Pre-Authorisation Process: Understanding Approval Requirements

Managing healthcare for family members back home or preparing for your own medical needs during visits to India requires robust financial planning. While choosing an extensive policy is the initial step, securing seamless care hinges on understanding the procedural mechanics of the insurer. The pre-authorisation process stands as the critical gatekeeper for cashless hospitalisation, ensuring that medical expenses are verified and approved before treatment begins.

For Non-Resident Indians (NRIs) navigating a cross-border setup, this administrative milestone demands specific attention. Missteps or documentation gaps can convert a seamless cashless experience into an unexpected, stressful out-of-pocket expense. Navigating the regulatory landscape of pre authorization health insurance nri requirements is essential to ensure that your policy delivers maximum utility when it matters most.

The Strategic Role of Pre-Authorisation in Indian Healthcare

Pre-authorisation is an evaluation framework where the insurance provider (or their designated Third-Party Administrator, known as a TPA) reviews the clinical necessity and coverage eligibility of a proposed treatment before hospital admission. This process confirms whether the specific medical procedure aligns with the policy terms, active sub-limits, and waiting periods.

For global citizens utilising NRI health insurance, pre-authorisation serves multiple critical operational functions:

-

Financial Predictability: It provides a clear, itemized breakdown of approved costs vs. co-payments, minimizing the risk of partial claim settlement or surprise billing at the time of discharge.

-

Validation of Coverage: It verifies that the planned treatment does not fall under standard policy exclusions, permanent caps, or incomplete waiting periods for pre-existing conditions (PECs).

-

Direct Settlement Activation: Successful pre-approval activates the cashless facility. This establishes a direct financial pipeline between the insurance provider and the network hospital, sparing families the burden of mobilizing large sums of emergency liquidity.

Step-by-Step Pre-Authorisation Framework

The pre-authorisation workflow fundamentally bifurcates depending on whether the medical admission is planned in advance or arises from an unforeseen emergency.

1. Planned Hospitalisation

For scheduled procedures—such as joint replacements, cataract surgeries, or elective treatments—the pre-authorisation request should ideally be initiated 48 to 72 hours prior to the scheduled admission.

-

The Workflow: The patient visits the hospital's dedicated insurance desk with the doctor’s recommendation. The hospital fills out 'Part B' of the pre-authorisation form, while the policyholder completes 'Part A'.

-

The Benefit: This window provides the insurer's medical underwriting team adequate time to evaluate historical medical records, verify policy continuity, and clear any queries without delaying the actual medical procedure.

2. Emergency Hospitalisation

In the event of an emergency admission—such as sudden cardiac events, accidents, or acute illnesses—medical care takes absolute priority.

-

The Workflow: The patient is admitted immediately to stabilize their condition. The hospitalisation protocol allows the network hospital's corporate cell or insurance desk to submit the pre-authorisation form within 24 hours of admission.

-

The Benefit: This grants retroactive cashless approval. While the initial stabilization might require a nominal security deposit to the hospital, it is fully refunded once the TPA issues the initial authorization letter.

Essential Documentation for Smooth Approvals

To avoid administrative delays or repeated iterations with the insurer, specific documentation must be presented at the network hospital's cashless desk. When coordinating care remotely for aging dependents, ensuring these documents are pre-compiled and digitally accessible is vital.

📋 The Core Document Checklist

-

Health Insurance Card: The digital e-card or a physical copy containing the active policy number, member ID, and corporate buffer details (if applicable).

-

Valid Identity Proof: Government-issued identification of the patient to verify age and relationship to the primary policyholder (e.g., PASSPORT, PAN card, or Voter ID).

-

First Consultation Note: The official prescription and clinical notes from the treating doctor explicitly advising hospitalisation and outlining the history of the ailment.

-

Diagnostic Reports: All relevant laboratory tests, radiology reports (such as MRI, CT scans, or X-rays), and histopathology findings supporting the final diagnosis.

-

Detailed Cost Estimate: An itemised billing projection provided by the hospital's billing department, explicitly breaking down room rent, OT charges, surgeon fees, and implant costs.

Why Pre-Authorisation Requests Face Delays or Rejections

Understanding the common triggers for administrative friction allows policyholders to mitigate risks before checking into a healthcare facility.

Incomplete Medical History Disclosures

Incurred claim reviews place significant weight on historical medical tracking. If the pre-authorisation medical notes indicate a chronic condition (like hypertension or diabetes) that was not disclosed during the policy inception or renewal, the insurer may halt the cashless approval. The case is then pending a detailed verification of the policyholder's historical health data, which can delay approvals by several days.

Mismatch in Clinical Treatment Coding

Insurers utilise standardised medical codes (such as ICD-10 formatting) to evaluate procedures. If there is an inconsistency between the declared diagnosis and the planned surgical or therapeutic line of treatment, the pre-authorisation request will face queries. For instance, if a diagnostic report does not strongly justify an aggressive surgical intervention according to standard medical guidelines, the underwriting team will demand further clinical justification.

