Calcium Montmorillonite: The Quiet Infrastructure Clay Behind Foundries, Feed Mills, Pet Care, Drilling, and Soil Engineering

Calcium montmorillonite Market does not enter industry as a glamorous mineral. It enters through rail sidings, bulk bags, mine stockyards, pelletizing drums, blending silos, feed premix units, litter granulation lines, drilling mud tanks, and civil-engineering trenches. Its value is not built on one application. It is built on repetition: 1 tonne mined, 8–12 tonnes handled through logistics, 3–5 quality checks before dispatch, and 6–10 downstream industries depending on moisture control, binding, adsorption, swelling, or rheology.

Semple Request At: https://datavagyanik.com/reports/global-calcium-montmorillonite-market/

At the mine level, Calcium montmorillonite begins as a layered aluminosilicate clay with high surface area, exchangeable calcium ions, and plate-like particles generally below 2 microns after beneficiation. A typical commercial chain starts with open-pit extraction, solar drying or rotary drying, crushing to below 10–30 mm, milling to 100–325 mesh, and packing in 25 kg bags, 1-tonne jumbo bags, or bulk tanker loads. For every 100,000 tonnes of saleable clay, the supporting infrastructure usually requires 4–6 hectares of active mining and stockyard space, 2–3 crushing stages, 1–2 drying systems, and 3–5 product grades.

The industrial story of Calcium montmorillonite is a story of controlled imperfection. It absorbs water, but not like a sponge. It binds particles, but not like cement. It improves viscosity, but not like a synthetic polymer. Its strength lies in low-cost functional behaviour: 2–5% addition can change the economics of a foundry sand system, 0.5–2% inclusion can improve feed pellet durability, and 5–15% use in absorbent products can alter clumping, odour capture, and moisture retention.

In foundry infrastructure, Calcium montmorillonite works behind every moulding line where green sand needs repeatable plasticity. A medium foundry producing 20,000 tonnes of castings a year may circulate 80,000–120,000 tonnes of sand internally, but clay binder demand may sit at only 1,200–3,000 tonnes annually. This small ratio gives the clay strategic importance: if sand moisture shifts by 1%, mould strength can fall, scrap rates can rise by 2–4%, and surface defects can multiply across thousands of castings.

In feed infrastructure, Calcium montmorillonite is a logistics mineral disguised as a nutrition-side input. Feed mills running 10 tonnes per hour can process 50,000–80,000 tonnes annually on a single line, and even a 1% clay inclusion translates into 500–800 tonnes of annual demand per mill. Its role is practical: pellet binding, flow improvement, moisture balancing, and adsorption of undesirable compounds. Poultry and livestock feed users care less about mineral romance and more about pellet durability index, dust reduction, storage stability, and mill throughput.

The pet care segment gives Calcium montmorillonite a consumer-facing identity. A cat litter plant may convert 30,000–150,000 tonnes of clay annually into granules, with drying, screening, dedusting, fragrance blending, and bagging as the main cost centres. In this chain, every 1% reduction in fines can reduce rejected material by 300–1,500 tonnes per year depending on plant scale. Every 2% improvement in moisture control can reduce freight inefficiency because water is one of the most expensive things to transport when the product sells by weight.

According to DataVagyanik, the global Calcium montmorillonite market is valued at USD 1,184.7 million in 2026 and is forecast to reach USD 1,642.9 million by 2032, growing at a CAGR of 5.6% between 2026 and 2032. The forecast reflects rising demand from animal feed binders, absorbent clay products, civil-engineering barriers, foundry sand systems, and specialty adsorption applications, with Asia Pacific accounting for the largest incremental volume addition due to expanding feed production, urban infrastructure, pet care adoption, and mineral-processing capacity.

The civil-engineering story is more physical than chemical. Calcium montmorillonite is used where water must be slowed, redirected, absorbed, or sealed. In landfill liners, ponds, canal works, basement waterproofing, tunnel grouting, and slurry trenching, the value is measured in permeability. A liner system may target hydraulic conductivity near 10⁻⁹ m/s, and clay quality determines whether that barrier performs for 10 years or 50 years. On a 20-hectare landfill cell, even a 5 kg/m² clay layer creates 1,000 tonnes of mineral demand before geotextile, compaction, and installation losses.

