Examining The Global Competitive Landscape And Trends Within Generative AI in Coding Market Share

The competitive distribution of market share in the global generative AI coding sector reflects the intense competition among technology giants with vast resources and established developer platform relationships, well-funded AI startups with specialized technical capabilities, and emerging open-source alternatives that are challenging proprietary tools with freely available alternatives. A thorough examination of the Generative AI in Coding Market share reveals that market leadership is being contested across multiple dimensions simultaneously—model quality as measured by developer-reported code suggestion acceptance rates, IDE integration breadth that determines which developer workflows the tool can serve, enterprise security capabilities that satisfy organizational risk requirements, and pricing models that create favorable unit economics for both providers and buyers.

Geographically, market share reflects the distribution of global software development activity and varying enterprise AI adoption maturity. North America maintains the largest market share driven by the concentration of major technology companies, enterprise software organizations, and startups that represent the most intensive software development activity and the highest AI tool adoption propensity globally. Europe represents the second largest segment, where enterprise adoption is increasingly influenced by AI regulatory requirements under the EU AI Act that may create compliance obligations for AI coding tools deployed in certain contexts. The Asia-Pacific region, particularly China, Japan, South Korea, and India's massive software development sector, represents a rapidly growing market segment where both global AI coding platforms and domestically developed alternatives are competing for market share.

The influence of developer platform ecosystem relationships on AI coding market share is particularly significant, as the most successful AI coding tools are those most deeply integrated within the development environments where developers spend the majority of their working time. GitHub's exceptional market position in developer collaboration creates powerful distribution advantages for GitHub Copilot, as the tight integration between Copilot and GitHub's code hosting, review, and CI/CD capabilities creates a seamless AI-enhanced development experience within the platform where millions of developers already work. Microsoft's simultaneous ownership of GitHub, Visual Studio Code, and Azure creates extraordinary opportunities for integrated AI coding assistance across the complete Microsoft developer ecosystem that independent AI coding competitors cannot replicate without equivalent ecosystem breadth.

Finally, the future of generative AI coding market share will be significantly influenced by the competitive dynamics around open-source AI coding models that are creating freely available alternatives to proprietary commercial tools. Open-source code generation models including Code Llama, StarCoder, and WizardCoder that approach commercial model performance while enabling deployment within enterprise infrastructure without sending code to external services are creating meaningful competitive pressure on commercial AI coding providers. Enterprise organizations with strong data privacy requirements or significant self-hosting infrastructure are increasingly evaluating open-source AI coding model deployment as an alternative to commercial subscriptions, creating market pressure that may accelerate commercial provider feature differentiation and pricing adjustments.

Top Report:

Categorie

Leggi tutto

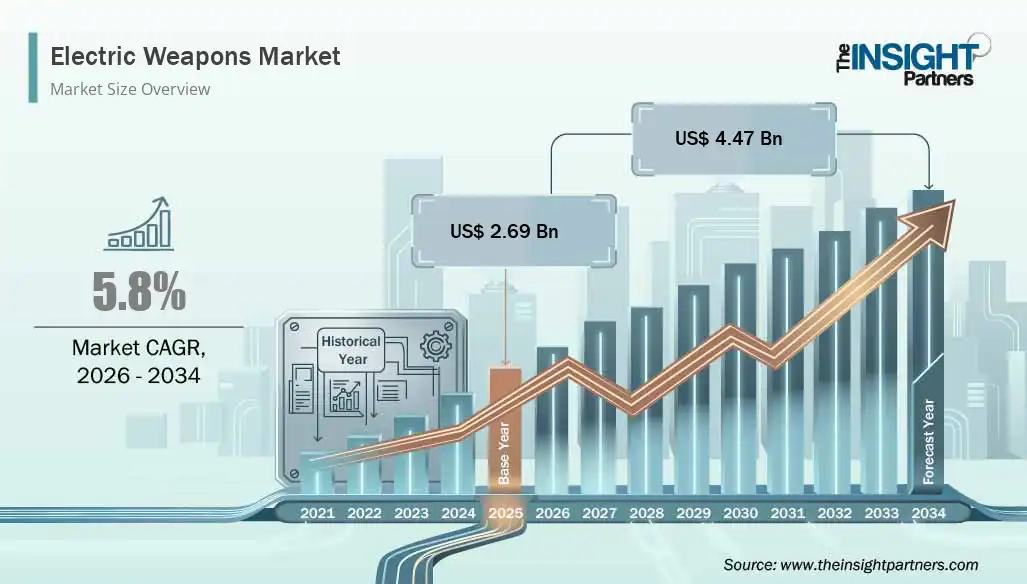

The electric weapons market is witnessing steady growth as defense agencies, law enforcement organizations, and security forces increasingly adopt advanced non-lethal and directed energy technologies. Electric weapons are designed to incapacitate or deter targets using electrical energy while minimizing permanent physical harm. These systems have gained considerable attention due to their...

Looking to make the most of the limited-time Oasis Riches solo event in Monopoly GO? Running from March 29 to April 1, this three-day event overlaps perfectly with the Desert Bloom Partners event, making it your best chance to stock up on Flower tokens while collecting a mountain of dice rolls. Event Highlights and Rewards Oasis Riches offers over 60 milestone rewards, with a total payout of...

According to the latest report published by Data Bridge Market Research, the Periodontal Disease Treatment Market Data Bridge Market Research analyses that the Periodontal disease treatment market which was USD 734.8 million in 2022, and would rocket up to USD 61,459.3 million by 2030, and is expected to undergo a CAGR of 9.2% during the forecast period. An influential...

"Innovating the Approach to Bumper Beam Market Bumper Beam Market Size was valued at USD 1.5 Billion in 2022. The Global Bumper Beam Industry is projected to grow from USD 1.6 Billion in 2023 to USD 2.2 Billion by 2032, exhibiting a compound annual growth rate (CAGR) of 4.20% during the forecast period (2023 - 2032). In today’s rapidly changing world, the Lightweight automotive...

In a world overflowing with digital messages and endless marketing noise, businesses need a smarter way to stand out. The moment a customer receives a professionally designed envelope, they form an opinion about the company behind it. That first impression can determine whether your communication gets opened immediately or ignored altogether. Professional envelope printing transforms ordinary...