Best Family Health Insurance Plans in India (2026 Guide)

Securing the medical well-being of one’s household has transitioned from being a secondary financial thought to a primary pillar of responsible fiscal planning. As the landscape of medical care in India continues to advance, the complexity of managing rising treatment costs has made it essential to identify the Best Family Health Insurance Plans In India. A family floater plan operates on a shared pool principle, where a single sum insured covers all registered members of the household, typically including the policyholder, spouse, and dependent children. This structure is often more economical and administratively simpler than maintaining multiple individual policies with varying renewal dates and terms.

When navigating the current market, the primary objective is to find a balance between comprehensive coverage and sustainable premiums. The Best Health Insurance Plans In India are no longer defined solely by their price tags but by their ability to provide a seamless healthcare experience during stressful times. In 2026, the criteria for selecting a top-tier plan involve scrutinising the fine print regarding hospital networks, restoration benefits, and the speed of claim settlements.

The Mechanism of Family Floater Coverage

A family floater policy acts as a collective safety net. If a household has a total coverage of ₹15,00,000, any member can utilise this amount for hospitalisation. If one member consumes ₹4,00,000 for a procedure, the remaining ₹11,00,000 remains available for the rest of the family for the remainder of the policy year. This flexibility is particularly beneficial for younger families where the probability of all members requiring expensive treatment simultaneously is relatively low.

For those looking for the Best Family Health Insurance Plans In India, it is vital to consider the inclusion of elderly parents. While most floater plans allow the addition of parents, doing so can significantly increase the premium because the cost is usually determined by the age of the oldest member. In such cases, experts often suggest keeping senior citizens on separate individual plans while maintaining a floater for the younger nuclear unit to ensure the most cost-effective protection.

Essential Features to Prioritise in 2026

The definition of a "good" plan has evolved. To ensure you are investing in the Best Health Insurance Plans In India, certain non-negotiable features must be present in the policy document.

-

Restoration or Refill Benefit: This is perhaps the most critical feature for a family. If the sum insured is exhausted due to a major claim, the insurer automatically restores the original amount for subsequent hospitalisations. Some modern plans now offer unlimited restoration, which provides an incredible layer of security for families with multiple members.

-

No Room Rent Caps: Many older or basic policies limit the room rent to 1% of the sum insured. In a modern hospital, this often forces the policyholder to pay a significant portion of the total bill out of pocket due to proportionate deductions. The Best Family Health Insurance Plans In India typically offer "No Room Rent Limit" or "Single Private A/C Room" eligibility, ensuring that the insurer covers the actual cost of the room without penalising other associated medical charges.

-

Pre and Post-Hospitalisation Coverage: Medical expenses are rarely confined to the duration of the hospital stay. A comprehensive plan should cover diagnostic tests, consultations, and medicines for at least 60 days before admission and 90 to 180 days after discharge.

-

Modern Treatment Coverage: With the rise of robotic surgeries and advanced stem cell therapies, ensuring that your policy covers "Modern Treatments" is essential. Many traditional policies used to exclude these, but they are now standard inclusions in the Best Health Insurance Plans In India.

The Importance of Cashless Facilities and Network Hospitals

The true value of any health insurance in English or any other language is realised at the hospital billing desk. A robust network of hospitals where the insurer has a direct tie-up allows for cashless hospitalisation. This means the policyholder does not have to arrange for large sums of cash upfront during an emergency. The insurer settles the admissible expenses directly with the healthcare provider.

In 2026, many insurers have expanded their networks to include even smaller boutique clinics and specialised day-care centres. When evaluating the Best Family Health Insurance Plans In India, one must verify that the hospitals in their immediate vicinity and the top-tier tertiary care hospitals in their city are included in the insurer’s network. A high Claim Settlement Ratio (CSR) and a low grievance ratio are also strong indicators of how reliably an insurer handles these cashless requests and final settlements.

Waiting Periods and Pre-existing Diseases

One of the most misunderstood aspects of health coverage is the waiting period. Most policies do not cover pre-existing diseases (PED) from day one. Traditionally, there was a three to four-year wait. However, the Best Health Insurance Plans In India now offer options to reduce this waiting period to one or two years, or even provide "Day 1" coverage through specific add-ons.

Transparency is key here. Disclosing all past medical histories, even minor surgeries or chronic conditions like hypertension, is mandatory to ensure that claims are not rejected later. While a PED waiver might increase the premium, it ensures that the family is protected when they need it most, rather than finding out during a crisis that a particular condition is currently "under waiting."

Enhancing Protection with Add-ons

While a base policy provides the foundation, riders or add-ons allow for customisation. Families often look for the following to supplement the Best Family Health Insurance Plans In India:

-

Maternity and Newborn Cover: Since most standard plans have a long waiting period for maternity (often 2 to 4 years), planning ahead is necessary. These riders cover delivery expenses and provide immediate cover for the newborn from day one, including vaccinations.