Drilling and tunnelling add another layer to the infrastructure map. Calcium montmorillonite may be used directly or beneficiated depending on viscosity requirement. A single horizontal directional drilling project of 5 km can consume 20–100 tonnes of bentonitic clay products, depending on bore diameter, soil condition, fluid loss, and recycling efficiency. In metro tunnelling, clay-based slurry supports excavation stability where collapse risk is measured not in tonnes but in minutes: one slurry failure can stop a tunnel boring machine, delay crews, and freeze equipment worth millions of dollars.

The agricultural use case is smaller per hectare but large in surface logic. Soil conditioners, pesticide carriers, seed coatings, and moisture-retention mixes use Calcium montmorillonite because a gram of fine clay can offer significant adsorptive surface. A 10,000-hectare farming cluster using only 5 kg per hectare in seed treatment or soil amendment can create 50 tonnes of seasonal demand. Scale that to 2 million hectares of commercial agriculture and the volume becomes 10,000 tonnes, enough to justify dedicated milling, bagging, and regional distribution.

The technical heartbeat of Calcium montmorillonite is cation exchange capacity, swelling behaviour, particle size, moisture, grit content, and mineral purity. Industrial buyers typically test moisture below 12%, residue on 200 mesh, methylene blue value, swelling index, pH, bulk density, and heavy metals depending on application. A feed-grade buyer may reject a shipment for contamination measured in parts per million, while a foundry buyer may reject the same shipment for poor green compression strength. Same mineral, different pass/fail logic.

The manufacturing map is therefore not just mining. It is grade discipline. One producer may sell crude clay at USD 40–80 per tonne near the mine, while beneficiated, micronized, activated, or feed-certified Calcium montmorillonite can move into higher-value bands depending on purity, packaging, certification, freight distance, and application risk. In low-margin applications, freight can represent 25–45% of delivered cost. In certified specialty applications, documentation, testing, and consistency can become more important than mining cost.

Asia’s advantage is volume. India, China, Turkey, and parts of Central Asia can support mine-to-port and mine-to-factory clay flows because construction, feed, foundry, and absorbent product demand sit close to mineral belts. A clay processor located within 150 km of deposits and 300 km of consuming industries can reduce delivered cost by 8–15% compared with a supplier moving low-value mineral over long road distances. This is why Calcium montmorillonite competitiveness is often decided before the product reaches the customer: geology plus logistics beats brochure-based marketing.

Europe’s story is quality and compliance. Pet litter, environmental barriers, foundry binders, and industrial absorbents require dust control, worker safety documentation, product traceability, and stable packaging. A 25,000-tonne-per-year litter brand cannot afford batch swings that create dust complaints, broken granules, or inconsistent clumping. In that setting, Calcium montmorillonite becomes part mineral, part process-control input, and part consumer-experience material.

North America’s infrastructure demand is tied to drilling, environmental remediation, pet care, and industrial absorbents. A spill-control product line may consume only 2,000–10,000 tonnes annually, but margins are higher because performance is sold through emergency response, warehousing, and workplace safety channels. In contrast, a bulk drilling-grade customer may buy larger tonnes but negotiate aggressively on delivered cost, viscosity, and yield.

The next growth story for Calcium montmorillonite will not come from one spectacular breakthrough. It will come from 10,000 small substitutions: synthetic binders reduced by 5%, feed dust lowered by 3%, landfill liner performance improved over decades, litter bags made lighter by better granulation, and drilling fluids adjusted for water-sensitive formations. This is infrastructure material logic. The mineral wins when it solves a physical problem repeatedly, cheaply, and close to the point of use.

