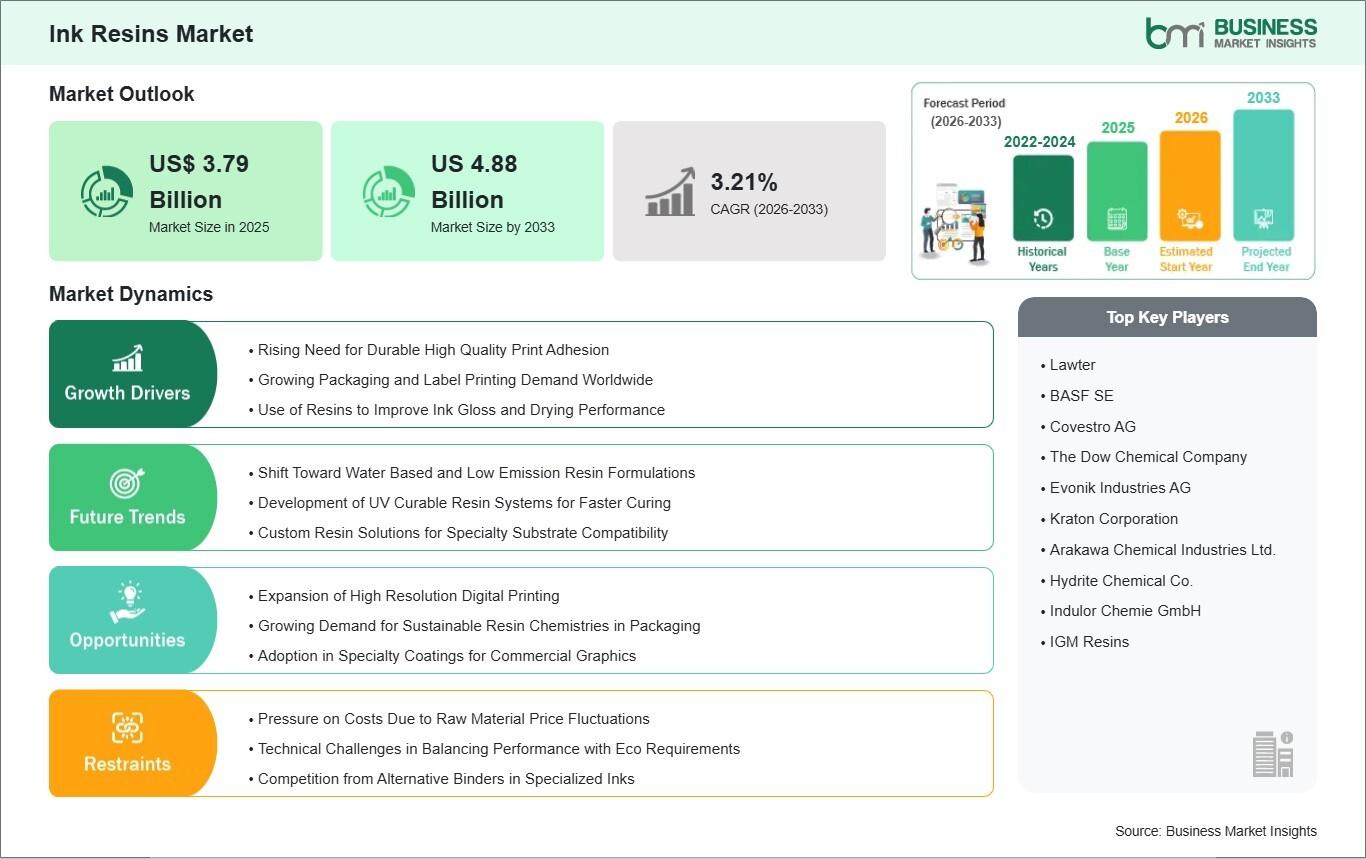

Ink Resins Market on Track to Surpass US$ 4.88 Billion by 2033 Amid Rising Demand for High-Performance Printing Inks

Driven by shifting consumer preferences, the explosive growth of e-commerce, and stringent international environmental regulations, the global printing and packaging industries are experiencing a profound technological transformation.

Data published by Business Market Insights indicates that the international Ink Resins Market will grow at a CAGR of 3.21% from 2026 to 2033, scaling its overall valuation from US$ 3.79 Billion in 2025 to an estimated US$ 4.88 Billion by 2033.

Recent advancements in bio-based materials, water-borne formulations, and energy-curable (UV/EB) resin systems are completely reshaping the competitive landscape. Regulatory bodies globally are tightening limits on Volatile Organic Compounds (VOCs) and hazardous air pollutants, compelling major ink manufacturers to transition away from traditional solvent-based resins. This shift has unlocked massive opportunities for chemical producers who can deliver sustainable, eco-friendly resin alternatives without compromising on high-speed press performance or substrate adhesion.

Download Sample Report : https://www.businessmarketinsights.com/sample/BMIPUB00033991

What Are Ink Resins?

