Primary vs Secondary Insurance: Which Plan Pays First?

When a patient has two active health insurance plans, one of the first questions is: which plan pays first? The answer depends on the relationship between the patient and each insurance policy. This is known as coordination of benefits, or COB.

Understanding primary and secondary insurance is important for both patients and providers. If the wrong plan is billed first, the claim may be denied, delayed, or sent back for correction. That can affect patient balances, provider payments, and the entire billing process.

What Is Primary Insurance?

Primary insurance is the health plan that processes and pays a claim first. It reviews the service, checks the patient’s benefits, applies the plan rules, and decides how much it will pay.

The primary insurance does not always pay the full amount. It may apply a deductible, copay, coinsurance, or coverage limit. Once the primary plan processes the claim, it sends an explanation of benefits, usually called an EOB. This EOB shows what was billed, what was allowed, what was paid, and what may remain.

The remaining balance may then be submitted to the secondary insurance, if the patient has one.

What Is Secondary Insurance?

Secondary insurance is the plan that reviews the claim after the primary insurance has completed its part. It may help cover some of the remaining eligible balance.

This does not mean the secondary plan automatically pays everything left over. It still applies its own rules. It may cover part of the deductible, coinsurance, or copay, but only if the service is covered under that plan.

The secondary plan usually needs the primary EOB before it can process the claim. Without that EOB, the secondary claim may be rejected or delayed.

How Do Insurance Plans Decide Which Pays First?

Insurance companies use coordination of benefits rules to decide which plan is primary and which plan is secondary. Patients usually cannot choose the order.

The order depends on how the patient is covered under each plan. For example, if a person has insurance through their own employer and is also listed under a spouse’s plan, their own employer plan is usually primary. The spouse’s plan is usually secondary.

This is because the patient is the main subscriber on one plan and dependent on the other.

Common Primary and Secondary Insurance Situations

Employer Insurance and Spouse’s Insurance

If a patient has coverage through their own job and also has coverage through a spouse, the patient’s own employer plan usually pays first. The spouse’s plan usually pays second.

Child Covered by Both Parents

When a child is covered under both parents’ insurance plans, many insurance companies use the birthday rule. The parent whose birthday comes first in the calendar year usually has the primary plan.

For example, if one parent’s birthday is March 5 and the other parent’s birthday is October 12, the March birthday usually makes that parent’s plan primary. The year of birth does not matter.

Divorced or Separated Parents

For children of divorced or separated parents, the rules may depend on custody arrangements or court orders. Sometimes the custodial parent’s plan is primary. In other cases, a court order may decide which parent must provide insurance.

Because these situations can vary, providers should confirm the correct payer order before submitting claims.

Medicare and Employer Insurance

Medicare may be primary or secondary depending on the patient’s employment status, employer size, disability status, and other Medicare Secondary Payer rules.

This area can be more complex. If Medicare is billed first when another plan should pay first, the claim may be denied. Providers should verify the payer order carefully before billing.

Medicaid and Private Insurance

Medicaid is often the payer of last resort. This means that when a patient has private insurance and Medicaid, the private insurance usually pays first. Medicaid may then review the remaining eligible balance.

However, Medicaid rules can vary by state and plan type. Billing teams should always verify the details before submitting claims.

Why Correct Payer Order Matters

Correct payer order is not just a paperwork issue. It directly affects reimbursement.

If the secondary insurance is billed before the primary plan, the claim may be denied. The billing team may then need to correct the insurance order, bill the primary plan, wait for the EOB, and then submit the secondary claim again.

This creates extra work and delays payment. It may also increase accounts receivable days for the practice.

For therapy providers, payer order is especially important because many patients may have employer insurance, Medicaid, or another secondary policy. In these cases, accurate eligibility verification and benefit checks help prevent denials. This is also where ABA billing services may involve careful review of primary and secondary insurance details so claims are submitted in the correct sequence.

Can Patients Choose Which Plan Pays First?

In most cases, no. Patients cannot decide which insurance plan pays first.

The payer order is based on coordination of benefits rules. Even if the secondary plan has better benefits, it cannot usually be billed first unless it is officially primary under COB rules.

Patients should inform providers about all active insurance plans. They should also update both insurance companies if their coverage changes. This helps prevent confusion when claims are processed.

What Providers Should Verify Before Billing

Before submitting a claim, providers should confirm:

-

Whether the patient has more than one active insurance plan

-

Which plan is primary

-

Which plan is secondary

-

Whether COB information is updated

-

Whether the secondary payer requires the primary EOB

-

Whether Medicaid, Medicare, or employer coverage affects payer order

These steps may seem basic, but they prevent many avoidable denials.

Common Mistakes to Avoid

One common mistake is assuming the patient’s preferred plan is primary. Another mistake is failing to ask about other active coverage during intake.

Billing teams should also avoid submitting secondary claims without the primary EOB. In many cases, the secondary payer cannot process the claim without proof of how the primary plan handled it.

