Molded Rubber Bellows: The Hidden Flex Infrastructure Protecting Machines, Vehicles, Robots and Moving Equipment in a $1 Trillion Mechanical Economy

A factory robot arm may look metallic from a distance, but its reliability often depends on a flexible black component that rarely appears in investment headlines. Molded Rubber Bellows sit between motion and contamination. They stretch, compress, fold, seal and recover thousands of times without becoming the main character of the machine. In a CNC machine, they protect guideways from coolant and metal chips. In a steering system, they protect joints from dust and road spray. In industrial actuators, they absorb motion while keeping grease inside and abrasive particles outside.

Semple Request At: https://datavagyanik.com/reports/global-molded-rubber-bellows-market/

The infrastructure behind Molded Rubber Bellows is not small. A single passenger vehicle can use 4 to 8 protective bellows across steering, suspension, gear-shift, braking and wiring protection points. With global car production crossing tens of millions of units annually, even a conservative 4-piece usage rate creates a 300 million-plus unit automotive consumption pool every year. That is before counting trucks, tractors, excavators, two-wheelers, industrial robots, medical tables, railway couplings, pump assemblies and marine equipment.

The story of Molded Rubber Bellows is therefore a story of movement. Every economy is adding more controlled motion. A warehouse adds automated conveyors. A hospital adds height-adjustable equipment. A farm adds hydraulic loaders. A port adds crane spreaders. A semiconductor fab adds precision linear stages. A metro system adds door actuators and vibration-isolated assemblies. Each of these assets needs protection at the exact point where rigid engineering fails: the joint, the slide, the rod, the cable exit, the steering rack, the shaft cover and the telescopic lift column.

The use case map starts with vehicles because automotive gives the biggest volume base. In a mid-size car, a steering rack boot may weigh 80 to 150 grams, a suspension dust boot 30 to 80 grams, a gear linkage boot 50 to 120 grams and a pedal or cable protection boot 20 to 60 grams. At 4 to 8 pieces per vehicle, rubber consumption per vehicle can range from 250 grams to more than 900 grams depending on design. For a 1 million vehicle production program, that converts into 4 million to 8 million individual bellows and roughly 250 to 900 metric tons of formulated rubber demand.

This is why Molded Rubber Bellows behave differently from ordinary rubber parts. They are not sold only by weight. They are sold by failure avoidance. If a steering boot costing less than 2 dollars fails early, the repair exposure can move to a 150 to 500 dollar steering or suspension service event. If a machine-tool way-cover bellows fails, the cost is not just a rubber replacement; it is coolant ingress, guideway scoring, alignment drift and downtime. For a machining cell producing 100 to 300 parts per shift, one day of avoidable downtime can erase the cost of hundreds of bellows.

The technical infrastructure is built around compression molding, transfer molding and injection molding. A small boot may be made in a multi-cavity mold producing 8, 16 or 32 pieces per cycle, while large industrial bellows may be made in single-cavity or two-cavity tools because the geometry is deeper, the wall thickness is heavier and the demolding risk is higher. Typical cycle times can range from 2 to 6 minutes for small automotive boots and 8 to 20 minutes for heavy industrial bellows, depending on rubber compound, wall thickness and curing profile.

The material choice decides the use case. EPDM dominates outdoor weather, water, ozone and brake-fluid-adjacent applications. NBR is used where oil and grease resistance matter. CR is selected when moderate oil, weathering and mechanical toughness must be balanced. Silicone appears where temperature flexibility is more important than abrasion strength. Natural rubber still appears in vibration-heavy or cost-sensitive industrial cases. For Molded Rubber Bellows used near engines, hydraulic cylinders or chemical splash zones, the compound decision can change the service life from 6 months to 5 years.

The market is also shaped by tooling economics. A simple small automotive bellows mold may cost 5,000 to 20,000 dollars, while a complex multi-cavity precision mold can move above 50,000 dollars. For a vehicle platform requiring 5 million units over its life, tooling cost becomes almost invisible at less than 1 cent per part. For a low-volume railway or marine application requiring 2,000 to 10,000 pieces per year, tooling cost can represent 5% to 20% of the landed component economics unless the buyer standardizes dimensions. That is why catalog bellows survive strongly in industrial aftermarket channels.

