A Strategic Deep Dive: A Comprehensive Virtual Router Market Analysis Today

A thorough strategic analysis of the virtual router market reveals a sector at the epicenter of the networking industry's most significant architectural shift in a generation: the move to software-defined everything. The market's core objective is to provide the agility and cost-efficiency of the cloud computing model to the world of network routing. A complete Virtual Router Market Analysis must acknowledge that this is not simply about replacing one type of router with another; it's about enabling a new, automated, and programmable way of building and operating networks. The dynamics of this market are shaped by the intense competition between established networking incumbents, who are transitioning their flagship operating systems to a virtualized form factor, and a host of software-centric challengers. Success in this space depends not just on the feature set of the vRouter itself, but on its performance, its integration with broader orchestration platforms (like SDN controllers and cloud management portals), and the strength of its ecosystem. Understanding the interplay of the technology's inherent strengths, its performance and security challenges, and the immense opportunities and threats it faces is critical for any enterprise or service provider navigating the transition to a virtualized network future.

SWOT Analysis: Inherent Strengths and Critical Weaknesses

The undeniable strength of the virtual router market lies in its ability to deliver unprecedented agility and cost savings. By decoupling routing software from proprietary hardware, organizations can dramatically reduce capital expenditures and shift to a more flexible, OpEx-based consumption model. The speed of provisioning—deploying a new router in minutes versus months—is a transformative strength that allows businesses to adapt quickly to changing demands. This software-based approach also enables a level of automation and centralized management that significantly improves operational efficiency. However, the market is not without its weaknesses. Performance has historically been a key concern. While modern servers and acceleration techniques have made significant strides, a software-based router running on a general-purpose CPU may not always match the raw, line-rate packet-forwarding performance of a physical router with dedicated ASICs (Application-Specific Integrated Circuits), especially for the most demanding core network applications. Another weakness is the potential skills gap. Managing a virtualized, software-defined network requires a different skillset, blending traditional networking knowledge with expertise in virtualization, software, and automation, which can be a barrier to adoption for some organizations.

SWOT Analysis: Massive Opportunities and Emerging Threats

The opportunities for the virtual router market are vast and expanding. The global rollout of 5G and the proliferation of edge computing represent a massive greenfield opportunity, as these distributed architectures require a lightweight, scalable, and easily deployable routing solution at thousands of new edge locations. The continued growth of SD-WAN as the default enterprise WAN architecture provides a steady and growing market for vRouters as virtual CPEs and cloud gateways. The rise of containerization also presents a major opportunity, with the evolution from Virtual Network Functions (VNFs) to Cloud-native Network Functions (CNFs) allowing for even more granular, efficient, and scalable deployments of virtual routing capabilities. Conversely, the market faces significant threats. Security is a primary concern; as with any software, vRouters can have vulnerabilities that could be exploited, and securing a distributed, virtualized environment can be more complex than securing a traditional, perimeter-based network. There is also a competitive threat from the major public cloud providers, whose own highly integrated, native networking services may be "good enough" for many cloud-centric use cases, potentially reducing the demand for third-party vRouter solutions within their ecosystems.

The Competitive Landscape: Incumbents vs. Challengers

The competitive landscape of the virtual router market is a dynamic arena where networking incumbents are adapting their business models to compete with software-first challengers. The established hardware giants like Cisco (with its CSR 1000V and Catalyst 8000V), Juniper Networks (with its vMX), and Nokia (with its Virtualized Service Router) hold a strong position. Their primary advantage is their vast installed base and the fact that their virtual routers run the same mature, feature-rich operating systems (IOS-XE, Junos, SR OS) that network engineers have trusted for decades. This provides a familiar management experience and ensures seamless interoperability with their existing physical networks. Competing with these giants are a number of other players, including pure-play software companies and open-source projects. For example, the Brocade Vyatta vRouter (now owned by Ciena) gained significant traction as a flexible, x86-native solution. Open-source projects like FRRouting provide a powerful, community-driven alternative for organizations with strong in-house development capabilities. The central battle in this market is between the proven stability and deep feature sets of the incumbents and the perceived agility and cost-effectiveness of their software-centric competitors.

