Factors That Can Affect Your Mortgage Interest Rate

Navigating the housing market can feel like riding a roller coaster, especially when you are trying to secure a home in a bustling metropolitan area. Whether you are eyeing a modern condo in the downtown core or a spacious detached home in the surrounding suburbs, your monthly housing budget will ultimately hinge on one critical figure: your mortgage interest rate.

Even a fraction of a percentage point difference can translate into tens of thousands of dollars saved or lost over the lifespan of your loan. But how exactly do lenders determine that number? While some elements are dictated by sweeping economic shifts, others are entirely within your control. Understanding the core Mortgage Rates dynamics and how they are calculated can give you a significant advantage when negotiating your home loan.

If you want to secure the most competitive Mortgage Rates in Toronto or anywhere else across Canada, it helps to understand the key factors that influence what you will pay.

1. Macroeconomic Drivers: The Big Picture

Before a lender ever looks at your financial profile, a baseline rate is established by broader economic forces. These systemic factors dictate the "floor" for borrowing costs across the country.

The Bank of Canada and the Prime Rate

For anyone considering a variable-rate mortgage, the Bank of Canada (BoC) plays a monumental role. The BoC sets the overnight policy rate eight times a year in response to national economic health, primarily focusing on keeping inflation near its 2% target. When inflation surges, the central bank raises rates to cool consumer spending.

Commercial financial institutions use this policy rate to set their own prime lending rates. If you opt for a variable mortgage, your interest rate will fluctuate in direct tandem with these adjustments, changing the portion of your monthly payment that goes toward your principal balance.

Government Bond Yields

If you lean toward the stability of a fixed-rate mortgage, your true benchmark isn't the BoC policy rate—it is the bond market. Canadian fixed mortgage rates are heavily influenced by 5-year Government of Canada bond yields. Investors trade these bonds constantly based on global economic outlooks, inflation expectations, and geopolitical events. When bond yields climb, lenders’ funding costs rise, and they pass those expenses onto consumers by hiking fixed mortgage rates.

2. Your Personal Financial Profile

While you cannot control global bond markets or central bank announcements, your personal financial habits heavily weigh on the final rate a lender offers you. This is where you can actively optimize your strategy to hunt down the best Toronto Mortgage Rates.

Credit Score and Credit History

Your credit score is a numerical summary of your financial reliability. Lenders view a high credit score as proof that you manage debt responsibly. If your credit report is immaculate, you represent a low default risk, qualifying you for discounted, lower-tier rates. Conversely, a poor credit history signals higher risk, prompting mainstream lenders to either increase your interest rate or reject the application, which may force you to rely on private lenders with much higher borrowing costs.

Down Payment and Mortgage Default Insurance

In Canada, the size of your down payment changes the entire risk architecture of your loan:

-

Less than 20% down: You are legally required to purchase mortgage default insurance (often called CMHC insurance). Because this insurance protects the lender if you default, it lowers their risk. Paradoxically, this means "insured mortgages" often qualify for slightly lower interest rates.

-

20% or more down: You avoid the added cost of premium insurance. While your interest rate might be a hair higher than an insured loan due to the lack of backing, your overall debt load is smaller, saving you thousands in total interest over time.

3. Loan-Specific Variables and Structural Choices

The structure of the mortgage agreement itself will dictate how your interest rate behaves over time.

Fixed vs. Variable Rates

Choosing between a fixed or variable rate is a balancing act between certainty and flexibility. A fixed-rate mortgage locks your interest rate in place for the entire duration of your term (e.g., 5 years), shielding you from market volatility. Lenders typically charge a slight premium for this "peace of mind." A variable rate is often lower at the outset but exposes you to market fluctuations. If the prime rate drops, you reap the rewards; if it climbs, more of your payment is eaten up by interest.

Mortgage Term and Open vs. Closed Parameters

The length of your mortgage term—the duration your current contract remains valid before renewal—also impacts the rate. Typically, shorter terms (like 1-year or 2-year terms) carry different rate pricing than standard 5-year terms based on where lenders predict the economy is headed.

Furthermore, you must choose between an "open" or "closed" mortgage. An open mortgage allows you to pay off your balance early without penalties, but it carries a significantly higher interest rate to compensate the lender for prepayment risk. Closed mortgages restrict early payoffs but reward you with much lower, highly competitive interest rates.

Conclusion

Securing an affordable home loan requires a mix of economic timing and personal financial discipline. While global bond markets and Bank of Canada inflation targets establish the baseline market conditions, your credit score, down payment size, and structural loan preferences ultimately cross the finish line to shape your customized rate. By cleaning up your credit profile, saving a robust down payment, and carefully weighing the trade-offs of fixed versus variable terms, you can confidently secure a mortgage rate that keeps your long-term housing goals firmly within financial reach.

