Commercial Helicopters Market Insights for Operators, OEMs, Lessors, and Service Providers

The Commercial Helicopters Market serves a diverse range of civil and parapublic missions, including emergency medical services, offshore transport, law enforcement support, firefighting, tourism, corporate travel, utility inspection, search and rescue, agriculture, aerial work, and passenger mobility in remote regions. Helicopters remain essential where vertical lift, hover capability, rapid deployment, and access to confined or difficult terrain are required. Market demand is influenced by fleet replacement, safety upgrades, offshore energy activity, medical transport needs, public safety budgets, tourism recovery, and infrastructure inspection requirements. Operators are prioritizing aircraft with improved fuel efficiency, mission flexibility, avionics capability, lower maintenance burden, and better dispatch reliability.

Industry Size and Market Structure

Industry size and market structure include helicopter OEMs, engine suppliers, avionics providers, leasing companies, MRO organizations, mission equipment integrators, operators, training providers, and aftermarket parts suppliers. The market is capital-intensive and highly regulated, with purchasing decisions based on mission profile, payload, range, cabin configuration, operating cost, safety systems, certification, resale value, and support network. Light helicopters serve training, tourism, patrol, and private uses, while medium and heavy helicopters support EMS, offshore transport, firefighting, utility lifting, and specialized missions. Aftermarket services represent a major revenue stream because airworthiness, maintenance, upgrades, and parts availability are critical throughout aircraft life.

Key Growth Trends Shaping 2025–2034

Key growth trends shaping 2025-2034 include fleet modernization, adoption of advanced avionics, increased use of helicopters in emergency and public safety services, and demand for mission-specific interiors and equipment. Offshore wind and energy infrastructure inspection are creating new opportunities alongside traditional oil and gas transport. Operators are also evaluating lower-emission propulsion pathways, sustainable aviation fuel compatibility, hybrid-electric concepts, and eventually advanced air mobility interfaces. Digital maintenance, health usage monitoring systems, and predictive analytics are becoming important to reduce downtime. Over the forecast horizon, helicopters with strong lifecycle economics, flexible configurations, and robust support ecosystems will be preferred.

Core Drivers of Demand

Core drivers of demand include emergency medical transport requirements, offshore energy logistics, tourism and charter activity, law enforcement modernization, disaster response, and infrastructure inspection. Remote geographies and difficult terrain continue to support demand in mining, utilities, and public services. Replacement of aging fleets creates opportunities for safer, quieter, and more efficient platforms. Government and private-sector mission outsourcing also supports operator demand. Residual value protection will remain central to operator investment confidence.

Challenges and Constraints

Challenges and constraints include high acquisition cost, pilot shortages, maintenance expense, safety risk management, fuel cost volatility, regulatory compliance, and sensitivity to economic cycles. Offshore demand can fluctuate with energy investment, while tourism depends on consumer travel trends. Noise restrictions and community acceptance can limit operations in urban areas. Emerging eVTOL technologies may influence selected short-distance missions over the long term, although operational certification and infrastructure remain key hurdles.

Browse more Information:

https://www.oganalysis.com/industry-reports/commercial-helicopters-market

Segmentation Outlook

Segmentation outlook covers commercial helicopters by type, including light, medium, and heavy helicopters; single-engine and twin-engine platforms; and turbine-powered models for mission-specific use. By application, the market includes EMS, offshore transport, corporate and VIP travel, tourism, law enforcement, firefighting, search and rescue, utility work, agriculture, training, and aerial surveying. End users include helicopter operators, governments, hospitals, energy companies, tourism providers, corporations, utilities, and public safety agencies. Revenue streams include new aircraft sales, leasing, retrofit, MRO, training, and mission equipment integration.

Regional Dynamics

Regional dynamics show North America as a major market due to EMS networks, public safety fleets, offshore operations, corporate aviation, and mature MRO infrastructure. Europe benefits from strong OEM presence, offshore wind growth, EMS services, and regulatory modernization. Asia-Pacific offers long-term growth through infrastructure development, tourism, public safety investment, island connectivity, and utility missions. Middle East and Africa demand is linked to oil and gas, VIP transport, emergency services, and remote-area operations. South and Central America presents opportunities in EMS, energy, mining, law enforcement, and tourism-related flying. Demand analysis should also consider aftermarket intensity, because helicopters require continuous inspection, component replacement, pilot training, and mission equipment upgrades. Operators often make fleet decisions based on support responsiveness and aircraft availability, not only payload or range. OEMs with strong service networks, financing options, and upgrade pathways will remain well positioned as customers extend asset life and modernize selectively.

Key Market Players

· Airbus Helicopters

· Bell Textron Inc.

· Leonardo S.p.A.

