Understanding the Risks: What Happens If You Can't Repay a Home Equity Loan?

Leveraging home equity is one of the most powerful mechanisms available to modern property owners. By converting the illiquid wealth built within a home's walls into immediate, low-interest capital, homeowners can consolidate debt, tackle major structural additions, or fund legacy-building investments. Because home equity loans are asset-backed financial instruments secured directly by real estate, lenders comfortably offer vastly superior rates compared to credit cards or personal loans.

However, that exact same security framework shifts the ultimate risk burden squarely onto the shoulders of the borrower. In the financial sector, there is no such thing as free flexibility. The low interest rates of a home equity loan are earned because you have signed over your primary residence as collateral. When unexpected life disruptions occur—such as sudden job losses, catastrophic medical events, or corporate business downturns—and regular monthly mortgage allocations stall, the consequences are severe. Understanding the chronological, structural, and legal cascade of what happens when you cannot repay a home equity loan is essential to protecting your property portfolio.

1. The Immediate Aftermath: Fees, Late Penalties, and Credit Impact

The journey toward default does not occur instantly; it begins the day a single monthly payment window closes without funding. Within 10 to 15 days of a missed deadline, lenders automatically assess late fees, which are added directly to your total outstanding balance.

Once a payment passes the critical 30-day delinquency threshold, the lender legally reports the default to the major credit bureaus (Equifax, Experian, and TransUnion). Because payment history represents the absolute heaviest component of your consumer credit calculation, a single 30-day late note on a mortgage product can trigger an immediate, devastating drop of 50 to 100 points in your credit score. This instantly compromises your ability to secure any future lines of credit, refinance existing obligations, or obtain competitive insurance premiums, sealing you outside standard commercial credit markets.

2. The Lien Hierarchy: The Reality of the Second Mortgage

To grasp the legal danger of a defaulted home equity loan, you must understand the mechanics of the "lien priority" framework. A home equity loan acts fundamentally as a second mortgage. The institutional bank that holds your primary purchase mortgage occupies the "first lien" position, while your home equity lender occupies the "second lien" position.

If you default on your home equity payments while continuing to pay your primary mortgage, the second lien holder retains the absolute legal right to initiate foreclosure independent of the first bank. However, during a foreclosure sale, the cash proceeds are legally required to satisfy the first mortgage holder completely before a single dollar flows to the home equity lender. Because of this subordinate status, if your home has lost value or if you hold thin equity margins, the second lender faces massive risk. This structural positioning drives them to pursue aggressive debt collection strategies to recover their outstanding capital before property valuations potentially drop.

3. The Legal Escalation: Acceleration and Foreclosure Proceedings

When delinquency stretches between 90 and 120 days, the loan officially transitions from simple delinquency into structural default. At this stage, the lender will typically execute an acceleration clause embedded deeply within the original promissory contract. Acceleration legally declares that the entire remaining balance of the loan—not just the past-due monthly payments—is due immediately in one lump sum.

If the borrower cannot satisfy the accelerated balance, the lender initiates formal foreclosure proceedings. Depending on the state where the property sits, this will follow either a judicial path (requiring court battles and a judge's direct decree) or a non-judicial path (executed rapidly via a trustee through public auction notices). The home is sold to the highest bidder at a public auction, completely stripping you of ownership, erasing your historical equity, and forcing an eviction from the premises.

The Post-Foreclosure Nightmare: Deficiency Judgments

Losing the home does not automatically erase the remaining debt. If the public foreclosure auction fetches a price that fails to fully cover the combined balances of both the first mortgage and the home equity loan, you face a "deficiency." In many jurisdictions, the home equity lender can sue you personally to obtain a deficiency judgment. This legal decree allows them to garnish your wages, place freezes on your personal bank accounts, and seize non-residential assets to satisfy the residual balance.

4. Proactive Defenses: Strategies to Avoid the Worst-Case Scenario

If you anticipate an impending financial crisis that will disrupt your payment capabilities, staying silent is a critical operational mistake. Lenders view proactive communication far more favorably than radio silence. Several mitigation strategies can be deployed before the legal machinery mobilizes:

Loan Modification Requests: Many institutions feature dedicated loss mitigation departments. If you can document a temporary financial hardship, the lender may agree to modify the loan terms permanently—extending the repayment timeline to lower monthly obligations, or temporarily reducing the interest rate to restore affordability.

Short Refinancing or HELOC Adjustments: If you possess exceptional personal credit but are facing an impending cash crunch, you may be able to transition the fixed debt into a revolving line of credit featuring initial interest-only payment structures, buying you temporary financial breathing room while you stabilize your primary income streams.

