technical attraction of R448A refrigerant is that it fits the retrofit economy. It is an A1, nonflammable zeotropic blend, so owners can often work within existing safety protocols more easily than they can with flammable A2L or natural refrigerant redesigns. Its blend chemistry includes HFC and HFO components, allowing lower GWP than R404A while maintaining the pressure-temperature behaviour needed in legacy systems. In practical terms, a retrofit may involve oil checks, seal inspection, expansion valve adjustment, controller recalibration, filter-drier replacement, leak testing and relabelling rather than a full mechanical-room rebuild.

Every retrofit has a budget story. For a 40,000-square-foot supermarket, a complete natural refrigerant conversion can move into six-figure or even seven-figure capital territory when piping, racks, cases and controls are replaced. By comparison, an R448A refrigerant retrofit is often treated as a service-led capital project: technician labour, refrigerant recovery, replacement gas, tuning, minor components and commissioning. If the installed charge is 800 kg and refrigerant handling plus tuning costs are mapped at even USD 60 to USD 140 per kg equivalent project exposure, the store is looking at USD 48,000 to USD 112,000 before considering downtime, reclaimed gas value or energy changes.

Regulation is the clock behind the story. The EU’s 2024 F-gas revision tightened the HFC phase-down pathway and set the long road toward a 2050 HFC phase-out. In the United States, the refrigerant transition is moving through AIM Act and SNAP-driven restrictions on high-GWP refrigerants in new equipment categories. The timeline matters because R448A refrigerant is not a forever answer for every new installation; it is a bridge for assets with 7 to 20 years of remaining operating life. That is why the strongest demand sits in installed-base management rather than greenfield refrigeration architecture.

According to DataVagyanik, the global R448A refrigerant market is valued at USD 1.18 billion in 2026 and is forecast to reach USD 1.74 billion by 2032, supported by retrofit activity in food retail, cold-chain logistics, industrial refrigeration and service-cylinder demand. DataVagyanik attributes this growth to three quantified forces: more than 35% of legacy commercial refrigeration assets in developed markets still needing lower-GWP transition planning, an estimated 6% to 9% annual increase in supermarket retrofit service spend, and continued replacement of R404A/R507 in medium- and low-temperature applications where owners prefer nonflammable A1 refrigerants over full system redesign.

The infrastructure chain behind R448A refrigerant is larger than a gas cylinder. It starts with fluorochemical production, blending facilities, purity testing, reclaim infrastructure, cylinder filling, wholesale distribution and technician certification. A typical supply chain touches 5 to 8 commercial layers before the refrigerant reaches a store: chemical producer, blender, packager, distributor, HVACR wholesaler, service contractor, equipment owner and compliance auditor. That layered structure is why price changes can arrive faster than physical shortages; one quota change or production constraint can be reflected through distributor inventories within weeks.

Application mapping shows why food retail dominates the narrative. A 60-door supermarket frozen section may consume 30% to 45% of refrigeration load, while chilled cases, meat rooms, bakery rooms and walk-in coolers consume the rest. R448A refrigerant works across both medium-temperature and low-temperature circuits, making it useful where one facility runs multiple evaporating temperatures. In a typical rack system, medium-temperature suction may serve produce, dairy and meat around -6°C to 2°C evaporating conditions, while low-temperature suction supports frozen food and ice cream around -30°C to -35°C. A single refrigerant strategy simplifies technician training and inventory.

Energy is the hidden adoption lever. Manufacturers and field users have reported efficiency improvements versus R404A in many retrofit conditions, but the actual result depends on compressor type, condensing temperature, superheat setting, evaporator condition and controls. Even a 3% reduction in annual refrigeration electricity use is material. A supermarket refrigeration system using 700,000 kWh per year would save 21,000 kWh annually at 3%. At USD 0.12 per kWh, that is USD 2,520 per year; across 500 stores, the same operating logic becomes USD 1.26 million per year.