Calcium montmorillonite is therefore not a single market. It is a chain of mines, dryers, mills, silos, lab benches, trucks, ports, feed lines, moulding boxes, litter bags, slurry tanks, and engineered barriers. Its adoption is counted in percentages, but its impact is counted in avoided defects, stabilized soils, cleaner feed mills, lower dust, better moisture control, and fewer failed barriers. That is why a clay that sells by the tonne quietly influences industries measured in billions.

Application Mapping: Where Calcium Montmorillonite Creates Measurable Value

The first application cluster is absorbency. In pet litter, industrial spill control, moisture-control packs, agricultural carriers, and hygiene-adjacent absorbents, Calcium montmorillonite competes on grams of liquid retained per gram of mineral, dust percentage, granule strength, and odour-holding capacity. A standard 5 kg litter bag may contain clay granules screened between 0.5 mm and 4 mm, with fines controlled below 3–7% depending on product grade. At a plant producing 10 million bags a year, every 100 grams of avoidable excess moisture per bag equals 1,000 tonnes of unnecessary shipped weight.

The second cluster is binding. Foundry sand, feed pellets, briquettes, fertilizers, and construction mixes use clay because tiny particles create physical bridges between larger particles. In a feed pellet line, binder inclusion at 0.5–1.5% may look small, but on a 200,000-tonne annual feed operation, that becomes 1,000–3,000 tonnes of mineral movement. If pellet breakage falls from 8% to 5%, the mill saves 6,000 tonnes of degraded feed form each year, reducing dust, reprocessing, and customer complaints.

The third cluster is barrier performance. In landfill caps, slurry walls, ponds, canal linings, and environmental containment systems, Calcium montmorillonite is used because water movement is expensive when it is uncontrolled. A 1-hectare pond lining system using 6 kg per square metre requires around 60 tonnes of clay before compaction losses. A 50-hectare industrial containment project can therefore absorb 3,000 tonnes, but the economic value sits in avoided seepage, regulatory compliance, and asset life rather than mineral tonnage alone.

The fourth cluster is carrier and adsorption chemistry. Calcium montmorillonite can hold active ingredients, reduce caking, improve flow, and stabilize powder blends. In agrochemical granules, seed treatments, veterinary premixes, and feed additives, the clay may represent 10–60% of the carrier mass depending on formulation. A pesticide granule plant producing 25,000 tonnes annually could use 2,500–15,000 tonnes of clay carrier if the formulation strategy is mineral-heavy. This is why clay processors often serve agriculture through formulators rather than farmers directly.

Infrastructure Spend: The Hidden Capital Behind a Low-Cost Mineral

A small clay beneficiation unit is not capital-free. A basic 30,000-tonne-per-year operation may need mining equipment, drying beds or rotary dryers, crushers, pulverizers, classifiers, dust collectors, screening systems, storage sheds, moisture-control systems, forklifts, bagging units, and a testing laboratory. Even where mining rights are inexpensive, operating reliability depends on 8–12 separate infrastructure nodes between pit and packed product.

Drying is usually the biggest energy-sensitive step. Clay mined at 25–35% moisture may need to be reduced below 10–12% for many industrial users. Removing 1 tonne of water requires energy, time, handling, and sometimes fuel-price exposure. If a plant dries 100,000 tonnes of wet clay with 30% moisture into saleable material at 10% moisture, it removes roughly 22,000 tonnes of water. That is why seasonal weather, dryer efficiency, covered storage, and pre-drying yards can decide margin more than mining cost.

Milling determines market access. Coarse grades may serve absorbents, civil works, and some agricultural carriers. Fine grades serve feed, foundry, coatings, drilling blends, and specialty adsorption. Moving from 100 mesh to 325 mesh increases power consumption, maintenance, classifier load, and dust-control requirements. A processor selling Calcium montmorillonite into feed or foundry customers needs consistent particle-size distribution, because a 15–20% swing in fines can change binding, flow, and moisture behaviour.