Ink resins, also known as ink binders or vehicles, are high-molecular-weight polymers that serve as the primary structural foundation of printing inks. Their primary function is to bind pigment particles together and adhere them securely to the target substrate surface, whether it be paper, corrugated cardboard, flexible plastic films, or metallic foils. After printing, the resin undergoes a physical drying or chemical curing process to form a durable, continuous film.

Synthesized from both natural sources (such as pine rosin) and synthetic chemicals (such as acrylics, polyurethanes, and epoxies), ink resins dictate the fundamental properties of the final ink formulation. They directly influence the ink's rheology (flow behavior), viscosity, color brilliance, scratch resistance, chemical durability, and compatibility with specific printing processes like flexography, gravure, offset, or digital inkjet printing.

Market Drivers

The primary driver accelerating the Ink Resins Market is the massive global expansion of the flexible packaging and labeling sectors. The rise of packaged food and beverages, pharmaceuticals, and consumer goods requires high-quality, vibrant, and food-safe printing. Because flexible packaging relies heavily on non-porous plastic substrates like polyethylene and polypropylene, specialized resins—particularly polyurethanes and modified acrylics—are in high demand to ensure deep adhesion, heat resistance, and moisture barriers during sterilization and transport.

Furthermore, the explosive growth of the global e-commerce logistics sector is creating a sustained demand for corrugated box and containerboard printing. Corrugated shipping boxes require high-volume, cost-effective flexographic printing inks. This has significantly boosted the procurement of water-based acrylic resins, which offer excellent color transfer, fast drying times on porous cardboard, and easy press cleanup, maximizing throughput for high-volume packaging manufacturers.

Additionally, rigid environmental mandates targeting VOC emissions act as a powerful catalyst for market re-engineering. Traditional solvent-borne ink systems release significant chemical vapors during the drying process, attracting heavy regulatory penalties and carbon taxes. Consequently, printing ink formulators are aggressively adopting water-soluble resins and UV-curable oligomers, which drastically reduce or entirely eliminate VOC emissions, helping commercial printers comply with regional environmental standards.

Market Segmentation

By Resin Type

- Acrylic Resins

- Polyurethane Resins

- Polyamide Resins

- Modified Rosins / Rosin Esters

- Epoxy Resins

- Cellulosic and Others

By Technology

- Water-Based Resins

- Solvent-Based Resins

- UV-Curable / Energy-Curable Resins

- Oil-Based Resins

By Printing Process

- Flexography

- Gravure

- Offset / Lithography

- Digital / Inkjet

By Application

- Flexible Packaging

- Corrugated Boxes & Cartons

- Publications & Commercial Printing

- Labels & Tags

- Industrial & Textile Printing

The acrylic and polyurethane resin segments collectively capture the largest share of global market revenue due to their versatile application profiles and excellent compatibility with water-borne systems. Flexography remains the dominant printing process segment, closely tied to the massive output of flexible packaging and corrugated boxes. Meanwhile, the UV-curable technology segment represents the fastest-growing technology pocket, fueled by the rising adoption of digital inkjet printing and instant-dry commercial labels.

Regional Insights

- Asia-Pacific commands the largest and fastest-growing market share for ink resins globally. This dominant position is fueled by explosive manufacturing expansion, rapid urbanization, and a massive consumer base driving packaging demand across China, India, Japan, and Southeast Asia.

- North America holds a highly sophisticated, high-value market position. Growth in this region is anchored by an advanced e-commerce logistics infrastructure, strong demand for premium retail packaging, and a highly mature regulatory environment that favors advanced UV-curable and water-based resin systems.

- Europe maintains a significant market share, strongly defined by pioneering sustainability initiatives, circular economy directives, and strict European Printing Ink Association (EuPIA) guidelines that severely restrict hazardous chemical use in food-contact packaging.

- Middle East & Africa and South & Central America are exhibiting steady infrastructure and economic development, supported by expanding food-processing sectors, localized packaging facilities, and rising investments in commercial printing technologies.

Top Players in the Ink Resins Industry

The global marketplace features intense competition among diversified chemical multinational corporations and specialized polymer manufacturers. Key industry participants prioritize vertical integration, backward integrating into raw monomer production to safeguard supply chains against fluctuating petrochemical prices.

- BASF SE

- Dow Inc.

- Evonik Industries AG

- DIC Corporation (Sun Chemical)

- Lawter Inc. (Harima Chemicals)

- Arakawa Chemical Industries, Ltd.

- Kraton Corporation

- Covestro AG

- Mitsui Chemicals, Inc.

- Resonac Holdings Corporation

These market leaders maintain their dominance by establishing long-term supply agreements with global ink giants like Flint Group and Siegwerk, while continuously acquiring boutique regional resin manufacturers to expand their localized product portfolios.

Technological Innovations

Technological innovations in Bio-Based and Renewable Resins are fundamentally transforming the industry's carbon footprint. Historically, synthetic ink resins have been derived almost exclusively from fossil-fuel-based petrochemical monomers. Next-generation resins leverage renewable feedstocks such as soy, corn, tall oil, and modified natural pine rosins. These bio-renewable resins deliver equivalent performance characteristics to petroleum-based acrylics while enabling ink formulators to market carbon-neutral products to environmentally conscious brands.