Cold storage gives R448A refrigerant a different type of relevance. Warehouses do not operate like supermarkets; they prioritize room volume, dock-door recovery, blast-freezing cycles, forklift traffic and inventory turnover. A 100,000-square-foot frozen warehouse may hold tens of millions of dollars of food inventory, and a refrigeration failure can damage more value in 12 hours than the annual refrigerant budget. For these operators, R448A refrigerant is judged less by marketing language and more by compressor discharge temperature, capacity match, glide management, leak rates and service availability within a 24-hour emergency window.

The spending timeline is also becoming clearer. From 2024 onward, European owners accelerated audits because quota pressure made high-GWP refrigerants harder to justify. In 2025 and 2026, U.S. commercial refrigeration buyers face sharper equipment-category decisions as new installations move toward lower-GWP thresholds. By 2027–2030, the installed base becomes the main battleground: not whether natural refrigerants win new flagship projects, but how millions of existing compressors, cases and valves are kept compliant, efficient and serviceable. That is the practical runway for R448A refrigerant.

The manufacturer map is concentrated around global fluorochemical and refrigerant supply ecosystems. Honeywell commercializes Solstice N40 as R448A refrigerant, while distribution and lifecycle support involve reclaim companies, gas handlers and HVACR wholesale networks. The market is not only “who makes the molecule”; it is also who can provide recovery cylinders, reclaimed supply, leak-management support, safety documentation, technician guidance and emergency availability. In refrigerants, a product without a service network is only a chemical; a product with a service network becomes infrastructure.

For food retailers, the business case usually fits into 4 measurable boxes: carbon liability reduction, regulatory continuity, serviceability and asset-life extension. A chain with 300 stores, each carrying 700 kg of old R404A, has 210,000 kg of installed high-GWP refrigerant exposure. Replacing that with R448A refrigerant can reduce theoretical CO₂-equivalent exposure by more than 500,000 tonnes. Even if annual leakage is only 10%, the avoided emissions exposure becomes large enough to appear in sustainability reporting, insurance discussions and maintenance budgeting.

The story is therefore not about one gas replacing another gas. R448A refrigerant is a bridge between old refrigeration infrastructure and the next generation of lower-GWP cooling. It lets a supermarket avoid premature asset scrapping, helps a warehouse reduce compliance risk, gives contractors a familiar A1 service pathway, and buys time while CO₂, ammonia, hydrocarbons and A2L architectures scale in the right places. In an industry where one degree of temperature abuse can spoil a pallet and one leak can trigger a compliance event, that bridge has measurable value.

From Refrigerant Cylinders to Retail Uptime: The Service Infrastructure Deciding Real Adoption

The real infrastructure behind this transition is not only inside the compressor room. It is in the contractor’s van, the distributor’s warehouse, the reclaim cylinder, the recovery machine, the gas analyser and the service logbook. A supermarket may decide the retrofit in a boardroom, but the actual conversion happens in 8 to 20 working hours per rack, with 2 to 5 trained technicians, multiple pressure checks, refrigerant recovery, evacuation, charging and performance validation. This is why the adoption of R448A refrigerant is tied directly to the maturity of the HVACR service ecosystem.

A technician-led retrofit has a measurable sequence. First, the existing R404A or R507 charge is recovered and weighed. Second, the system is checked for oil compatibility, elastomer condition, filter-drier condition and expansion valve suitability. Third, the system is evacuated to remove moisture and non-condensables. Fourth, the replacement charge is introduced, usually at a controlled percentage of the original charge, followed by superheat and subcooling adjustment. Fifth, operating performance is logged over multiple load conditions. A 1,000 kg supermarket system can easily generate 40 to 80 data points during commissioning if suction pressure, discharge pressure, evaporator temperature, case temperature, compressor amps and ambient conditions are properly recorded.