Packaging also changes economics. Bulk loose supply may work for civil projects and large absorbent plants. Jumbo bags suit feed mills, drilling-fluid blenders, and foundries. Small bags serve retail litter, agricultural products, and specialty users. A 1-tonne jumbo bag can reduce handling cost per tonne, but a 25 kg bag expands customer access in fragmented rural or SME markets. The same mineral can therefore move through three packaging economies: bulk for infrastructure, jumbo for industrial users, and retail pack for consumer channels.

Manufacturer and Player Behaviour: How the Market Actually Moves

The market is shaped by regional mineral processors, bentonite miners, clay refiners, animal-feed additive companies, cat litter brands, foundry material suppliers, drilling-fluid service firms, and agrochemical formulators. The producer at the mine rarely captures the entire value chain. A miner may sell crude or semi-processed clay; a processor upgrades it; a brand owner converts it into a consumer or industrial product; a distributor manages fragmented customers.

Companies that control reserves and processing win on cost. Companies that control certification and formulation win on margins. Companies that control distribution win on customer access. A Calcium montmorillonite supplier selling to a pet litter brand must manage granule size, whiteness or colour, dust, odour control, absorption, and packaging reliability. A supplier selling to a feed additive blender must manage safety documentation, toxin limits, moisture, microbial quality, and traceability. A supplier selling to a civil contractor must manage bulk availability, project timing, and delivered cost.

The most stable suppliers are those with multi-application balancing. If foundry demand slows, feed and pet care can absorb capacity. If construction projects are delayed, agricultural carriers and absorbents support offtake. A 100,000-tonne processor with 40% pet care exposure, 25% feed exposure, 15% foundry exposure, 10% civil works exposure, and 10% specialty applications is structurally safer than a plant dependent on one seasonal customer group.

Timeline of Spend and Demand Signals

From 2018 to 2020, demand was shaped by low-cost absorbents, feed binder adoption, and steady foundry consumption. The major shift came from logistics: buyers became more sensitive to local supply after freight volatility exposed the weakness of moving low-value mineral over long routes. A tonne of clay worth USD 80–150 near a plant could become commercially unattractive if road freight added USD 30–60 per tonne.

From 2020 to 2022, pet ownership, home hygiene products, agricultural input reformulation, and supply-chain localization strengthened clay demand in consumer and industrial channels. Cat litter and absorbent products gained volume because households shifted spending toward indoor pet care and hygiene. At the same time, feed mills looked for low-cost functional additives to control pellet quality, moisture, and storage risk under volatile grain and protein-meal prices.

From 2022 to 2024, infrastructure and environmental uses became more visible. Landfill engineering, wastewater containment, pond lining, construction sealing, and remediation projects increased the importance of clay-based barriers. Industrial buyers also became more specification-driven: dust limits, heavy-metal checks, documentation, moisture control, and particle consistency moved from optional quality points to routine procurement filters.

From 2024 to 2026, the market moved into a more segmented phase. Commodity Calcium montmorillonite continued to compete on delivered price, but feed-grade, pet-care-grade, foundry-grade, and environmental-grade products separated by documentation and performance. The price gap between crude clay and processed grades widened because buyers were no longer buying clay alone; they were buying lower rejection rates, stable production, and regulatory comfort.

Use Case Economics: Why Small Percentages Create Large Market Pull

In pet litter, a plant processing 100,000 tonnes annually can justify investment in better dryers, screeners, and dust collectors if fines reduction improves saleable output by 2%. That 2% equals 2,000 tonnes of extra usable product. At industrial scale, waste reduction is not an environmental slogan; it is a direct capacity multiplier.

In feed, the economics are equally practical. If Calcium montmorillonite improves pellet durability and reduces fines by even 1.5 percentage points in a 300,000-tonne feed mill, it protects 4,500 tonnes of product form. That can reduce customer rejection, improve truck unloading, and lower dust inside storage silos. For large integrators, the value is not only ingredient cost but smoother movement from mill to farm.

In foundries, the use case is defect reduction. A casting line producing 100 tonnes per day with a 3% scrap rate loses 3 tonnes daily. If better binder consistency reduces scrap by only 0.5 percentage points, the recovered output is 0.5 tonnes per day, or roughly 150 tonnes annually on a 300-day production calendar. The clay cost is small compared with labour, energy, machining, and rejected metal value.