According to DataVagyanik, the Molded Rubber Bellows market size is estimated at USD 1,184.6 million in 2026 and is forecast to reach USD 1,742.9 million by 2032, expanding at a CAGR of 6.65% between 2026 and 2032. The forecast is supported by three measurable demand layers: rising vehicle platform complexity, factory automation growth and replacement demand from installed industrial equipment. Automotive accounts for the largest unit consumption, but industrial automation and machinery applications are expected to add higher-value growth because custom geometry, chemical resistance and low-volume engineering raise average selling prices.

Factory automation gives the next major storyline. Global robot installations recently moved above half a million units annually, and each robot cell includes more than the robot arm. It includes linear slides, cable tracks, pneumatic grippers, actuator rods, vacuum lines, end-effectors and safety shutters. A single automated cell can contain 5 to 20 flexible protection points. Even if only 2 to 5 of those use Molded Rubber Bellows, a 10,000-cell automation expansion creates 20,000 to 50,000 incremental bellows demand in installation alone, followed by replacement cycles every 2 to 5 years depending on heat, oil mist and stroke frequency.

Construction equipment adds a harsher infrastructure layer. Excavators, wheel loaders, backhoe loaders, graders and compactors expose rods, joints and linkages to mud, grit, stones, hydraulic oil and ultraviolet radiation. A medium excavator can contain 6 to 15 rubber protection boots and bellows across joystick controls, hydraulic rod protection, articulation points, cabin interfaces and electrical pass-throughs. In an equipment fleet of 100,000 machines, that means 600,000 to 1.5 million flexible protective components installed in the field, with aftermarket replacement driven by abrasion rather than product redesign.

The timeline matters because spending is shifting from pure new build to protection of uptime. From 2024 onward, high interest rates slowed parts of construction equipment purchasing in Europe and North America, but infrastructure maintenance, mining replacement and public works continued to support spare parts. In India, equipment sales volatility in FY26 showed that project execution can pause, but the installed fleet still requires service. This is favorable for Molded Rubber Bellows because replacement demand does not stop when machine purchases soften. A loader parked for two months may still need cracked boots replaced before redeployment.

There is another quiet growth engine: electrification. Electric vehicles reduce some engine-bay rubber components, but they add thermal management lines, battery pack interfaces, charging-port protection, cable protection and precision actuator shielding. In steering and suspension, the need for dust and water exclusion does not disappear. In fact, electric platforms often demand lower noise, lower vibration and better sealing because cabin quietness makes minor mechanical defects more noticeable. Molded Rubber Bellows used in EV-adjacent systems therefore move toward tighter dimensional control, cleaner compounds and better fatigue resistance.

The manufacturing map is fragmented but technically disciplined. Large rubber component producers serve OEM platforms through validation cycles that can run 12 to 36 months. Smaller specialists serve industrial machinery, rail, marine, medical and replacement channels with faster customization. The difference is qualification burden. Automotive suppliers must prove ozone resistance, heat aging, compression set, salt spray exposure, flex fatigue and dimensional repeatability. Industrial buyers focus more on stroke length, fold geometry, wall thickness, tear resistance and chemical compatibility. One product family may require 10 to 30 compound variations to serve different operating environments.

A Molded Rubber Bellows design begins with geometry, not rubber. Engineers calculate compressed length, extended length, stroke frequency, fold depth, root radius and clamp-zone thickness. If the fold is too sharp, it cracks. If the wall is too thick, it resists motion and overloads the joint. If the wall is too thin, it tears during installation. A bellows with 5 folds may suit a short steering motion, while a 12-fold design may protect a long actuator stroke. This is why the same outer diameter can sell at three different price points depending on stroke requirement and fatigue rating.

The price architecture can be quantified by channel. Small high-volume automotive Molded Rubber Bellows may sell into OEM supply chains at 0.40 to 2.50 dollars per piece depending on size and material. Industrial catalog parts can range from 5 to 60 dollars. Custom large bellows for machinery, rail or marine applications can cross 100 dollars when tooling amortization, low-volume curing and inspection are included. The value jump is not because rubber becomes expensive; it is because engineering, validation and downtime protection become part of the invoice.

The Infrastructure Layer Behind Molded Rubber Bellows: Tooling, Compounding, Testing and Aftermarket Replacement

The infrastructure that supports Molded Rubber Bellows begins far upstream from the visible part. Carbon black, process oil, synthetic rubber, sulfur, accelerators, plasticizers, anti-ozonants and release agents define the performance envelope before the mold closes. In a typical 100-kilogram rubber batch, the base polymer may represent 35 to 55 kilograms, fillers 25 to 45 kilograms, oil and plasticizer 5 to 15 kilograms and curatives or additives 2 to 8 kilograms. A 3% change in filler loading can shift hardness, tear strength and flex life enough to decide whether the bellows survives 50,000 cycles or 500,000 cycles.