This is also why wholesale distribution matters. In commercial refrigeration, a refrigerant shortage is not theoretical; it can shut down a meat room, a dairy aisle or a frozen-food line. A regional distributor serving 300 to 800 contractors may hold dozens of cylinder sizes, from small service cylinders to larger recovery and refill containers. When high-GWP refrigerants become more expensive or restricted, contractors shift their stocking pattern. They carry fewer emergency R404A cylinders and more retrofit-compatible alternatives. That inventory reshuffling is one of the quiet signals showing that R448A refrigerant is becoming part of the working supply chain rather than remaining a specification-sheet option.

The use-case economics become sharper at chain scale. A single store may save only a few thousand dollars per year from better energy performance, but a 1,000-store food retail chain operates like a distributed refrigeration utility. If each store has 500,000 to 900,000 kWh of annual refrigeration electricity demand, the chain’s refrigeration load can exceed 500 million kWh per year. A 2% efficiency improvement across that installed base equals 10 million kWh. At USD 0.10 to USD 0.15 per kWh, that is USD 1 million to USD 1.5 million in annual electricity impact before refrigerant leakage, compliance cost and avoided emergency conversion are even counted.

There is also a risk-cost dimension. Refrigerant leaks are expensive because they combine direct gas replacement cost, labour cost, lost cooling capacity and compliance exposure. A system with a 1,000 kg charge and a 12% annual leak rate loses 120 kg per year. If the replacement gas and handling cost is valued at USD 70 to USD 130 per kg, leakage alone becomes USD 8,400 to USD 15,600 per year. For 200 similar sites, the leakage bill becomes USD 1.68 million to USD 3.12 million annually. In that context, a lower-GWP retrofit is not a sustainability ornament; it is a risk-control action.

The food waste calculation is even larger. A refrigerated supermarket can hold USD 250,000 to USD 1 million of perishable inventory depending on format, location and sales density. A cold-storage warehouse can hold USD 5 million to USD 50 million in frozen or chilled goods. If refrigeration instability damages even 2% of a USD 10 million inventory position, the loss is USD 200,000. This is why operators do not adopt new fluids simply because regulation says so. They need pressure stability, predictable capacity and fast emergency support. R448A refrigerant gains relevance where it offers a lower-GWP route without forcing owners to accept unfamiliar operating risk.

Technical discipline is especially important because this refrigerant has temperature glide. That means evaporating and condensing behaviour must be interpreted correctly using dew point and bubble point values. In field terms, a technician cannot treat the pressure-temperature chart casually. Case temperature, evaporator performance and expansion valve settings must be tuned with glide in mind. In a 30-case frozen-food circuit, a small error in superheat adjustment can affect frost pattern, compressor return temperature and product temperature consistency. The infrastructure story is therefore also a training story: the market expands only as the technician base becomes comfortable with blend behaviour.

Application mapping shows three strong adoption clusters. The first is food retail retrofit, where the installed base is large and R404A exposure is still visible. The second is cold-chain logistics, where warehouses need long operating life and high uptime. The third is food processing, where refrigeration supports production lines, blast chillers, storage rooms and packaging zones. A poultry processor, for example, may depend on chilling capacity at multiple points: carcass chilling, portioning rooms, packed-product storage and dispatch docks. When each zone has a different load profile, refrigerant performance must be judged across the full production day, not one laboratory condition.

Investment also flows into tools around the refrigerant, not only the refrigerant itself. Leak detection systems, cloud-connected controllers, electronic expansion valves, compressor monitoring, reclaimed refrigerant handling and automated compliance reporting all become part of the retrofit ecosystem. A multi-store chain may spend USD 2,000 to USD 10,000 per site on upgraded leak detection and controls, depending on layout and system age. Across 500 sites, that becomes USD 1 million to USD 5 million of supporting infrastructure. This spend is not always recorded as refrigerant-market revenue, but it directly enables refrigerant transition.