In civil engineering, the use case is risk avoidance. A containment project using 5,000 tonnes of mineral barrier material may appear material-heavy, but the cost of seepage, rework, regulatory penalties, groundwater treatment, or project delay can exceed the mineral cost several times. This is why Calcium montmorillonite is often specified not because it is expensive, but because failure is expensive.

The Investment Theme: From Raw Clay to Engineered Mineral Platforms

The next wave of value will come from engineered grades. Producers will invest in cleaner beneficiation, controlled drying, lower-dust milling, automated bagging, moisture-stable warehousing, and application laboratories. A serious supplier will need more than a mine: it will need rheology testing for drilling customers, compression-strength testing for foundry users, pellet durability testing for feed users, absorption testing for litter brands, and permeability support for civil-engineering buyers.

By 2030, the strongest Calcium montmorillonite suppliers will look less like quarry operators and more like mineral-platform companies. Their competitive edge will be measured in 5 numbers: tonnes of controlled reserves, processing capacity, moisture consistency, rejection rate, and delivered-cost radius. The winners will not simply sell clay. They will sell predictability.

The core theme is simple: industries do not adopt this mineral because they want another raw material. They adopt it because it converts physical uncertainty into manageable behaviour. Wet sand becomes mouldable. Loose feed becomes durable pellets. Leaking soil becomes a barrier. Spilled liquid becomes manageable waste. Powder blends become flowable. Pet litter becomes a repeat-purchase consumer product.

That is the infrastructure story of Calcium montmorillonite: a low-cost clay sitting underneath high-cost systems. Its market expands when factories need consistency, farms need efficiency, cities need containment, pet owners need convenience, and contractors need materials that perform without complex chemistry. In a world where every industry is trying to reduce waste, stabilize inputs, and localize supply chains, this mineral remains quiet, heavy, practical, and economically difficult to replace.

From Soybean Crushing Corridors to Dairy Clusters: How Bypass Protein Soybean Meal Builds a Measurable Feed Economy

The geographic story of Bypass Protein Soybean Meal begins with soybean availability. The United States, Brazil, Argentina, India, and China together form the core soybean meal production and consumption axis. These countries already operate large crushing, solvent extraction, refining, feed milling, and livestock-input networks. That matters because bypass protein adoption does not begin with a laboratory product; it begins where soybean meal is already trusted by nutritionists, bought in bulk by feed mills, and understood by farmers as a protein base. The infrastructure advantage is that Bypass Protein Soybean Meal upgrades an existing feed chain instead of forcing livestock producers to shift to an unfamiliar raw material.

In Brazil, Argentina, and the United States, soybean meal moves through export terminals, river logistics, crushing complexes, and industrial feed formulators. In India, it moves through solvent extraction plants, dairy cooperatives, private feed mills, and regional cattle-feed brands. In China, it is closely linked with intensive livestock farming, commercial feed manufacturing, and imported soybean crushing. Across these regions, the technical opportunity is similar: take a protein ingredient already produced in millions of tons and carve out a premium functional segment for cows, buffaloes, and high-performance ruminants.

The adoption timeline can be read in four phases. Before 2010, bypass protein was mostly a nutritionist-led concept used in progressive dairy systems and research farms. Between 2010 and 2016, commercial dairies began adopting protected proteins as milk-yield targets rose above 20 liters per animal per day in organized farms. Between 2017 and 2022, feed companies started positioning bypass protein as a branded productivity ingredient, especially in dairy-intensive regions. From 2023 onward, Bypass Protein Soybean Meal entered a more quantified era, where feed companies increasingly discuss protein efficiency, nitrogen loss reduction, milk response, ration precision, and lifecycle productivity.