· Sikorsky

· Robinson Helicopter Company

· MD Helicopters

· Enstrom Helicopter Corporation

· Korea Aerospace Industries

· Hindustan Aeronautics Limited

· Kopter Group

Competitive Landscape and Forecast Perspective (2026–2034)

Competitive landscape and forecast perspective for 2026-2034 indicate competition across aircraft performance, safety systems, operating cost, support network, and mission adaptability. OEMs are expected to strengthen aftermarket services, digital maintenance tools, training support, and customized mission packages. Operators will increasingly evaluate total cost of ownership rather than acquisition price alone. Market growth will be strongest where helicopters remain essential to emergency response, offshore logistics, remote connectivity, and high-value utility missions. From a planning standpoint, OEMs and operators should focus on mission economics, availability, and safety performance. Buyers are increasingly interested in platforms that can be reconfigured across missions, supported by strong parts networks, and monitored through digital maintenance systems. Leasing, retrofit, and MRO strategies will remain important as operators manage capital constraints and fleet renewal timing. Mission equipment integration, simulator-based training, and operational data analytics will further shape fleet decisions over the forecast period.

Browse Related Reports:

https://www.oganalysis.com/industry-reports/offshore-mooring-systems-market

https://www.oganalysis.com/industry-reports/aircraft-turbofan-engine-market

https://www.oganalysis.com/industry-reports/more-electric-aircraft-market

https://www.oganalysis.com/industry-reports/antiice-valves-market

https://www.oganalysis.com/industry-reports/landing-gear-control-systems-market

الأقسام

إقرأ المزيد

Oral health is not just about fixing problems when they arise. The most effective way to maintain a healthy, confident smile is through consistent preventive care. Preventive Dentistry Westlake Village focuses on stopping dental issues before they become painful, costly, or complex. By taking a proactive approach, individuals and families can enjoy better long-term oral health, fewer...

For those who rely on their Ute for both work and adventure, adding a high-quality Canopy for Ute from EZ Toolbox is a game-changer. Combining rugged durability with smart design, these aluminium canopies redefine practicality and protection for any lifestyle. Whether you’re a tradesperson transporting valuable tools or an outdoor enthusiast carrying camping gear, this canopy ensures your...

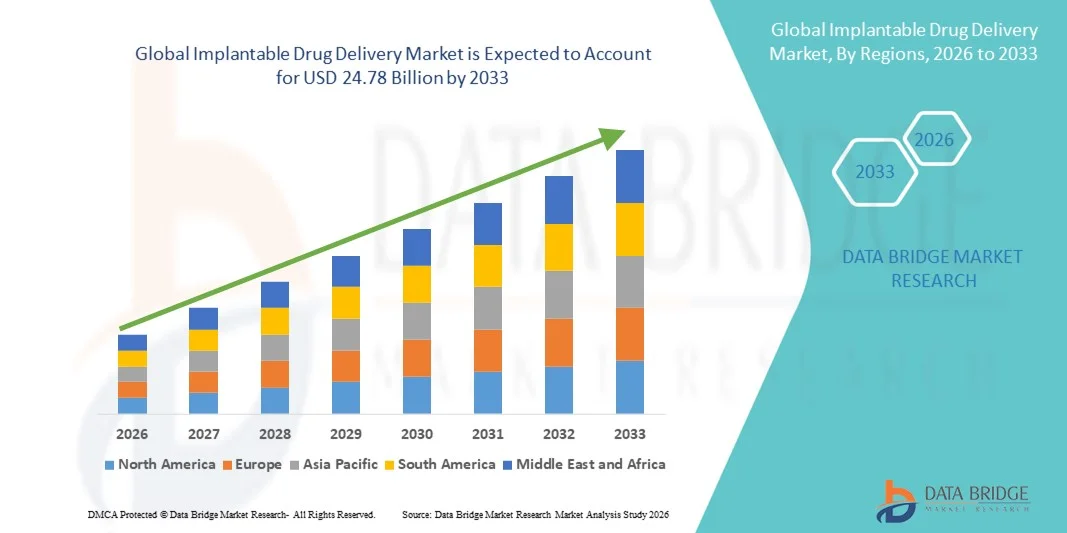

"Implantable Drug Delivery Market Summary: According to the latest report published by Data Bridge Market Research, the Implantable Drug Delivery Market The global implantable drug delivery market size was valued at USD 13.29 billion in 2025 and is expected to reach USD 24.78 billion by 2033, at a CAGR of 8.10% during the forecast period The comprehensive...

The Global Biocomposites Market, valued at USD 32.59 billion in 2023, is projected to reach USD 122.22 billion by 2032, expanding at a CAGR of 15.8% between 2024 and 2032. Growth is driven by rising demand for eco-friendly materials, sustainability-focused manufacturing, and increasing use in automotive, construction, and consumer goods industries. Biocomposites, made from natural or...

Dental health plays a crucial role in overall well-being, and missing teeth can significantly impact both function and confidence. Many people seeking long-term solutions for tooth loss turn to Dental Implants in Dubai. These implants offer a permanent replacement option that restores chewing ability, preserves facial structure, and enhances aesthetics. However, before proceeding, a common...