The strongest commercial argument is asset-life extension. Refrigeration systems are capital-intensive assets with long depreciation windows. If a rack system has 8 to 12 years of useful life remaining, full replacement can destroy remaining asset value. A retrofit using R448A refrigerant can preserve compressors, condensers, cases and much of the piping network while reducing GWP exposure. That makes it attractive for stores that are profitable but not scheduled for full refurbishment. In retail economics, the best upgrade is often the one that avoids both regulatory risk and unnecessary capex.

Regional behaviour differs. Europe moves under tighter F-gas pressure, so adoption is more closely linked to quota economics and the shrinking acceptability of high-GWP service gases. North America has a large supermarket installed base and strong contractor infrastructure, making retrofit execution more scalable. Asia Pacific is mixed: Japan and Australia show more structured transition behaviour, while parts of Southeast Asia and India still balance cost, service availability and equipment age. In emerging markets, R448A refrigerant adoption is likely to concentrate first in multinational retail chains, premium cold storage, export-oriented food processors and facilities linked to global compliance standards.

Pricing behaviour is shaped by quota, production economics, cylinder logistics and reclaim availability. Refrigerants are not priced like commodity gases because regulation can change supply value overnight. A distributor may see different pricing between virgin gas, reclaimed gas and emergency service supply. For end users, the relevant price is not only the cylinder price; it is the installed cost per kilogram after recovery, labour, leak repair, system tuning and downtime. That is why a USD-per-kg comparison can be misleading unless it is attached to system-level cost.

The 2026–2032 story will not be a straight-line replacement story. New systems in many advanced markets will increasingly favour CO₂, ammonia, hydrocarbons and lower-GWP A2L options depending on application. However, the installed base remains huge, and installed infrastructure always changes more slowly than policy documents. Millions of valves, compressors, evaporators and cases cannot be replaced in one regulatory cycle. That time gap is the commercial space where R448A refrigerant continues to operate.

For a medium-format retailer, the decision can be reduced to one operating question: how do we keep the store cold, compliant and financially rational for the next decade? If the answer requires lower GWP, familiar safety classification, manageable retrofit cost and service-network availability, the case becomes practical. Not perfect. Not permanent. Practical. In refrigeration, practical technologies often win because food cannot wait for ideal infrastructure.

The deeper theme is that cooling is now part of climate infrastructure. Every supermarket aisle, every frozen warehouse, every food-processing cold room and every last-mile cold-chain node is being pulled into carbon accounting. Refrigerant choice is no longer a back-office engineering detail; it affects emissions reporting, maintenance budgets, energy planning, insurance risk, capex timing and brand credibility. That is why the shift toward R448A refrigerant should be read as a transition story, not just a product story.

The old refrigeration economy was built around capacity: keep the box cold. The new refrigeration economy is built around measured capacity: keep the box cold with lower GWP, lower leakage, lower energy waste, better monitoring and documented compliance. The companies that understand this will not treat refrigerant conversion as a one-time gas swap. They will treat it as a cold-chain infrastructure upgrade measured in kilograms, kilowatt-hours, leak rates, service hours and avoided spoilage. That is the real quantification behind the market.

Semple Request At: https://datavagyanik.com/reports/r448a-refrigerant-market-research-insights-market-size-analysis-and-forecast-competitive-landscape-market-share/

Categorie

Leggi tutto

Choosing the right watch today is about more than telling time. It reflects personal style, craftsmanship, and long-term value. From luxury collectors to everyday buyers, the demand for well-made timepieces continues to grow. Understanding the difference between quality and hype is essential for making a confident purchase. Branded Watches are known for their reliability, design...

The world is changing quickly, and students today need more than traditional classroom knowledge to succeed in the future. Many families are now exploring online stem courses because they help children develop valuable skills in science, technology, engineering, and mathematics from the comfort of home. These programs are designed to make learning practical, engaging, and relevant to modern...