Pre-Emptive Market Sales: If the financial hardship is permanent and loan modification is mathematically impossible, the most pragmatic move is taking control of the asset liquidation yourself. Listing the property on the open market via a traditional real estate transaction allows you to sell the asset at fair market value, satisfy both the first and second mortgages completely on your own terms, and walk away with any remaining residual equity—preserving your credit score and avoiding the long-term stigma of a foreclosure mark.

A home equity loan is an incredibly efficient wealth-extraction engine, but it requires unwavering cash flow discipline. Treating your home’s equity not as disposable wealth, but as a serious, asset-backed obligation ensures that you balance the structural advantages of lower interest rates against the real-world operational risks of borrowing against the roof over your head.

Categorie

Leggi tutto

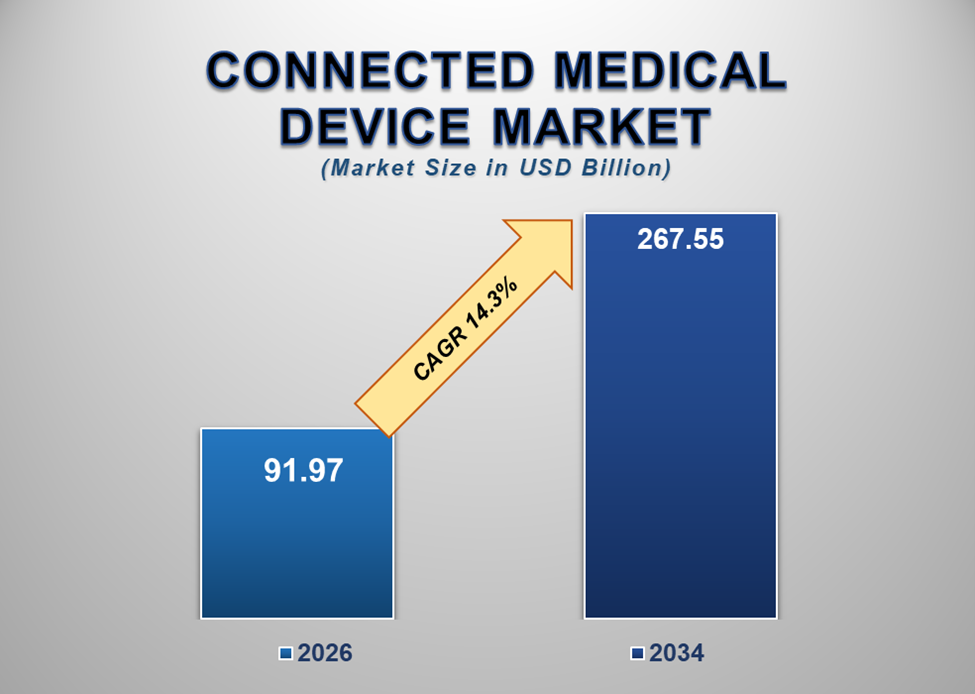

The Connected Medical Device Market Demand is rapidly transforming the global healthcare ecosystem by integrating advanced technologies such as IoT, artificial intelligence (AI), and cloud computing into medical devices. These smart devices enable real-time data collection, remote monitoring, and improved patient outcomes, making healthcare more efficient, personalized, and...

Global Tiki Torch Market Gains Momentum Amid Rising Outdoor Living and Decorative Lighting Trends The global tiki torch market is witnessing steady expansion as outdoor lifestyle trends, garden aesthetics, and decorative lighting solutions gain popularity across residential and commercial spaces. Consumers are increasingly investing in outdoor décor products that enhance...

The quality of fresh water around the world has become a critical topic of discussion for governments, municipal corporations, and individual homeowners alike. Industrialization, agricultural runoff, and aging municipal pipeline infrastructure have increasingly contributed to water contamination. In response, residential and commercial consumers are turning toward robust, comprehensive water...

Many students believe that becoming a pilot requires a strong technical background like computer science or engineering. This idea usually comes from how advanced modern aircraft look. The truth is much simpler. Your degree does not decide whether you can become a pilot. The aviation path is completely separate from your college specialization. If you have completed a degree in computer...

Um schneller an neue Karten im Pokémon Sammelkartenspiel Pocket zu gelangen, solltet ihr eine oft übersehene Funktion aktiv nutzen. Die tägliche Interaktion mit den öffentlichen Alben und Galerien anderer Spieler bringt euch wertvolle Shop-Tickets ein. Diese Tickets könnt ihr gegen Pack-Sanduhren eintauschen, die die Wartezeit auf das nächste Boosterpack...