Furthermore, the advancement of High-Performance Water-Borne Polyurethane Dispersions (PPDs) is solving a critical industry hurdle: printing on non-porous films. Water-based inks traditionally struggled with adhesion and water resistance when applied to plastic packaging films. New PPD chemistry utilizes advanced molecular cross-linking that triggers during the drying phase, creating an incredibly tough, water-resistant, and flexible film layer that perfectly mimics the durability of legacy solvent-based systems.

Additionally, the development of Low-Migration UV-Curable Resins is revolutionizing food and pharmaceutical packaging safety. Standard UV inks can sometimes leave unreacted monomers that migrate through packaging layers and contaminate products. Innovative low-migration oligomers feature high molecular weights and self-initiating structures that ensure complete, instantaneous polymer cross-linking under UV light, completely eliminating chemical migration risks and satisfying the most stringent food safety regulations.

Future Market Outlook

The long-term outlook for the Ink Resins Market remains robust and highly stable. As international consumer product brands transition toward fully recyclable and compostable packaging structures, the ink industry must follow suit. Resin manufacturers who succeed in engineering fully water-soluble or compostable binders that do not interfere with plastic and paper recycling streams will capture a decisive competitive advantage.

The continuing shift toward digital inkjet printing for short-run, highly customized commercial packaging will ensure a lucrative, high-margin revenue stream for advanced, ultra-low-viscosity monomer and oligomer chemistry. Organizations that blend agile R&D with sustainable chemical synthesis will solidify their leadership in the global printing materials ecosystem.

Frequently Asked Questions (FAQs)

What is the primary function of a resin in a printing ink formulation?

The primary function of a resin is to act as a binder or vehicle. It encapsulates the pigment particles to keep them evenly dispersed, carries the ink through the printing press mechanics, and ultimately adheres the pigment permanently to the substrate surface by forming a durable plastic-like film layer as it dries or cures.

Why is the market transitioning from solvent-based to water-based and UV-curable resins?

The transition is primarily driven by strict environmental regulations and workplace safety standards. Solvent-based resins release high amounts of Volatile Organic Compounds (VOCs) during evaporation, which contribute to air pollution and present health risks to press operators. Water-based and UV-curable resins rely on water or light-induced polymerization, drastically reducing chemical emissions and lowering fire hazards.

What are "low-migration" resins, and why are they critical for food packaging?

Low-migration resins are specially engineered polymers designed to prevent residual chemical compounds from passing through packaging materials into food, beverages, or medicines. They are critical because normal, unreacted ink monomers can alter the taste, odor, or chemical safety of a packaged product, violating rigid international consumer health protection laws.

How do rosin-based resins differ from acrylic resins?

Rosin-based resins are derived from natural pine tree secretions and modified chemically; they are cost-effective and heavily used in traditional offset or gravure printing for publications. Acrylic resins are fully synthetic polymers that offer superior clarity, chemical resistance, UV stability, and versatility, making them the preferred choice for modern high-end water-based flexographic inks and digital inkjet systems.

Browse More Reports:

https://www.businessmarketinsights.com/reports/process-instrumentation-market

https://www.businessmarketinsights.com/reports/protective-gloves-market

https://www.businessmarketinsights.com/reports/pu-sole-footwear-polyurethane-market

About Us

Business Market Insights is a market research platform that provides a comprehensive subscription service for targeted industry and company intelligence reports. Our research team has extensive professional expertise across dynamic industrial domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications.

Contact Us

If you have any questions about this report or would like further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070

Categorie

Leggi tutto

Regional Overview of Executive Summary Autologous Fat Grafting Market by Size and Share The global Autologous Fat Grafting market size was valued at USD 1.41 billion in 2024 and is expected to reach USD 2.99 billion by 2032, at a CAGR of 9.80% during the forecast period. Deliberately analysed facts and figures of the market and keen business insights...

Gloves Market : According to the latest report published by Data Bridge Market Research, the Gloves Market The global Gloves market size was valued at USD 26.96 billion in 2024 and is expected to reach USD 55.33 billion by 2032, at a CAGR of 9.40% during the forecast period The market growth is largely fueled by the rising demand for personal protective...

" Emollient Esters Market Summary: According to the latest report published by Data Bridge Market Research, the Emollient Esters Market The global emollient esters market is expected to reach USD 801.38 million by 2032 from USD 576.76 million in 2024, growing with a substantial CAGR of 4.30% in the forecast period of 2025 to 2032. Emollient Esters Market analysis report contains...

Global Executive Summary Pet Food Additives Market: Size, Share, and Forecast CAGR Value The pet food additives market is expected to witness market growth at a rate of 7.3% in the forecast period of 2022 to 2029. To gain meaningful market insights and thrive in this competitive market place, Pet Food Additives Market survey report plays a key role. The report takes into account the...

Orlando is one of the most popular trade show destinations in the United States, drawing thousands of exhibitors annually from various industries, such as tourism, healthcare, technology, education, hospitality and entertainment. The Orange County Convention Center is one of the world's top convention facilities, attracting businesses from all over to display their products and services. With...