-

OPD Cover: Many families find that their frequent expenses are not for hospitalisation but for doctor consultations and pharmacy bills. Outpatient Department (OPD) covers help reimburse these smaller but more frequent costs.

-

Consumables Cover: During a hospital stay, a significant portion of the bill often consists of non-medical items like gloves, masks, and nebulizer kits, which are usually excluded. A consumables rider ensures these are paid for by the insurer.

Final Considerations for Selection

Choosing the right sum insured is the final piece of the puzzle. With medical inflation rising, a cover that seemed adequate five years ago may fall short today. For a family of four living in a metropolitan area, a sum insured of at least ₹15,00,000 to ₹25,00,000 is recommended.

The Best Health Insurance Plans In India also offer wellness rewards. Many insurers now track your physical activity through wearable devices and offer discounts on renewal premiums for maintaining a healthy lifestyle. This proactive approach not only keeps the family fit but also reduces the long-term cost of the policy.

Investing in a family health plan is not merely a tax-saving exercise under Section 80D; it is a strategic move to safeguard the family's hard-earned savings. By carefully comparing the features of the Best Family Health Insurance Plans In India, one can ensure that when a medical emergency strikes, the focus remains entirely on recovery rather than the financial burden of the treatment. Selecting a plan with a reputable insurer, a wide hospital network, and clear terms will provide the peace of mind every household deserves in 2026.

Categorias

Leia Mais

Pune EscortsEscorts Service in Mumbai PleasureSeeker is a leading escort service dedicated to providing sophisticated, tailored experiences that align perfectly with your personal desires and fantasies. Our carefully selected escorts are not only strikingly beautiful but also skilled at creating authentic, engaging interactions that leave a lasting impression. We prioritize complete...

Bangkok is a city of contrasts — towering skyscrapers stand beside ancient temples, modern malls exist alongside traditional street markets, and fast highways run parallel to historic canals. Among the most unforgettable cultural experiences in Thailand’s capital are its floating markets. These vibrant water-based marketplaces allow visitors to witness a centuries-old trading...

Introduction: Polytetrafluoroethylene (PTFE) prices in 2025 showed mixed movement across regions, influenced by feedstock costs, energy prices, and steady industrial demand. Supply remained stable in key producing countries, supporting balanced market conditions. The polytetrafluoroethylene (PTFE) price chart reflected moderate regional variations, driven by differences in production...

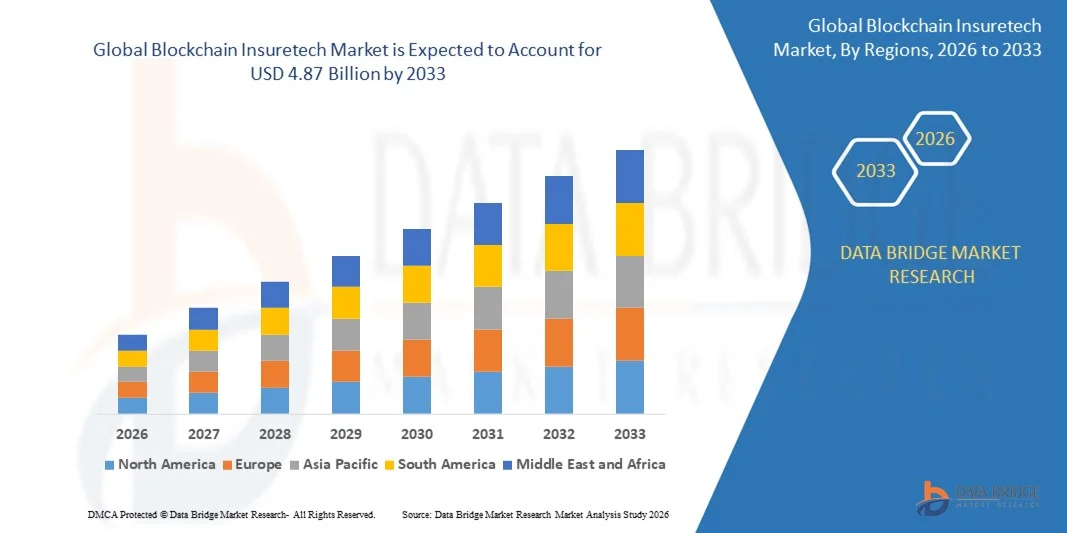

Blockchain Insuretech Market: According to the latest report published by Data Bridge Market Research, the Blockchain Insuretech Market The global blockchain insuretech market size was valued at USD 2.20 billion in 2025 and is expected to reach USD 4.87 billion by 2033, at a CAGR of10.40% during the forecast period Attaining maximum return on...

UK Security Watchdog Raises Concerns Over Encrypted App Development Security experts are alarmed by a recent statement from the UK's independent reviewer of national security legislation suggesting that creating secure messaging applications could potentially be classified as "hostile activity" under current laws. Jonathan Hall KC's latest assessment of the Counter-Terrorism and Border...