Mixing infrastructure is therefore critical. A rubber processor making Molded Rubber Bellows for automotive and industrial users usually needs internal mixers, two-roll mills, preforming equipment, compression or injection presses, trimming stations, post-curing ovens and inspection benches. A mid-sized plant with 20 to 40 molding presses can produce thousands to hundreds of thousands of bellows per day depending on cavity count and part size. If each press runs 18 hours per day, 25 days per month, and a 16-cavity mold completes one cycle every 4 minutes, one press can theoretically produce about 108,000 small parts per month before downtime, rejects and changeovers.

Actual output is lower because rubber molding has practical losses. Mold cleaning, compound changeover, flash trimming, inspection, trial shots and curing variation can reduce usable press time by 15% to 35%. For a facility targeting 1 million small bellows per month, the effective planning base is not nameplate press capacity; it is validated good-part output. If reject rates rise from 2% to 7%, a 1 million-piece order requires an additional 50,000 molded pieces just to maintain shipment quantity. In automotive programs, that difference can disrupt assembly schedules because rubber parts are usually delivered on just-in-time terms.

Application mapping shows four demand clusters. The first cluster is mobility: passenger cars, commercial vehicles, two-wheelers, tractors and off-highway equipment. This cluster consumes the highest number of Molded Rubber Bellows because each vehicle platform repeats similar sealing points across millions of units. The second cluster is industrial motion: CNC machines, hydraulic presses, packaging machines, textile machinery, robots and conveyors. This cluster consumes fewer units but pays more per part. The third cluster is infrastructure equipment: rail couplings, metro doors, crane systems, marine linkages and power plant actuators. The fourth cluster is precision and controlled environments: medical devices, laboratory automation, semiconductor tools and optical equipment.

Each cluster has its own replacement logic. Automotive OEM demand follows production volume. Automotive aftermarket follows vehicle parc age, road condition and service frequency. Industrial machinery follows operating hours. Construction equipment follows terrain and abrasion. Rail and marine follow scheduled maintenance. A steering boot may be replaced after 5 to 10 years, but a bellows on a dusty actuator in a cement plant may fail in 12 to 24 months. A clean indoor medical device bellows may last 7 to 12 years because it avoids oil, ozone, gravel and ultraviolet exposure.

The spend-size trend is visible through end-user capital expenditure. When automotive OEMs invest in new platforms, bellows suppliers receive tool-development work 18 to 30 months before peak production. When warehouse operators invest in automation, bellows demand rises through actuators, grippers and guided mechanisms. When governments fund railway or metro extensions, protective components appear in braking, suspension, doors and couplings. When mining or construction fleets expand, aftermarket bellows demand follows within the first service cycle. A single 1,000-machine construction fleet can generate 6,000 to 15,000 installed rubber protection points and 1,500 to 5,000 annual replacement opportunities depending on working conditions.

This is why Molded Rubber Bellows should be viewed as a maintenance insurance product. A bellows costing 10 dollars can protect a 300-dollar rod seal assembly, a 1,000-dollar actuator or a 20,000-dollar precision slide. In a packaging line running 120 packs per minute, one hour of stoppage can affect 7,200 packs. If gross contribution is even 3 cents per pack, the lost contribution is 216 dollars per hour before labor, restart waste and missed dispatch schedules. That is why industrial buyers often pay 2x to 5x more for a proven bellows rather than switch to an unvalidated cheaper part.

Technical qualification is increasingly measurable. For automotive-grade Molded Rubber Bellows, ozone resistance may be tested at fixed strain under elevated ozone concentration, heat aging may be assessed at 70°C to 125°C depending on application, and flex-fatigue testing may run thousands to millions of cycles. Dimensional control is checked at clamp seats, inner diameter, outer diameter and fold symmetry. For oil-contact applications, volume swell and hardness change after immersion decide whether NBR, HNBR, CR or FKM-type compounds are justified. A 10% swell may be acceptable in some low-risk covers, but unacceptable in precision clamped assemblies.