The spending pattern follows the same curve. A traditional dairy farm may spend 55–70% of operating cost on feed, with concentrates representing a major share for lactating animals. When feed inflation rises, the first reaction is usually ingredient substitution. But organized farms have learned that cutting protein quality can reduce milk output faster than it saves money. This is where Bypass Protein Soybean Meal becomes a defensive input. It allows the farm to protect milk yield while improving protein utilization, which is why adoption rises during both high milk-price periods and high feed-cost periods.

On a 100-cow commercial dairy, daily concentrate feed use can range from 600 kg to 1,200 kg depending on milk yield, forage quality, and lactation stage. If Bypass Protein Soybean Meal forms even 5–12% of the concentrate mix, the farm consumes 30–144 kg per day. Over a 300-day lactation-linked feeding cycle, that becomes 9–43 metric tons of annual demand from a single mid-sized unit. Multiply this by 1,000 organized farms in a regional dairy belt, and the demand pool becomes 9,000–43,000 metric tons annually without including calves, heifers, or beef systems.

The application mapping is not uniform across animals. High-yield cows are the primary use case because their amino acid demand exceeds what ordinary rumen microbial protein can support. Buffaloes are another important pocket in South Asia because high-fat milk economics rewards productivity improvement, especially when animals are in early and mid-lactation. Beef cattle represent a smaller but growing premium channel where finishing systems are becoming more scientific. Sheep and goats are minor but possible users in intensive systems, though their inclusion rates are much lower and usually depend on specialty feed formulation.

A useful way to quantify demand is by milk intensity. Farms below 8 liters per animal per day usually focus on low-cost roughage, oil cakes, bran, and basic concentrate. Farms in the 8–15 liter range start using balanced concentrate and mineral mixtures. Farms above 15 liters enter the zone where protein quality, energy density, fat supplementation, rumen health, and amino acid delivery become critical. Farms above 25 liters are the strongest natural buyers of Bypass Protein Soybean Meal because each lost liter of milk becomes a measurable revenue loss.

The theme becomes clearer when viewed through a 1-liter milk response model. If 1 kg of Bypass Protein Soybean Meal helps produce an incremental 0.8 liter of milk in a responsive cow, and the milk price is USD 0.45 per liter, the revenue gain is USD 0.36 per day. If the ingredient premium is USD 0.15 per day after replacing conventional meal, the net operating gain is USD 0.21 per cow per day. For 200 cows, that equals USD 42 per day and USD 12,600 across a 300-day effective cycle. The numbers become persuasive only when animals, rationing, and management are good enough to respond.

This is why adoption is strongest in farms with measurable systems. Milk meters, bulk tanks, feed mixers, lactation grouping, veterinary records, and body-condition scoring all increase the chance that Bypass Protein Soybean Meal will be used correctly. A farm feeding all animals the same mixture cannot capture full value because dry cows, early-lactation cows, peak-lactation cows, and late-lactation cows do not need the same protein flow. In advanced systems, bypass protein is directed toward the animals that can monetize it fastest.

The manufacturing story has its own numbers. A commercial feed processor handling 100,000 tons of annual cattle feed may allocate 3–8% of volume to premium protein-enhanced formulations. That creates 3,000–8,000 tons of higher-value feed output. If Bypass Protein Soybean Meal inclusion averages 8–15% in those formulations, the processor may require 240–1,200 tons of bypass soybean meal annually. For a regional processor, this is large enough to justify dedicated procurement, testing, and supplier contracts. For a national feed company, it becomes a strategic product line.

The infrastructure required is not glamorous, but it is decisive. Warehouses must control moisture because soybean meal quality deteriorates when exposed to humidity. Finished feed must avoid fungal growth because mycotoxins can reduce milk yield and reproductive performance. Heat treatment must be standardized because inconsistent processing changes protein solubility. Transport must protect material from rain and contamination. Mixing must be accurate because over-inclusion wastes money and under-inclusion weakens results. Every kilogram of Bypass Protein Soybean Meal carries a performance promise, and that promise depends on logistics discipline.