Categorieën

Read More

RR88: A Smooth and Trusted Online Entertainment Platform for Asian Players A Modern Destination for Digital Entertainment RR88 has become a well-known name in the Asian online entertainment space because it focuses on quality, stability, and user comfort. The platform is designed to serve players who want simple access, clear features, and reliable performance every day. With a clean...

Global automotive thermoplastic resin composites market, valued at USD 8.42 billion in 2024, is projected to grow from USD 9.15 billion in 2025 to USD 16.78 billion by 2032, exhibiting a compound annual growth rate (CAGR) of 7.8% during the forecast period. Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/231177/automotive-thermoplastic-resin-composites-market...

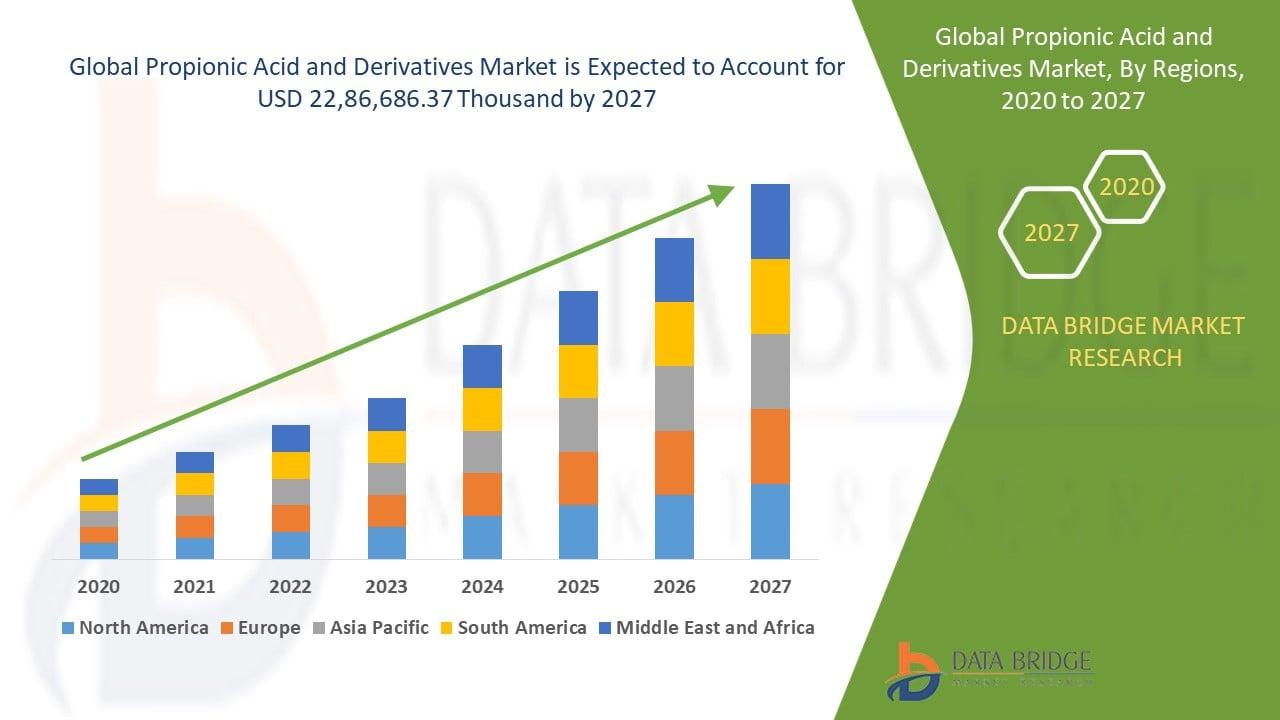

"Comprehensive Outlook on Executive Summary Propionic Acid and Derivatives Market Size and Share The global propionic acid and derivatives market size was valued at USD 1.90 billion in 2024 and is projected to reach USD 3.05 billion by 2032, with a CAGR of 6.10% during the forecast period of 2025 to 2032 The Propionic Acid and Derivatives report encompasses thorough analysis of market...

Slot online has become one of the most popular choices for people who want simple and enjoyable digital entertainment. In an age where convenience matters, many users prefer games that are easy to access and do not require complicated rules. slot online fits perfectly into this lifestyle because it allows players to relax and enjoy the experience without pressure. Whether played during...

The global packaging landscape is undergoing a significant transition as consumer preferences shift toward single-serve and portable formats. Stick packs, characterized by their slender, tube-like shape, have become an essential packaging solution across various industries. The Stick Packing Machine Market is expected to register a CAGR of 5.5% from 2025 to 2031. This growth is...