Mapping the Competitive Landscape: Understanding Assistive Technology Market Share Distribution

The distribution of Assistive Technology Market Share is not uniform across the industry but varies dramatically depending on the specific product segment being examined. It is a market of contrasts, with some areas being highly consolidated and others remaining remarkably fragmented. A prime example of consolidation is the global hearing aid market. This lucrative segment is dominated by a small number of powerful multinational corporations, often referred to as the "Big Five": Sonova, Demant, WS Audiology, GN Store Nord, and Starkey. Together, these companies control an overwhelming majority of the global market share, estimated to be over 90%. Their dominance is built on extensive patent portfolios, massive investments in research and development, global manufacturing and distribution networks, and strong relationships with audiology professionals. This high concentration creates significant barriers to entry for new players and allows the incumbents to command premium prices for their technologically advanced products, shaping the dynamics of the entire hearing care industry.

In stark contrast to the consolidated hearing aid segment, the market for mobility aids presents a much more fragmented picture. While there are certainly large, recognizable international brands that hold significant market share—such as Invacare Corporation, Pride Mobility Products, and Sunrise Medical—this sector also supports a vast number of smaller, regional, and local manufacturers. This fragmentation is driven by several factors. The need for customization is paramount, as wheelchairs and scooters often need to be adapted to an individual's specific physical needs and environment. This favors manufacturers who can offer personalized solutions and responsive local service and repair, areas where smaller, more agile companies can excel. Furthermore, the product range is incredibly diverse, from simple, low-cost walkers to complex, high-end powered wheelchairs, allowing numerous companies to carve out profitable niches. The logistics of shipping bulky equipment also provides a natural advantage to local and regional players, contributing to a landscape where market share is more evenly distributed among a wider array of competitors.

The market share dynamics within the emerging and rapidly evolving segments, such as assistive software, vision aids, and communication devices, are particularly fluid and interesting. These areas are hotbeds of innovation, often characterized by a dynamic struggle between established hardware manufacturers and nimble software startups. For instance, in the blind and low-vision segment, traditional manufacturers of hardware magnifiers and Braille displays now compete with software companies offering screen readers and mobile apps that run on mainstream devices. In this space, the concept of market share is complicated by the influence of technology giants like Apple, Google, and Microsoft. By building robust and free accessibility features directly into their operating systems (e.g., VoiceOver, TalkBack, Narrator), these companies have captured an enormous "user share," even if they don't directly sell assistive devices. Their influence is disruptive, setting a high bar for functionality and putting pressure on specialized AT companies to provide significant added value to justify their cost.

Companies within the assistive technology space employ a variety of strategic maneuvers to capture and expand their market share in this competitive environment. Mergers and acquisitions (M&A) are a common strategy, particularly in consolidated segments like hearing aids, where large players frequently acquire smaller companies to gain access to new technologies, expand their product portfolios, or enter new geographic markets. A relentless focus on research and development (R&D) is another critical strategy, as launching innovative products with unique features is a key way to differentiate from competitors and command premium pricing. Building and maintaining strong distribution channels and relationships with key prescribers, such as therapists and audiologists, is essential for reaching end-users and building brand loyalty. More recently, direct-to-consumer (DTC) marketing and branding efforts have become increasingly important, as companies seek to connect directly with empowered consumers who are actively researching solutions online, aiming to build brand recognition and trust outside of traditional clinical channels.

Top Trending Reports:

Broadcast Scheduling Software Market

Catégories

Lire la suite

In an increasingly interconnected world, the ability to transfer money quickly, safely, and at competitive rates is more critical than ever. For individuals and businesses alike, finding a reliable financial service provider can be a daunting task. Radhe Exchange emerges as a platform dedicated to simplifying the complexities of international money transfers and currency exchange. By...

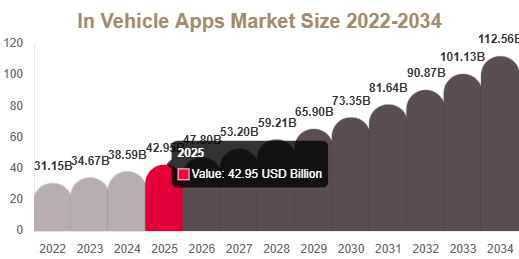

In Vehicle Apps Market Overview Market Overview The in vehicle apps market is experiencing rapid growth driven by the increasing adoption of connected vehicles, rising demand for advanced infotainment systems, and growing integration of digital ecosystems within automobiles. In vehicle apps include navigation systems, entertainment platforms, vehicle diagnostics, voice assistants, communication...

https://expediaonline1.blogspot.com/2026/06/expedia-multi-city-flight-booking-1-866_01740069879.html https://anandtraders1119.wixsite.com/engaging-insights-bl/post/expedia-multi-city-flight-booking-1-866-855-0041-1 https://www.boycat.co/blogs/146295/Expedia-Multi-City-Flight-Booking-1-866-855-0041 https://pastelink.net/mk7semn0...

Sunwin là nền tảng giải trí trực tuyến hiện đại, được sở hữu hợp pháp bởi Amadeus Technology B.V. – doanh nghiệp đăng ký theo luật pháp Curaçao (số đăng ký 164694), địa chỉ tại Chuchubiweg 17, Curaçao. Trong hệ sinh thái này, Sunwin.free là site chủ quản trực tiếp vận hành các...

Have you ever thought about how your chosen cover actually gets made? For those invested in their bike’s long-term condition, knowing a bit about what goes on behind the scenes can be helpful. When you look at Motorcycle Covers, consider them the end result of processes implemented by Motorcycle Cover Manufacturers—and those processes influence performance and durability. In...