The industry-body trend around dairy modernization is also important. Over the last decade, dairy development programs across Asia, Latin America, and the Middle East have consistently emphasized artificial insemination, breed improvement, milk chilling, veterinary access, fodder development, and feed balancing. Each of these programs indirectly expands the addressable base for Bypass Protein Soybean Meal. Breed improvement creates animals capable of producing more milk. Milk chilling rewards volume and quality. Feed balancing exposes protein gaps. Veterinary networks reduce disease losses. Together, they convert traditional dairying into a measurable protein economy.

In practical terms, the product sits at the intersection of three investment flows: oilseed processing investment, animal-feed manufacturing investment, and dairy productivity investment. Soybean processors invest in crushing, extraction, desolventizing, toasting, and meal handling. Feed companies invest in formulation software, pelleting lines, coating systems, lab testing, and distribution. Dairy farms invest in better animals, better sheds, water systems, milking machines, and feed storage. Bypass Protein Soybean Meal benefits when all three investment streams move together.

Application mapping by channel shows five commercial routes. The first is direct sale to large dairies that formulate their own rations. The second is inclusion in branded cattle-feed products. The third is sale through dairy cooperatives that bundle feed with milk procurement. The fourth is nutritionist-led prescription in high-yield herds. The fifth is premix-style positioning where bypass protein is sold as a performance additive. Each route has different economics. Direct dairy sales are volume-driven; branded feeds are margin-driven; cooperative channels are trust-driven; nutritionist channels are performance-driven.

The technical comparison with ordinary soybean meal is central to market behavior. Conventional soybean meal is valued for high protein, amino acid quality, availability, and affordability. Bypass Protein Soybean Meal is valued for controlled degradability, better intestinal amino acid delivery, and performance stability in high-output animals. It does not replace conventional meal in all rations. Instead, it splits the soybean meal category into bulk protein and functional protein. That split is exactly how commodity feed ingredients become specialty nutrition products.

At farmer level, the adoption objection is usually price. A farmer may see ordinary soybean meal at one price and bypass soybean meal at a higher price, then reject the premium. The answer is not persuasion; it is measurement. If milk yield, milk fat, milk protein, body condition, conception interval, and feed cost per liter are not tracked, the product looks expensive. If those numbers are tracked, Bypass Protein Soybean Meal becomes a testable economic input. The difference between rejection and adoption is often one properly monitored 30-day feeding trial.

A 30-day trial can be simple. Select 20 comparable early-lactation animals, feed the revised ration, measure daily milk output, record feed cost, monitor dung consistency, and check milk urea nitrogen where available. If the group gains 0.8–1.2 liters per animal per day, the trial creates 480–720 extra liters in 30 days. At USD 0.45 per liter, that equals USD 216–324 extra revenue from only 20 animals. This is the kind of quantification that moves Bypass Protein Soybean Meal from brochure language to farm decision-making.

The sustainability angle is becoming equally important. Protein is one of the costliest and most nitrogen-intensive parts of a dairy ration. When protein is poorly used, it increases urinary nitrogen, ammonia pressure, and environmental loss. By improving the share of absorbed protein, Bypass Protein Soybean Meal supports lower protein wastage per liter of milk. If a farm produces 10,000 liters of milk per day and reduces feed protein wastage by even 3–5%, the environmental and economic impact becomes material across a year.

The next growth wave will come from precision. More farms will group animals by lactation stage. More feed mills will sell functional dairy feeds rather than generic cattle feed. More processors will certify protected protein claims. More nutritionists will use software to balance metabolizable protein instead of crude protein alone. In that system, Bypass Protein Soybean Meal is not just an ingredient. It becomes a measurable bridge between soybean agriculture, feed technology, dairy infrastructure, and milk economics.

By 2032, the strongest winners will be companies that can prove consistency. The market will reward processors that control heat treatment, document batch quality, maintain supply reliability, and support nutritionists with data. It will reward feed brands that teach farmers how to calculate feed cost per liter. It will reward dairy systems that treat protein as an investment rather than an expense. Most importantly, it will reward farms that understand one simple equation: more animals increase cost, but better protein efficiency increases output from the same herd.