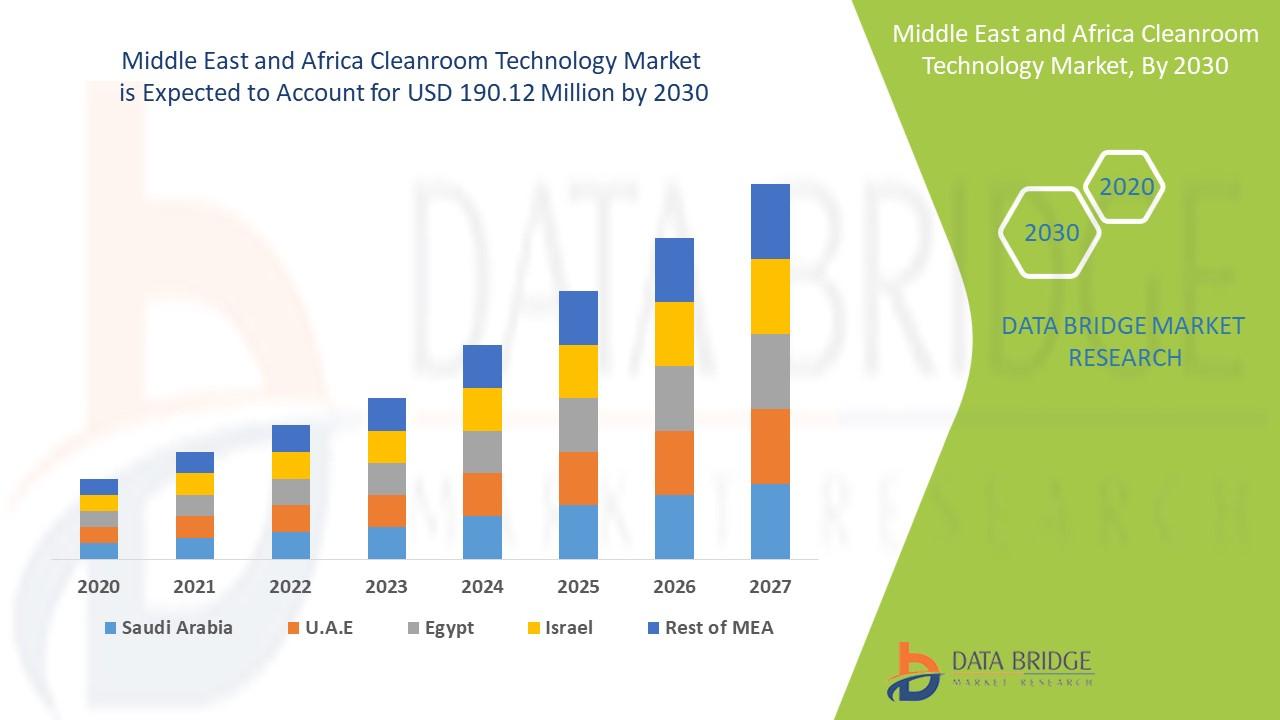

"Latest Insights on Executive Summary Middle East and Africa Cleanroom Technology Market Share and Size Cleanroom technology market is expected to gain market growth in the forecast period of 2020 to 2030. Data Bridge Market Research analyses that the market is growing with a CAGR of 3.9% in the forecast period of 2020 to 2030 and is expected to reach USD 190.12 million by 2030 from...

UFABRO hadir sebagai domain digital modern yang mendukung pengalaman akses cepat dan navigasi praktis untuk pengguna yang tertarik dengan berbagai strategi taruhan online, termasuk sistem 1x2 parlay yang semakin populer di kalangan pecinta analisis pertandingan. Dengan desain yang sederhana, performa responsif, dan struktur konten yang tertata rapi, UFABRO memberikan kenyamanan bagi pengguna...

What if the next breakthrough in your industry is already mapped out—and your competitors are quietly acting on it while you hesitate? In today’s hyper-competitive innovation race, waiting even a few weeks can mean the difference between market leadership and missed opportunity. That’s exactly why a landscape analysis patent strategy is no longer optional—it’s...