Another issue is outdated COB information. If the patient changes jobs, gets married, loses coverage, adds Medicaid, or becomes eligible for Medicare, the insurance order may change.

FAQs

1. Which insurance pays first?

The primary insurance pays first. The secondary insurance reviews the claim after the primary plan processes it.

2. Does secondary insurance pay the full remaining balance?

Not always. Secondary insurance may pay part of the remaining eligible balance, depending on its own plan rules.

3. Can a patient choose which insurance is primary?

Usually, no. The primary plan is determined by coordination of benefits rules.

4. What happens if the wrong insurance is billed first?

The claim may be denied or delayed. The provider may need to correct the payer order and resubmit the claim.

5. Is Medicaid usually secondary?

In many cases, yes. Medicaid often pays after private insurance, but rules may vary by state.

Conclusion

Primary and secondary insurance work together, but they do not pay at the same time. The primary insurance pays first. The secondary insurance may review the remaining eligible balance after the primary plan has processed the claim.

The most important step is confirming the correct payer order before billing. When providers verify coverage, update COB details, and submit claims in the right sequence, they can reduce denials, avoid payment delays, and create a smoother billing experience for patients and staff.

Categorie

Leggi tutto

Der Path to Glory (PtG) Upgrade Tracker zu EA Sports FC 26 begleitet alle dynamischen WM-Karten während der Weltmeisterschaft 2026. Er listet die Startwerte der PtG-Profis, bereits erhaltene Verbesserungen und den Fortschritt möglicher weiterer Upgrades. Die Karten sind Live-Items, deren Aufwertung nicht von der individuellen Leistung, sondern vom Abschneiden der jeweiligen...

The aviation industry is often associated with pilots, cabin crew, and aircraft engineers. However, behind every successful airline and airport is a large team of professionals responsible for managing operations, customer service, logistics, safety, finance, and administration. This is where a BBA in Aviation Management becomes relevant. For students who are passionate about aviation but...

Packaging is an essential component in the marketing and logistics of products, and the case of playing cards is no different. Custom playing card boxes have both beauty and practical roles and determine the perception of value by the consumer. Most companies want to differentiate their brand identity using packaging, but they pay little attention to the influence of this on the total cost....

The global Automated Nucleic Acid Extraction Market Size is valued at USD 4.31 billion in 2025 and is projected to reach USD 9.24 billion by 2033, growing at a CAGR of 10.03% during the forecast period from 2026 to 2033. The market is witnessing strong growth driven by increasing demand for rapid and accurate molecular diagnostics, along with advancements in genomics and...

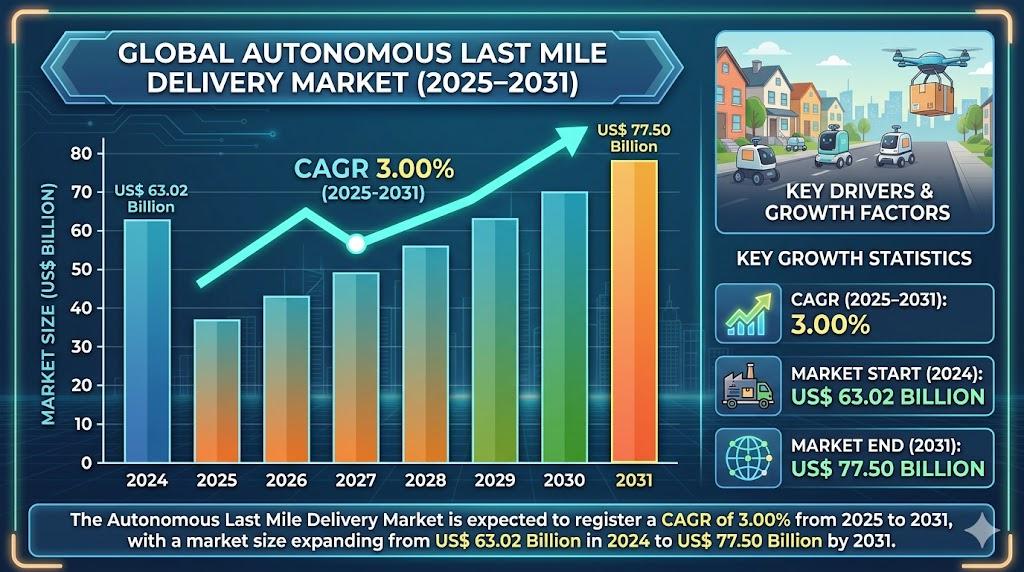

The logistics sector is undergoing a profound transformation driven by rapid technological integration and evolving consumer patterns. According to a research study published by The Insight Partners, the final leg of the logistics journey is transitioning toward full automation. The Autonomous Last Mile Delivery Market is expected to register a CAGR of 3.00% from 2025 to 2031, with...