The mold design itself has quantifiable economics. For a 12-cavity automotive bellows mold costing 36,000 dollars, tooling amortization over 3 million parts is only 1.2 cents per part. Over 300,000 parts, it becomes 12 cents per part. Over 30,000 parts, it becomes 1.20 dollars per part. This explains why the same geometry can be viable in automotive but expensive in industrial custom channels. It also explains why distributors stock standard cylindrical, conical, square and telescopic bellows in common sizes. Standardization spreads mold cost across many customers instead of one buyer.

Regional manufacturing logic follows customer density. Asia has the strongest volume advantage because automotive, two-wheeler, industrial machinery and electronics assembly supply chains are concentrated in China, India, Japan, South Korea, Thailand, Vietnam and Indonesia. Europe has a strong engineering base because of automotive systems, rail, machinery and premium industrial equipment. North America has demand strength in trucks, off-highway equipment, aerospace-adjacent motion systems, medical devices and industrial automation. Latin America and the Middle East rely more heavily on vehicle replacement, mining, oilfield equipment, construction fleets and imported machinery spares.

In India, the story is especially interesting because three demand channels are expanding together: vehicle production, infrastructure equipment and domestic machinery manufacturing. A two-wheeler may use fewer bellows than a passenger car, but India’s two-wheeler scale creates large unit demand for fork boots, cable boots, dust covers and small flexible protectors. A tractor or backhoe loader uses heavier rubber protection parts and faces harsher soil exposure. If a domestic supplier captures both high-volume two-wheeler programs and industrial replacement parts, the same press shop can balance volume stability with higher-margin custom work.

China’s role is different. It combines large automotive output, industrial robot deployment, machinery exports and a vast rubber component supplier base. Chinese manufacturers can scale Molded Rubber Bellows using multi-cavity molds, rapid tooling and export distribution. However, export customers increasingly demand compound traceability, RoHS or REACH compliance where applicable, stable hardness, low odor, clean trimming and consistent packaging. Low price alone is less decisive when the bellows goes into medical, electronics, rail or premium machinery equipment.

Europe pushes the market toward performance and sustainability. OEMs ask for longer service intervals, lower scrap, better documentation and compliance with restricted-substance rules. A European machinery builder may buy only 20,000 bellows per year, but it may require drawings, material declarations, batch certification and repeatable performance across 5 to 10 years of spare-part supply. This creates a premium niche where Molded Rubber Bellows are not commodity parts; they are engineered protection elements built into machine lifetime guarantees.

North America adds another angle: aftermarket and rugged equipment. Pickup trucks, agricultural machines, mining vehicles, oilfield tools and industrial maintenance channels create demand for replacement bellows in harsh environments. A fleet operator replacing 200 hydraulic cylinder boots per year may care less about unit price and more about field failure frequency. If a 25-dollar upgraded boot reduces replacement labor by two service calls per machine annually, the economic gain can be hundreds of dollars per asset.

The sustainability story is also becoming quantifiable. Rubber molding generates flash waste, rejected parts and end-of-life disposal challenges. If a plant produces 10 million small bellows per year at an average part weight of 70 grams, annual molded output equals 700 metric tons. A 5% scrap and flash rate creates 35 metric tons of rubber waste. Reducing scrap to 3% saves 14 metric tons annually. At a compounded rubber cost of 2.50 to 5.00 dollars per kilogram, that equals 35,000 to 70,000 dollars in direct material savings, before labor and disposal.

For buyers, the practical adoption question is not whether Molded Rubber Bellows are needed. It is where they must be upgraded. The highest return comes from high-stroke, high-contamination and high-downtime locations. A bellows protecting a rarely used indoor linkage can be standard EPDM. A bellows protecting a hydraulic rod in mining dust may need thicker walls, better tear resistance and oil-resistant formulation. A bellows in a medical device may need clean appearance, low odor and smooth surface finish. A bellows in a machine tool may need coolant resistance and chip-deflection geometry.

The future growth theme is modular motion protection. As machines become more compact, bellows must fit tighter spaces. As robots become faster, they must flex more frequently. As vehicles become quieter, they must reduce vibration and squeak risk. As factories become data-driven, maintenance teams will replace protective components before failure rather than after failure. This turns Molded Rubber Bellows from passive covers into planned maintenance items.

By 2032, the winning suppliers will not be the ones with only rubber presses. They will be the ones with compound libraries, fatigue-testing capability, quick tooling, dimensional scanning, application engineering and replacement-channel reach. The product may still look like a folded rubber sleeve, but the business behind it will look like precision infrastructure: chemistry, tooling, validation, logistics and installed-base intelligence working together.