Room Rent Capping and Sub-Limits

If a policyholder selects a hospital room category higher than their eligible entitlement (e.g., choosing a private deluxe room when the policy only covers a twin-sharing room), the initial approval will be capped. Crucially, this often triggers a proportionate deduction penalty across the entire hospital bill—including surgeon fees and operation theatre charges—requiring the patient to clear the steep variance entirely out-of-pocket during final discharge.

Managing Cross-Border Claims Remotely: The Digital Advantage

Modern healthcare administration allows non-resident individuals to manage the end-to-end claim ecosystem digitally. When maintaining an active NRI Health Insurance policy for parents or family members in India, your physical presence is no longer a prerequisite for managing hospitalisation workflows.

Leading Indian insurance providers offer integrated digital portals and dedicated helplines designed specifically for overseas policyholders. Companies like Niva Bupa, Care Health, and Star Health provide comprehensive digital e-cards and real-time claim tracking applications. These tools allow you to:

-

Monitor pre-authorisation approvals in real-time.

-

View and directly upload documents to resolve outstanding queries from the TPA.

-

Review final settlement sheets from any location globally.

Proactive Steps for NRIs

To optimise the pre authorisation health insurance nri process from abroad, it is highly recommended to identify two or three preferred network hospitals in your family's residential city before any medical need arises.

Familiarising your dependents with the exact location of the hospital’s internal insurance desk, keeping a shared cloud folder of their medical history, and understanding your TPA’s turnaround time ensures that when a medical need occurs, the transition from consultation to approved inpatient care remains entirely seamless.

Categorie

Leggi tutto

Building a strong brand isn’t just about ads or posts—it’s about trust. When people feel genuinely connected to your brand, they don’t just follow you; they believe in you. Understanding the Real Challenge Most businesses know that social media is powerful—but few truly understand how to use it effectively. Many owners spend hours posting daily, expecting quick...

Top VPN Alternatives in 2023 Exploring Top VPN Alternatives to CyberGhost in 2023 While CyberGhost delivers impressive server speeds and an extensive network, you might find it doesn't perfectly align with your specific needs. Whether you're struggling with its censorship evasion capabilities or looking for different features, several excellent alternatives exist in today's competitive VPN...

Dubai is renowned for its luxurious lifestyle, modern skyline, and vibrant entertainment scene, making it a top destination for visitors seeking companionship. Among the most sought-after companions are Indian escorts, celebrated for their elegance, charm, and professional approach. Based on customer reviews, the top 20 Indian Escorts in Dubai stand out for providing exceptional services that...

The global healthcare industry is placing increasing emphasis on patient safety, hospital hygiene, and contamination control. Within this context, critical areas such as medical equipment sterilization, endoscope reprocessing market growth, and infection prevention solutions are becoming essential components of modern clinical workflows. These segments collectively support the expansion of the...

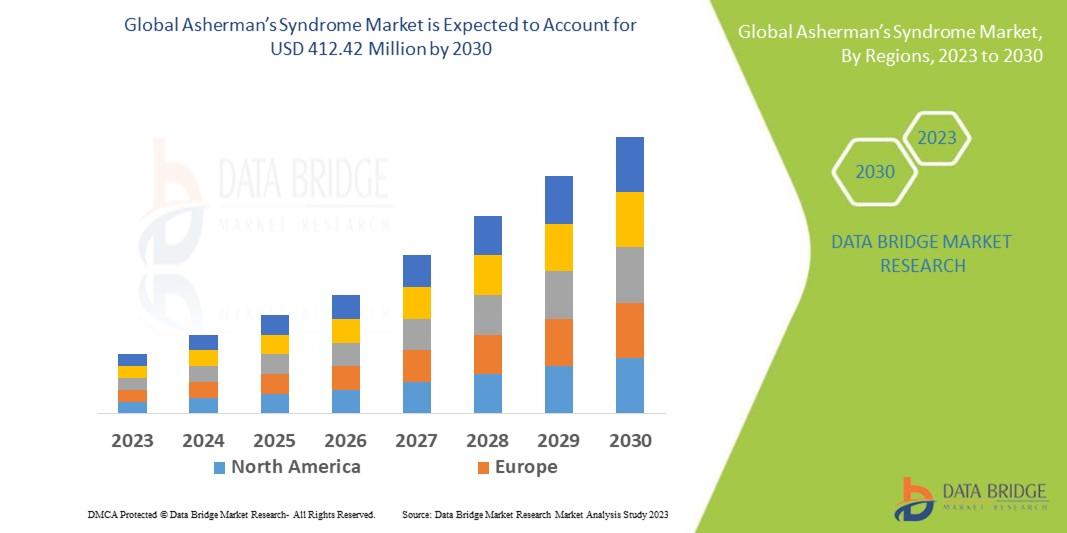

<strong> Asherman?s Syndrome Market </strong><p id=subheading_0><strong>According to the latest report published by Data Bridge Market Research, </strong>the<strong><a href=https://www.databridgemarketresearch.com/reports/global-ashermans-syndrome-market> Asherman?s Syndrome Market</a></strong></p><b>...