Top Trending Reports:

Categorías

Read More

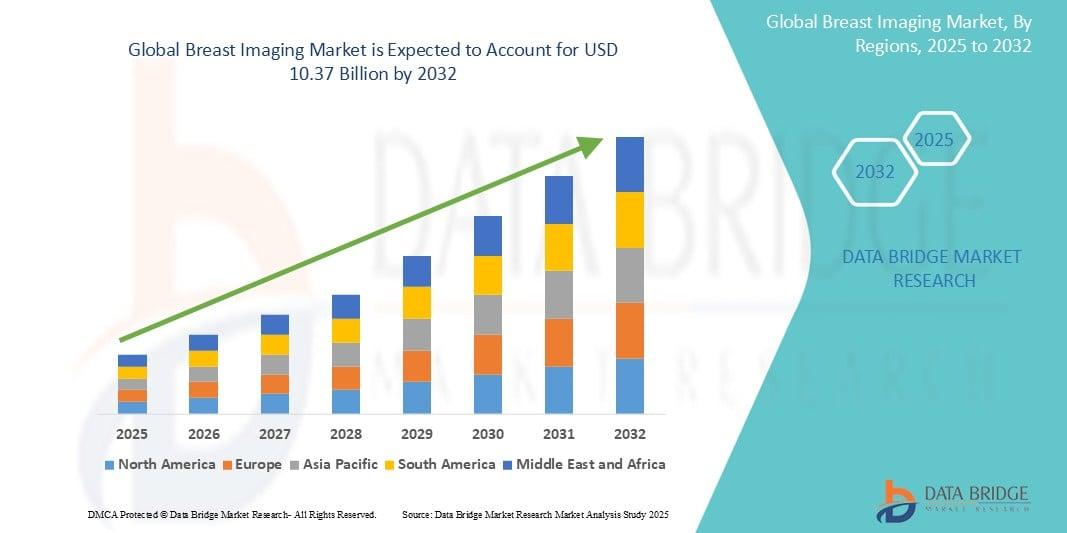

"Breast Imaging Market Summary: According to the latest report published by Data Bridge Market Research, the Breast Imaging Market The global breast imaging market size was valued at USD 5.21 billion in 2024 and is expected to reach USD 10.37 billion by 2032, at a CAGR of 8.97% during the forecast period This Breast Imaging Market research report also...

The global Carboprost Tromethamine Market continues to evolve as healthcare providers seek effective solutions for managing obstetric emergencies and improving reproductive healthcare outcomes. According to Polaris Market Research, the market is expected to reach USD 2,100.63 million by 2032, growing at a CAGR of 3.7% from 2024 to 2032. Rising investments in maternal healthcare, expanding...

"Executive Summary Acoustic Insulation Market Size and Share Analysis Report CAGR Value The global acoustic insulation market size was valued at USD 15.72 billion in 2024 and is expected to reach USD 22.89 billion by 2032, at a CAGR of 4.81% during the forecast period Acoustic Insulation Market report objective analysis is employed to make decisions...

A new growth forecast report titled Sepsis Diagnostics Market Size, Share, Trends, Industry Analysis Report: By Product (Instrument, Blood Culture Media, Assay Kits & Reagents, and Software), Technology, Testing Type, End User, Pathogen, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) – Market Forecast, 2025–2034 introduced by...

In an era of rising chronic diseases and patient-centric healthcare, injector pen polymers are enabling a revolution in self-administered drug delivery—combining durability, precision, and user comfort in lightweight, ergonomic devices. The global injector pen polymers market size was valued at USD 1.16 billion in 2024 and is expected to reach USD 1.82 billion by...