That is why Molded Rubber Bellows deserve a larger industrial story. They are not glamorous. They do not appear in annual budget speeches. They rarely get mentioned in automation investment announcements. Yet they sit exactly where motion meets risk. Every fold is a small mechanical compromise between flexibility and protection. Every replacement is a calculation between part cost and downtime. Every new machine, vehicle, actuator, robot and rail system adds another protected joint. In that sense, the global growth of Molded Rubber Bellows is not just a rubber story; it is the measurable expansion of protected motion across the modern economy.

Semple Request At: https://datavagyanik.com/reports/global-molded-rubber-bellows-market/

Категории

Больше

Cloud Computing Market Overview The Cloud Computing Market is expanding rapidly as organizations adopt enterprise cloud solutions to improve efficiency, scalability, and innovation. Cloud computing has become a core part of digital transformation strategies across industries. According to industry estimates, the market is expected to grow from around USD 1,074.65...

"Executive Summary Ready to Drink (RTD) Mocktails Market Size and Share Forecast The global ready to drink (RTD) mocktails market was valued at USD 6.54 million in 2024 and is expected to reach USD 13.61 billion by 2032 The Ready to Drink (RTD) Mocktails Market report gives strength to the organization and makes better decisions for steering the business on the right...

Skating into Hearts: Netflix's Upcoming Ice Drama "Finding Her Edge" Netflix continues to expand its diverse content lineup with a thrilling new addition for fans of competitive sports dramas. "Finding Her Edge," an adaptation of Jennifer Iacopelli's beloved novel, is set to grace our screens in January 2026, promising to deliver a perfect blend of athletic ambition, teenage emotions, and...

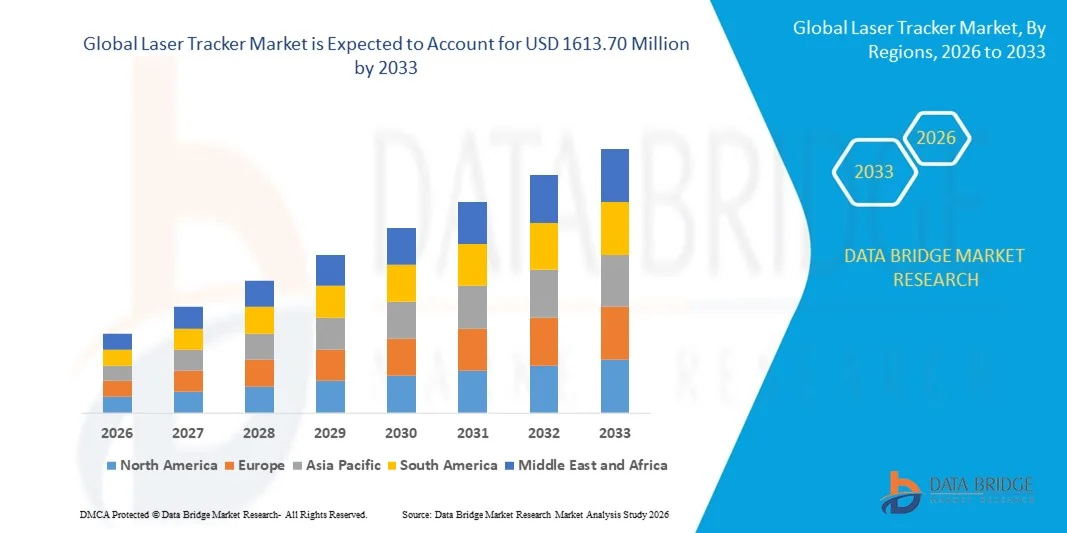

"Laser Tracker Market Summary: According to the latest report published by Data Bridge Market Research, the Laser Tracker Market The global laser tracker market size was valued at USD 647.10 million in 2025 and is expected to reach USD 1613.70 million by 2033, at a CAGR of12.10% during the forecast period An excellent Laser Tracker Market research report...

From smartphones and laptops to medical devices and power tools, lithium-ion batteries are the silent heartbeat of modern portable technology. The relentless pursuit of thinner, lighter, and more powerful devices has forced battery engineers to push the limits of volumetric energy density. Consumers now expect their electronics to last through a full day of heavy use, requiring sophisticated...