In the end, Bypass Protein Soybean Meal is a story of infrastructure hidden inside an ingredient. The visible product is a brown protein meal. The invisible system behind it includes soybean farms, solvent extraction units, heat-treatment lines, feed laboratories, ration software, veterinary networks, dairy cooperatives, milk chillers, and farmers willing to measure results. That is why its adoption is not driven by trend language. It is driven by liters of milk, kilograms of protein, dollars of feed cost, and the daily arithmetic of turning soybean protein into animal productivity.

Semple Request At: https://datavagyanik.com/reports/global-calcium-montmorillonite-market/

Categorias

Leia mais

https://www.boycat.co/posts/135796

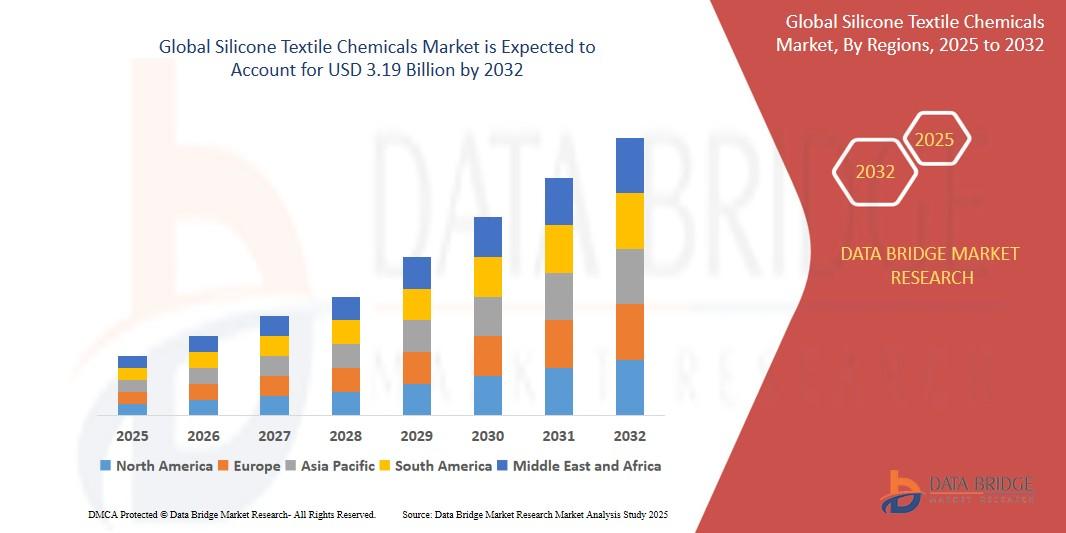

"Executive Summary Silicone Textile Chemicals Market: Share, Size & Strategic Insights The Global Silicone Textile Chemicals Market size was valued at USD 1.84 billion in 2024 and is expected to reach USD 3.19 billion by 2032, at a CAGR of 6.3% during the forecast period Silicone Textile Chemicals Market research report works best for the systematic...

" According to the latest report published by Data Bridge Market Research, the Soil Conditioners Market The global soil conditioners market size was valued at USD 7.40 billion in 2024 and is expected to reach USD 14.13 billion by 2032, at a CAGR of 8.42% during the forecast period This Soil Conditioners Market research report is a comprehensive...

Introduzione Con l'aumento dei prezzi dell'energia e l'ansia per il clima, il mercato dei raffrescatori evaporativi portatili sta suscitando nuovo interesse come alternativa economica ed ecologica ai tradizionali sistemi di condizionamento. Mentre il raffreddamento basato sulla refrigerazione si basa sull'evaporazione dei refrigeranti, i raffrescatori evaporativi sfruttano l'evaporazione...

Ashley Young: Polyvalence et Leadership Une nouvelle recrue vient d’être ajoutée à la DCE de FC 26 : Ashley Young dans sa version Time Warp. À l’horizon 2025, Ashley Young se distingue par sa longévité exceptionnelle et son professionnalisme exemplaire dans le football d’aujourd’hui. Sa capacité à occuper divers...